What is the Industrial Wearable Market Overview – definition, scope, and significance?

The Industrial Wearable Market comprises smart devices designed for use in demanding work environments, including augmented‑reality (AR) glasses, virtual‑reality (VR) headsets, smartwatches, smart bands, and biometric patches. These wearables integrate processors, memory modules, sensors, connectivity and optical components to improve safety, productivity, and data‑driven decision‑making across sectors such as automotive, aerospace, manufacturing, oil & gas, and energy & power. Their significance lies in enabling real‑time monitoring of worker health, hands‑free access to operational guidance, and streamlined maintenance procedures, thereby reducing downtime and occupational hazards.

What are the main drivers, restraints, challenges, and opportunities shaping the Industrial Wearable Market?

Key drivers include rising workplace safety regulations, the need for digital transformation in heavy‑industry processes, and growing adoption of Industry 4.0 technologies that demand real‑time data capture. Restraints stem from high upfront costs, concerns over data privacy, and limited battery life in harsh conditions. Challenges involve integration with legacy systems and ensuring durability against extreme temperatures and chemicals. Opportunities arise from advances in low‑power processors, edge‑AI analytics, and emerging use cases such as remote assistance and predictive maintenance.

Which growth trends are currently influencing the Industrial Wearable Market?

Current trends feature the convergence of AR glasses with computer‑vision analytics for on‑site troubleshooting, the shift from bulky VR headsets to lightweight mixed‑reality devices, and the expansion of health‑monitoring patches that track exposure to gases and fatigue levels. Additionally, manufacturers are embedding modular sensor arrays that can be customized per industry, while cloud‑based platforms are standardizing data ingestion from disparate wearable components, accelerating cross‑functional insights.

How has COVID‑19 impacted the Industrial Wearable Market and what is the recovery trajectory?

The pandemic accelerated demand for contact‑less monitoring and remote assistance solutions, prompting early adopters in manufacturing and oil & gas to equip workers with smartbands and AR glasses for hands‑free operation. Supply‑chain disruptions temporarily slowed component shipments, but the market rebounded as firms prioritized health‑centric technologies. Recovery is now strong, with a clear upward trajectory supported by renewed capital spending on safety‑first initiatives.

What does the Competitive Landscape of the Industrial Wearable Market look like?

The market is moderately consolidated, featuring specialist firms and larger technology vendors. Notable players include Blackline Safety Corp., Vuzix Corporation, and Workaround GmbH (Proglove), each focusing on niche product lines such as safety‑oriented wearables, AR visualisation, and industrial‑grade smart gloves. Recent consolidation activity shows strategic partnerships and selective acquisitions aimed at expanding sensor portfolios and software ecosystems, enhancing overall market competitiveness.

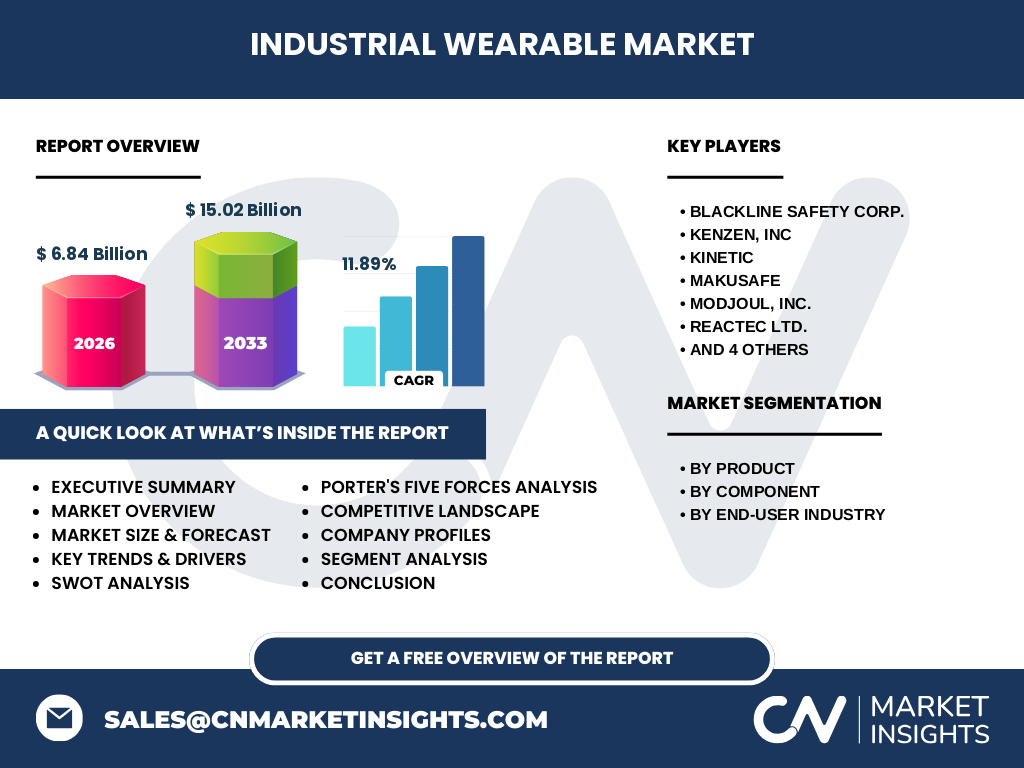

Can you provide an Executive Summary of the Industrial Wearable Market?

The Industrial Wearable Market is poised for rapid expansion, currently valued at $6.84 billion in 2026 and projected to reach $15.02 billion by 2033, reflecting an 11.89 % CAGR. Growth is driven by safety regulations, digital‑factory initiatives, and advances in low‑power components. While cost and integration hurdles persist, emerging AI‑driven analytics and modular designs present lucrative opportunities. Leading firms are strengthening their positions through innovation, strategic alliances, and focused sector penetration.

What are the market forecasts for 2025‑2032?

Based on the provided CAGR of 11.89 %, the market is expected to more than double its 2026 size by the early 2030s. Persistent adoption across automotive, aerospace, and manufacturing will sustain momentum, while expanding use in energy & power and oil & gas will broaden the addressable base. Forecasts indicate steady year‑over‑year growth, with peak acceleration anticipated as AI integration matures and component costs decline.

How is the market sized and shared by product, component, and end‑user segments?

By product, the market is divided among AR glasses, VR headsets, smartwatches, smart bands, and patches, each serving distinct operational needs—from visual guidance to biometric monitoring. Component segmentation covers processors, memory modules, optical systems, displays, electromechanical components, touchpads, sensors, connectivity modules, and camera modules, reflecting the complex hardware ecosystem. End‑user segmentation includes automotive, aerospace, manufacturing, oil & gas, and energy & power, illustrating broad cross‑industry relevance.

What is the global market size and share by region?

The global industrial wearable market totals $6.84 billion in 2026, with a forecasted rise to $15.02 billion by 2033. Although specific regional monetary breakdowns are not disclosed, the market is globally distributed, reflecting demand from major industrial hubs in North America, Europe, and the Asia‑Pacific, where manufacturing and energy sectors drive adoption.

How does the market perform regionally?

Regionally, North America leads in early technology adoption, supported by stringent workplace safety legislation and robust R&D ecosystems. Europe follows with strong automotive and aerospace clusters adopting AR‑based maintenance solutions. The Asia‑Pacific region shows the fastest growth trajectory, propelled by expanding manufacturing capacities, large‑scale energy projects, and increasing investment in smart‑factory initiatives.

Which companies are leading the Industrial Wearable Market and what are their strategies?

Key players include Blackline Safety Corp. (focus on real‑time gas detection wearables), Kenzen, Inc. (biometric health monitoring), Kinetic (smartband analytics), MaKusafe (safety‑centric wearables), Modjoul, Inc. (energy‑focused sensor integration), Reactec Ltd. (VR training platforms), Sleep Performance Inc. (fatigue‑management patches), Valencell Inc. (advanced sensor technology), Vuzix Corporation (AR glasses), and Workaround GmbH (Proglove) (industrial smart gloves). Their strategies revolve around expanding sensor capabilities, forging software partnerships, and targeting vertical‑specific solutions.

What does Porter’s Five Forces analysis reveal about the Industrial Wearable Market?

• Threat of new entrants: Moderate – high R&D costs and regulatory compliance create barriers, yet niche startups can enter with specialized sensors. • Bargaining power of suppliers: Moderate – diversified component suppliers for processors, optics and connectivity reduce concentration risk. • Bargaining power of buyers: High – large industrial customers demand customized solutions and price competitiveness. • Threat of substitutes: Low – few alternatives provide comparable real‑time, hands‑free data capture. • Competitive rivalry: High – multiple innovators compete on feature set, durability, and integration services.

What are the SWOT aspects of the Industrial Wearable Market?

Strengths: Enhances safety, enables real‑time analytics, aligns with Industry 4.0. Weaknesses: High device cost, limited battery endurance, data‑privacy concerns. Opportunities: AI‑driven edge processing, modular sensor kits, expansion into emerging economies. Threats: Rapid technology obsolescence, regulatory changes, potential cybersecurity breaches.

How is the value chain structured for industrial wearables?

The value chain begins with semiconductor and sensor manufacturers, proceeds to component assemblers (optical systems, displays, connectivity modules), followed by OEMs that integrate hardware into wearables. Software developers provide analytics platforms and cloud services, while system integrators tailor solutions for specific industries. Distribution occurs through direct B2B sales, system‑integration partners, and specialized industrial distributors, culminating in after‑sales support and data‑service contracts.

What key investment insights should investors consider?

Investors should target firms with strong sensor IP, scalable manufacturing, and proven vertical integrations, especially those serving high‑growth sectors like energy & power. Partnerships with cloud analytics providers and AI startups can unlock recurring revenue streams. Monitoring regulatory trends on occupational health will identify early‑adoption opportunities, while diversification across product types (e.g., AR glasses and health patches) mitigates single‑segment risk.

What are the main conclusions of the Industrial Wearable Market analysis?

The industrial wearable sector is entering a phase of accelerated growth, underpinned by safety imperatives and digital transformation. While cost and integration remain hurdles, rapid advances in low‑power electronics and AI analytics are set to widen adoption across all major industrial verticals. Market leaders that combine robust hardware with flexible software ecosystems are positioned to capture the expanding $15 billion opportunity by 2033.

Which research methodology was employed for this study?

The research combined primary interviews with industry experts, secondary data collection from company reports, regulatory filings, and reputable databases. Market sizing used bottom‑up aggregation of product revenues, while forecasting applied compound annual growth rate (CAGR) modeling based on historical trends and forward‑looking indicators such as capital expenditure forecasts and technology adoption rates.

What is the scope of the research?

The scope covers global industrial wearables, segmented by product type, component, and end‑user industry. It includes analysis of major competitors, value‑chain dynamics, and regional performance across the primary industrial hubs. The study excludes consumer‑grade wearables and focuses exclusively on devices meeting industrial durability, safety, and connectivity standards.

Which key companies and recent developments define the market?

Blackline Safety Corp. launched a next‑generation gas‑monitoring smartwatch with integrated LTE. Vuzix Corporation introduced lightweight AR glasses with enhanced field‑of‑view for aerospace maintenance. Workaround GmbH (Proglove) expanded its smart‑glove line to support 5G connectivity for real‑time data streaming. Kenzen, Inc. rolled out a biometric patch capable of continuous core‑temperature monitoring for oil‑field workers. Valencell Inc. partnered with a major automotive supplier to embed advanced heart‑rate sensors into factory‑floor smartbands.