What is the Heat Shrink Tubing Market Overview – Definition, scope, and significance?

Heat shrink tubing (HST) refers to a polymeric tube that contracts when exposed to heat, forming a tight, protective seal around cables, wires, or components. The market encompasses a wide range of materials—including polyolefin, PTFE, FEP, PFA, and PVDF—designed for diverse voltage ratings (low, medium, high) and end‑use sectors such as energy, telecommunications, automotive, aerospace, and medical devices. Its significance stems from the ability to provide electrical insulation, moisture resistance, mechanical protection, and aesthetic finishing in a compact, cost‑effective solution. As electronic systems become more compact and demand higher reliability, HST is increasingly adopted across OEMs and service providers, driving market growth worldwide.

What are the Heat Shrink Tubing Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include the rapid expansion of renewable energy infrastructure, the rise of electric vehicles, and the growing need for reliable wiring in data centers and smart‑grid applications. Stringent safety standards and increasing automation in manufacturing further boost demand for high‑performance HST. Restraints arise from the high cost of advanced fluoropolymer grades and volatile raw‑material prices, which can limit adoption in price‑sensitive segments. Challenges involve strict compliance requirements in aerospace and defense, as well as competition from alternative insulation technologies such as liquid‑applied coatings. Opportunities are evident in the development of nano‑filled or bi‑based shrink materials, customization for 5G infrastructure, and expanding applications in medical device miniaturization.

What are the current Heat Shrink Tubing Market Growth Trends?

Two major trends dominate the market today. First, there is a shift toward high‑temperature, low‑flame‑spread fluoropolymer grades to meet stricter fire safety regulations in transportation and building construction. Second, manufacturers are offering modular, pre‑sized kits and automated shrink‑lamination equipment to reduce installation time and labor costs. Additionally, the integration of RFID tags and conductive inks within shrink tubing is emerging as a value‑added service for the IoT and smart‑sensor ecosystems.

How did COVID‑19 impact the Heat Shrink Tubing Market and what is the recovery trajectory?

The pandemic caused short‑term disruptions in supply chains for raw polymers and delayed capital projects in automotive and aerospace, leading to a modest dip in shipments during 2020‑2021. However, accelerated digital transformation, increased demand for remote connectivity, and government stimulus for renewable energy helped the market rebound quickly. By 2022, order backlogs were cleared, and the sector entered a growth phase supported by the surge in data‑center builds and electric‑vehicle production, positioning it for sustained expansion.

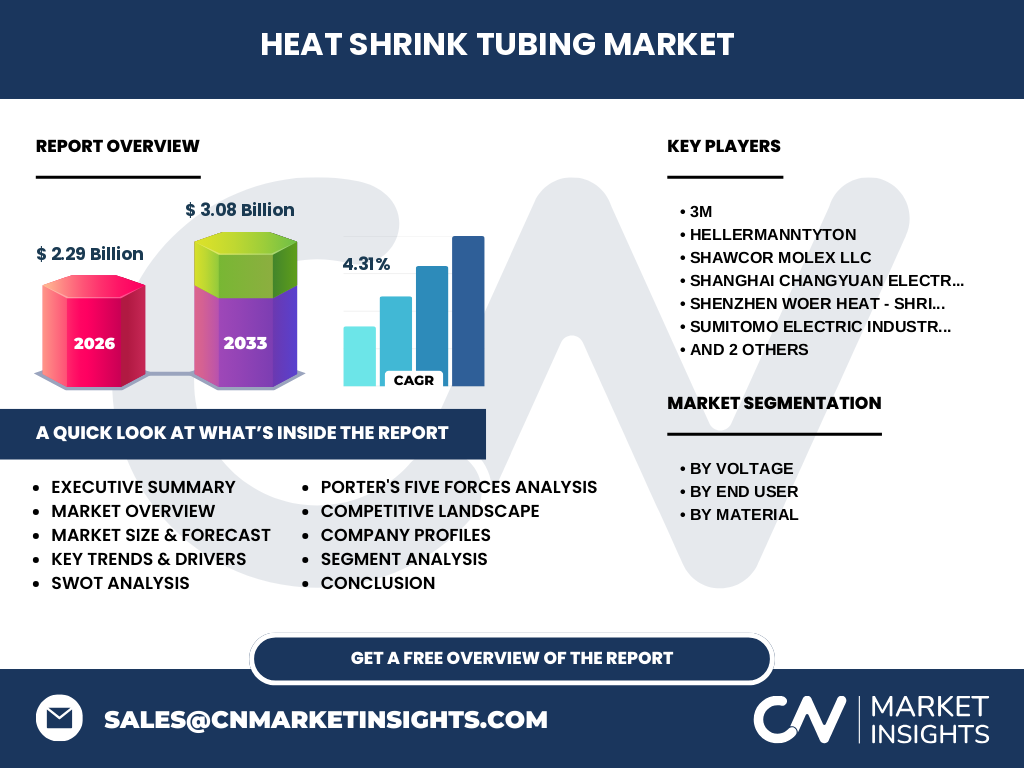

Who are the major competitors in the Heat Shrink Tubing Market and what is the level of market consolidation?

The competitive landscape is characterized by a mix of global conglomerates and specialized regional players. Leading firms include 3M, HellermannTyton, SHAWCOR Molex LLC, Shanghai Changyuan Electronic Material Co., Ltd, Shenzhen Woer Heat‑Shrinkable Material Co., Ltd, Sumitomo Electric Industries, Ltd., TE Connectivity, and Techflex, Inc. While the market is relatively fragmented, recent strategic alliances and acquisitions—especially among Asian manufacturers seeking scale—indicate a moderate trend toward consolidation.

What are the key findings in the Executive Summary of the Heat Shrink Tubing Market?

The market is valued at US 2.29 billion in 2026 and is projected to reach US 3.08 billion by 2033, reflecting a CAGR of 4.31 % over the forecast horizon. Growth is propelled by demand from renewable‑energy projects, electric‑vehicle wiring, and high‑speed telecommunications. Advanced fluoropolymer grades and automated application solutions are differentiating factors. Despite raw‑material price volatility, the market remains resilient, with ample opportunity for innovators to capture share through sustainability‑focused products and digital integration.

What is the Heat Shrink Tubing Market Forecast for 2025‑2032?

Building on the 4.31 % CAGR, the market is expected to maintain steady upward momentum through 2032. By 2028, the market size is anticipated to surpass US 2.6 billion, with continued acceleration in the electric‑vehicle and 5G infrastructure segments. Forecasts suggest that high‑voltage and high‑temperature tubing will exhibit the fastest growth rates, while traditional low‑voltage polyolefin products will experience modest, steady gains.

How is the Heat Shrink Tubing Market sized and shared by segmentation?

Segmentation is based on voltage level, end‑user industry, and material type. Voltage categories—low, medium, and high—address distinct performance specifications, with low‑voltage accounting for the largest volume due to widespread use in consumer electronics and building wiring. End‑user distribution spans energy, utilities, electrical power, infrastructure/construction, industrial, telecommunications, automotive, aerospace, defense, mass transit, medical, petrochemical, and mining. Material segmentation includes polyolefin (dominant in low‑cost applications), PTFE, fluorinated ethylene propylene (FEP), perfluoro alkoxy alkane (PFA), and polyvinylidene fluoride (PVDF), each targeting niche performance requirements such as high temperature resistance or chemical stability.

What is the Global Heat Shrink Tubing Market size and share by region?

The market is truly global, with major contributions from North America, Europe, Asia‑Pacific, and the Rest of the World. While specific regional revenue figures are not disclosed, Asia‑Pacific leads due to a concentration of manufacturing hubs, rising automotive production, and extensive renewable‑energy investments. North America and Europe follow, driven by stringent safety standards and robust telecom infrastructure upgrades. Emerging economies in Latin America and the Middle East are projected to grow faster than mature markets, reflecting expanding industrialization.

What does the Regional Analysis of the Heat Shrink Tubing Market reveal?

In Asia‑Pacific, China and India dominate manufacturing output, with Chinese firms such as Shanghai Changyuan and Shenzhen Woer expanding capacity to serve both domestic and export markets. Japan’s Sumitomo Electric contributes high‑performance fluoropolymer products for aerospace and automotive applications. North America benefits from the presence of 3M, TE Connectivity, and a strong demand base in energy and defense. Europe’s market is anchored by strict EU regulations that favor high‑quality, fire‑retardant tubing, supporting companies like HellermannTyton. Overall, regional growth is aligned with infrastructure spending, renewable‑energy deployment, and the rollout of 5G networks.

Which companies lead the Heat Shrink Tubing Market and what are their strategies?

3M leverages its broad material portfolio and extensive distribution network to offer both standard and customized solutions across voltage classes. HellermannTyton focuses on engineering services and value‑added kits for automotive and industrial wiring. SHAWCOR Molex emphasizes integration with connector systems, targeting data‑center and telecom markets. Shanghai Changyuan and Shenzhen Woer pursue cost leadership and rapid scale‑up in polyolefin grades. Sumitomo Electric differentiates through advanced fluoropolymer technologies for aerospace and high‑temperature applications. TE Connectivity and Techflex prioritize digitalization, offering shrink‑lamination equipment and IoT‑enabled tubing.

How does Porter’s Five Forces analysis apply to the Heat Shrink Tubing Market?

Threat of new entrants is moderate; high capital investment in extrusion lines and material R&D creates barriers, yet low‑to‑moderate entry is possible for niche fluoropolymer producers. Bargaining power of suppliers is relatively high because specialty polymers are sourced from a limited pool of chemical manufacturers, exposing the market to price swings. Bargaining power of buyers is moderate; large OEMs negotiate pricing but require strict quality compliance, limiting switching. Threat of substitutes is low to moderate, as alternatives like liquid‑applied coatings lack the mechanical robustness and ease of installation of HST. Competitive rivalry is intense, with several global players competing on technology, price, and service breadth.

What are the SWOT insights for the Heat Shrink Tubing Market?

Strengths: Proven reliability, wide material range, and ability to meet stringent safety standards. Weaknesses: Dependence on volatile polymer prices and limited differentiation for basic polyolefin products. Opportunities: Development of sustainable bio‑based shrink materials, integration with smart‑sensor technologies, and expanding demand from EVs and 5G. Threats: Regulatory changes impacting fluoropolymer use, global supply‑chain disruptions, and competitive pressure from emerging insulation technologies.

What does the Heat Shrink Tubing Market value chain look like?

The value chain begins with raw‑material suppliers (polymer resin producers), followed by extruders who formulate and produce tubing. Next are coating and printing specialists who add color, markings, or conductive inks. Distribution channels include distributors, electronic component wholesalers, and direct OEM sales. End‑users integrate the tubing during assembly, often with heat‑shrink guns or automated laminators. After‑sales services such as technical support, training, and warranty management complete the chain, creating multiple touchpoints for value creation.

What key investment insights can be drawn from the Heat Shrink Tubing Market?

Investors should focus on companies with strong fluoropolymer capabilities, as these command premium pricing and address high‑growth sectors like aerospace and EVs. Participation in joint ventures that develop automated shrink‑lamination equipment offers upside in the service‑oriented segment. Acquisitions of niche bio‑based material manufacturers could position a portfolio for the emerging sustainability trend. Finally, allocating capital to firms expanding in fast‑growing regions—particularly Asia‑Pacific—aligns with projected demand spikes.

What is the overall conclusion of the Heat Shrink Tubing Market analysis?

The heat shrink tubing market is on a solid growth trajectory, underpinned by a 4.31 % CAGR and a forecasted increase from US 2.29 billion in 2026 to US 3.08 billion by 2033. Technological innovation, expanding end‑use applications, and regional infrastructure investments provide a strong foundation for continued expansion. While raw‑material cost pressures and regulatory scrutiny present challenges, companies that innovate in material science and digital integration are well‑positioned to capture market share.

What research methodology was employed for this Heat Shrink Tubing Market study?

The research combines primary interviews with industry executives, suppliers, and end‑user engineers, alongside secondary data collection from company annual reports, trade publications, and market databases. Quantitative analysis uses trend extrapolation based on the provided 2026 market size (US 2.29 billion) and forecast (US 3.08 billion) to calculate the 4.31 % CAGR. Qualitative insights are derived from expert opinion and competitive intelligence.

What is the scope of this Heat Shrink Tubing Market research?

The study covers global market dynamics, segmentation by voltage, end‑user, and material, and regional performance across North America, Europe, Asia‑Pacific, and the Rest of the World. It excludes detailed financial breakdowns beyond the provided market size and CAGR, and does not quantify market share percentages for individual companies or regions.

Which key companies and recent developments are shaping the Heat Shrink Tubing Market?

3M announced a new line of high‑temperature polyimide‑based shrink tubing for aerospace connectors. HellermannTyton launched a smart‑label program embedding RFID tags within shrink sleeves for supply‑chain visibility. SHAWCOR Molex released a pre‑configured cable‑assembly kit targeting 5G base stations. Shanghai Changyuan expanded its polyolefin capacity by 20 % to meet rising demand in electric‑vehicle wiring. Shenzhen Woer introduced a bio‑based polyolefin grade aimed at reducing carbon footprint. Sumitomo Electric unveiled a fluoropolymer tubing with enhanced chemical resistance for petrochemical applications. TE Connectivity acquired a niche laminator manufacturer to strengthen its automated installation services. Techflex announced a partnership with a major telecom carrier to co‑develop shrink‑tubing solutions for underwater fiber‑optic cables.