What is the Robotic Welding Market overview, including its definition, scope, and significance?

The Robotic Welding Market encompasses systems and solutions that automate welding processes using programmable robotic arms. It covers both spot and arc welding technologies across various payload capacities—from less than 50 kg to over 150 kg—and serves end‑users such as automotive, transportation, electrical & electronics, metal & machinery, and construction sectors. The market’s significance lies in its ability to boost production efficiency, improve weld quality, reduce labor costs, and enhance worker safety, making it a pivotal component of modern manufacturing and industrial automation strategies.

What are the main drivers, restraints, challenges, and opportunities shaping the Robotic Welding Market?

Key drivers include rising automation adoption, stringent quality standards, and labor shortages in high‑mix, high‑volume production. Restraints arise from high upfront capital investment and the need for skilled personnel to program and maintain robots. Challenges involve integration complexity with existing production lines and concerns over cybersecurity. Opportunities are emerging in advanced sensor integration, AI‑enabled welding optimization, and expanding applications in emerging sectors such as electric vehicle manufacturing and renewable‑energy equipment.

What current and emerging growth trends are influencing the Robotic Welding Market?

Current trends feature a shift toward collaborative robots (cobots) for flexible cell layouts, increased use of laser‑based welding, and the incorporation of Industry 4.0 connectivity for real‑time monitoring. Emerging trends include the development of hybrid welding robots that combine arc and spot capabilities, the adoption of cloud‑based analytics for predictive maintenance, and the rise of modular, scalable robotic platforms that can be quickly re‑configured for short‑run production.

How has COVID‑19 impacted the Robotic Welding Market, and what is the recovery trajectory?

The pandemic accelerated the need for contact‑less manufacturing, prompting many facilities to invest in robotic welding to maintain output while reducing on‑site labor. Initial demand slowed during lockdowns, but the market rebounded quickly as manufacturers sought resilience against future disruptions. Recovery is now robust, with a clear upward trajectory supported by renewed capital spending and an emphasis on supply‑chain independence.

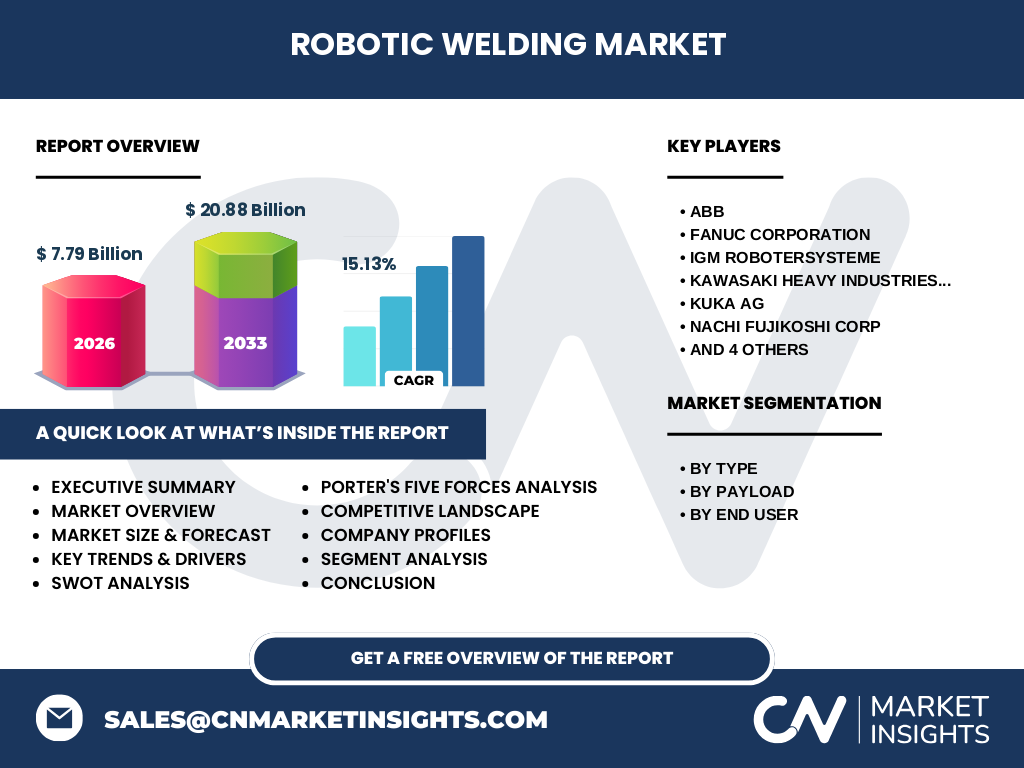

Who are the major competitors in the Robotic Welding Market, and what does the competitive landscape look like?

The market is dominated by established automation leaders such as ABB, Fanuc Corporation, Kawasaki Heavy Industries, Kuka AG, and Yaskawa Electric Corporation, alongside niche specialists like IGM ROBOTERSYSTEME, NACHI FUJIKOSHI CORP, NOVARC TECHNOLOGY, OTC DAIHEN, and Panasonic Corporation. Competitive dynamics are characterized by continuous product innovation, strategic partnerships, and occasional mergers and acquisitions to broaden technology portfolios and geographic reach.

What are the key findings in the executive summary of the Robotic Welding Market?

The market is valued at USD 7.79 billion in 2026 and is projected to reach USD 20.88 billion by 2033, delivering a robust CAGR of 15.13 %. Growth is driven by expanding automation in automotive and electronics, increasing demand for high‑precision welds, and rapid adoption of smart manufacturing. The competitive field is concentrated among a few global players, while emerging opportunities in AI‑enhanced welding and modular robot designs promise to further accelerate market expansion.

What are the forecast expectations for the Robotic Welding Market from 2025 to 2032?

Based on the provided CAGR of 15.13 %, the market is expected to maintain strong double‑digit growth through 2032. This trajectory reflects ongoing capital investment in advanced welding robots, widening adoption across non‑automotive sectors, and the rollout of next‑generation technologies that improve cycle time and reduce energy consumption.

How is the Robotic Welding Market sized and shared by type, payload, and end‑user segmentation?

Segmentation by type includes Spot Welding and Arc Welding, each serving distinct application needs. By payload, the market is divided into three categories: less than 50 kg, 50‑150 kg, and more than 150 kg, reflecting the range from light‑duty assembly to heavy‑frame construction. End‑user segmentation comprises Automotive & Transportation, Electrical & Electronics, Metal & Machinery, and Construction, with automotive traditionally holding the largest demand due to high production volumes and strict quality standards.

What is the global distribution of market size and share by region?

The Robotic Welding Market exhibits a worldwide footprint, with mature adoption in North America, Europe, and East Asia, while rapidly growing demand is observed in Southeast Asia and South America. Each region contributes to the overall market size, reflecting localized manufacturing hubs and varying levels of automation readiness.

What are the detailed regional performance insights for the Robotic Welding Market?

North America leads in technology integration and early adoption of collaborative robots. Europe displays strong growth driven by stringent environmental regulations and a shift toward electric vehicle production. East Asia, particularly Japan, South Korea, and China, remains the largest manufacturing base, supporting high volumes of automotive and electronics output. Emerging markets in Latin America and the Middle East show accelerating investment in industrial automation as part of broader economic diversification plans.

Which companies are leading in the Robotic Welding Market, and what are their strategic approaches?

ABB focuses on integrated digital welding solutions and extensive service networks. Fanuc emphasizes high‑speed, high‑precision robots with strong OEM relationships. Kawasaki leverages its machining expertise to offer robust heavy‑payload systems. Kuka drives innovation through modular robot architecture and AI‑enabled process control. Yaskawa targets flexible automation for small‑batch production. These leaders complement their product strengths with strategic alliances, localized support, and continuous R&D investment.

How does Porter’s Five Forces analysis apply to the Robotic Welding Market?

Threat of new entrants is moderate due to high capital requirements and technology barriers. Bargaining power of suppliers is limited, as component sourcing is diversified across global electronics and actuator manufacturers. Bargaining power of buyers is growing, driven by large OEMs demanding cost‑effective, high‑performance solutions. Threat of substitutes remains low because alternative welding methods lack the repeatability and integration offered by robots. Rivalry among existing competitors is intense, fostering rapid innovation and price competition.

What are the SWOT highlights for the Robotic Welding Market?

Strengths: High productivity gains, consistent weld quality, and safety improvements.

Weaknesses: Significant initial investment and the need for specialized programming skills.

Opportunities: Expansion into emerging sectors, AI‑driven optimization, and modular robot designs.

Threats: Economic downturns affecting capital spending and potential supply‑chain disruptions for critical components.

What does the value chain for the Robotic Welding Market look like?

The value chain begins with research and development of robotic platforms, followed by component manufacturing (actuators, sensors, controllers). Integration services combine hardware with welding-specific software, after which system integration occurs on the factory floor. Post‑sale services include training, maintenance, and aftermarket upgrades, creating ongoing revenue streams for suppliers.

What key investment insights can be drawn from the Robotic Welding Market?

Investors should focus on companies with strong AI and connectivity capabilities, as these are poised to dominate the next wave of smart welding. Funding opportunities exist in niche players offering specialized payload solutions or hybrid welding technologies. Growth in non‑automotive end‑users presents a diversification avenue, reducing reliance on cyclical automotive demand.

What are the main conclusions from the Robotic Welding Market analysis?

The market is on a clear growth path, underpinned by a 15.13 % CAGR and a near‑tripling of value by 2033. Automation imperatives, evolving industry standards, and the push for resilient supply chains drive adoption. While capital costs and talent gaps pose challenges, technological advances and expanding applications across multiple sectors provide a compelling outlook.

How was the research for this report conducted?

The methodology combined primary interviews with industry experts, secondary data collection from company filings, market databases, and trade publications, followed by triangulation to validate figures. Forecast modeling applied the stated CAGR to the baseline market size, and segmentation analysis leveraged the provided classification framework.

What is the scope of the research, and what are its limitations?

The study covers global market size, segmentation by type, payload, and end‑user, as well as regional performance and competitive dynamics. It relies on publicly available data and expert insights up to 2026, with projections extending to 2033. Limitations include the exclusion of granular market share percentages and the absence of confidential proprietary data.

Which key companies are active in the Robotic Welding Market, and what recent developments have they announced?

Leading firms such as ABB, Fanuc, Kawasaki, Kuka, and Yaskawa have launched next‑generation welding robots featuring enhanced payload capacity and AI‑based weld monitoring. IGM ROBOTERSYSTEME introduced a compact spot‑welding unit aimed at small‑batch production. NACHI FUJIKOSHI released a hybrid arc/spot welding solution for automotive chassis. NOVARC TECHNOLOGY announced a partnership with a major automotive OEM to deploy collaborative welding cells. Panasonic unveiled a new sensor suite for real‑time defect detection, while OTC DAIHEN expanded its service network across Southeast Asia.