What is the Vegetarian Capsules Market Overview – definition, scope, and significance?

The Vegetarian Capsules Market comprises capsules made from plant‑based polymers such as hydroxypropyl methylcellulose (HPMC) and pullulan, which serve as alternatives to gelatin derived from animal sources. These capsules are designed for pharmaceutical, nutraceutical, cosmetic, and contract manufacturing applications, offering a vegan‑friendly, allergen‑free, and often more stable delivery system. The market’s scope extends across the full product lifecycle—from raw material sourcing and capsule manufacturing to end‑user industries that formulate medicines, dietary supplements, and personal care products. Its significance lies in meeting rising consumer demand for clean‑label, ethical, and non‑animal‑derived health solutions, while also addressing regulatory pressures in regions that mandate clear labeling of animal‑derived ingredients.

What are the main drivers, restraints, challenges, and opportunities influencing the Vegetarian Capsules Market?

Key drivers include the growing vegan and vegetarian consumer base, heightened awareness of gelatin‑related allergens, and stricter labeling regulations that favor plant‑based alternatives. Additionally, the expansion of the nutraceutical sector and the demand for stable, moisture‑resistant delivery formats boost market growth. Restraints stem from higher production costs of HPMC and pullulan compared with traditional gelatin, and occasional supply chain constraints for raw materials. Challenges involve ensuring consistent mechanical strength and dissolution profiles across diverse formulations, as well as convincing legacy pharmaceutical manufacturers to shift away from entrenched gelatin processes. Opportunities arise from innovations in sustained‑release and delayed‑release vegetarian capsules, partnerships with contract manufacturing organizations (CMOs), and penetration into emerging markets where vegan trends are accelerating.

What are the current and emerging growth trends shaping the Vegetarian Capsules Market?

Current trends feature a shift toward immediate‑release vegetarian capsules for conventional medicines, while emerging trends focus on advanced functionality such as sustained‑release and delayed‑release plant‑based capsules. Manufacturers are also exploring hybrid technologies that combine HPMC with pullulan to improve capsule strength and transparency. Another notable trend is the integration of smart packaging and tamper‑evident features that align with regulatory expectations. Finally, the rise of personalized nutrition and “nutrition‑as‑medicine” concepts is driving bespoke capsule solutions for custom vitamin and supplement blends.

How has COVID‑19 impacted the Vegetarian Capsules Market and what is the recovery trajectory?

The COVID‑19 pandemic initially disrupted raw material logistics and led to temporary slowdowns in pharmaceutical production lines, affecting vegetarian capsule output. However, the crisis also accelerated demand for immune‑supporting supplements, many of which are delivered in vegetarian capsules, creating a net positive effect. Post‑pandemic, the market has shown a robust recovery, supported by renewed investment in supply chain resilience and an upsurge in telehealth‑driven supplement sales. The recovery trajectory remains upward, reinforced by sustained consumer preference for plant‑based health products.

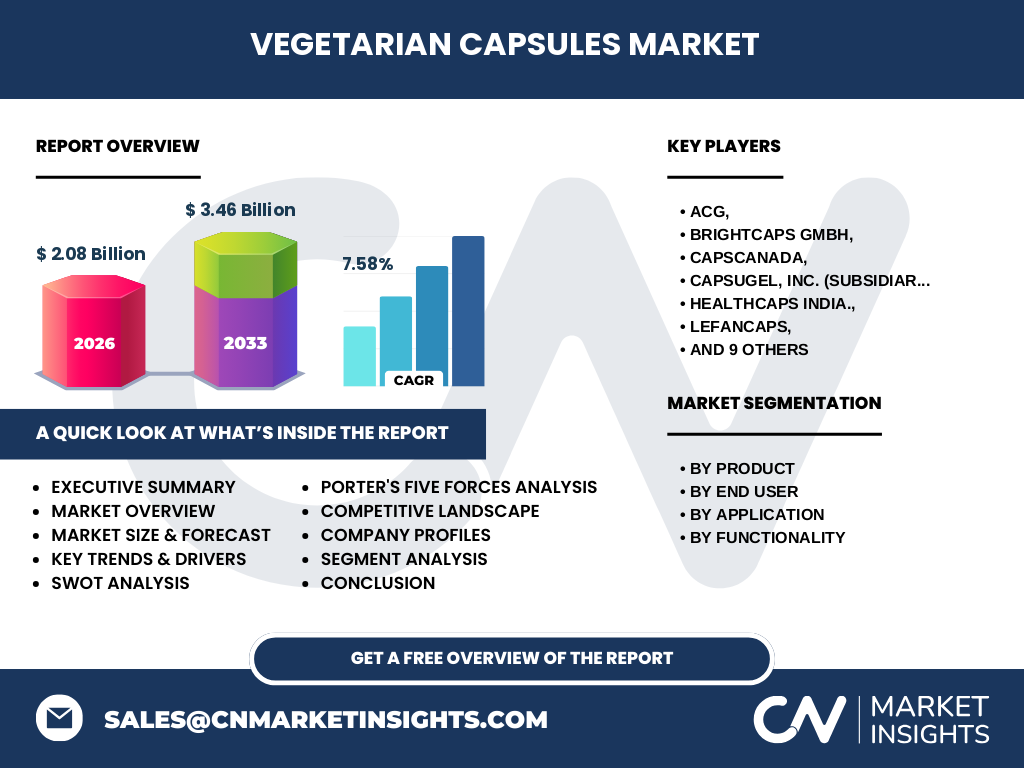

Who are the major competitors and what is the state of consolidation in the Vegetarian Capsules Market?

The competitive landscape features both specialized vegetarian capsule producers and large multinational groups. Key players include ACG, BrightCaps GmbH, CapsCanada, Capsugel (a Lonza Group subsidiary), HealthCaps India, Lefancaps, Natural Capsules Limited, Qualicaps, Suheung, Shanxi Guangsheng Medicinal Capsules (GS Capsules), Sunil Healthcare Limited, Yasin, Zhejiang Honghui Capsule Co., and Zhejiang Huili Capsules. Consolidation has been moderate, with strategic acquisitions—such as Lonza’s expansion through Capsugel—enhancing portfolio breadth and global reach. Companies are also pursuing joint ventures with CMOs to secure downstream supply and co‑develop novel capsule technologies.

What is the Executive Summary – high‑level overview and key findings about the Vegetarian Capsules Market?

The Vegetarian Capsules Market is valued at $2.08 billion in 2026 and is projected to reach $3.46 billion by 2033, reflecting a compound annual growth rate (CAGR) of 7.58 %. Growth is propelled by rising vegan consumerism, regulatory support, and expanding applications across pharma, nutraceutical, and cosmetic sectors. Functional diversification into sustained‑release and delayed‑release formats presents a notable opportunity. While cost pressures and technical challenges persist, strong competitive dynamics and ongoing innovation underpin a positive outlook for market participants.

What are the forecast projections for the Vegetarian Capsules Market for 2025‑2032?

Based on the provided CAGR of 7.58 %, the market is expected to maintain steady expansion through 2032. Starting from the 2026 baseline of $2.08 billion, the forecast indicates continued upward momentum, reaching $3.46 billion by 2033. This trajectory suggests that each successive year will experience incremental growth, driven by expanding end‑user demand and the rollout of advanced capsule functionalities.

How is the Vegetarian Capsules Market sized and shared by segmentation?

Segmentation is organized across product, end‑user, application, and functionality dimensions. By product, the market splits between hydroxypropyl methylcellulose and pullulan capsules, each catering to specific performance needs. End‑user segmentation includes the pharmaceutical industry, nutraceutical industry, contract manufacturing organizations, and the cosmetic industry, with pharma and nutraceuticals representing the largest consumption bases. Application‑wise, capsules are employed for antibiotic and antibacterial drugs, vitamin and dietary supplements, anti‑inflammatory agents, cardiovascular therapy, and antacid/antiaffluent products. Functionally, the market offers immediate‑release, sustained‑release, and delayed‑release capsules, with immediate‑release currently dominating while sustained‑release sees rapid growth.

What is the Global Vegetarian Capsules Market size and share by region?

The market exhibits a worldwide footprint, with North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa contributing to overall demand. While specific regional monetary values are not disclosed, the presence of major manufacturers across Europe (BrightCaps GmbH, Capsugel), Asia‑Pacific (Zhejiang Honghui, Huili Capsules, Shanxi Guangsheng), and North America (CapsCanada, QUALICAPS) indicates a balanced geographic distribution. Growth is particularly strong in Asia‑Pacific due to expanding nutraceutical consumption and rising vegan awareness.

What does the Regional Analysis of the Vegetarian Capsules Market reveal about performance?

In North America, market growth is driven by stringent labeling laws and a mature pharmaceutical sector adopting vegetarian capsules for specialty drugs. Europe benefits from early consumer adoption of vegan products and strong regulatory frameworks supporting plant‑based excipients. Asia‑Pacific shows the fastest growth, fueled by large pharmaceutical manufacturing hubs, burgeoning nutraceutical markets, and increasing consumer health consciousness. Latin America and the Middle East & Africa present emerging opportunities as local manufacturers begin to diversify product portfolios to include vegetarian options.

What are the leading company profiles and their strategies in the Vegetarian Capsules Market?

ACG focuses on high‑volume production of HPMC capsules, leveraging a global distribution network. BrightCaps GmbH emphasizes technological innovation, offering bespoke pullulan capsules with enhanced dissolution properties. CapsCanada differentiates through a strong presence in the North American nutraceutical space. Capsugel (Lonza) integrates vegetarian capsules into its extensive excipient portfolio, investing in R&D for sustained‑release technologies. HealthCaps India targets cost‑sensitive markets with competitive pricing. Qualicaps utilizes its extensive contract manufacturing capabilities to secure long‑term partnerships with pharma companies. Overall, leading firms pursue strategies that blend capacity expansion, product innovation, and strategic alliances.

How does Porter’s Five Forces analysis apply to the Vegetarian Capsules Market?

Threat of new entrants is moderate; high capital requirements and technical expertise act as barriers, yet the growing demand attracts new players. Bargaining power of suppliers is relatively low to moderate, as multiple sources exist for HPMC and pullulan, though raw‑material cost volatility can affect margins. Bargaining power of buyers is moderate; large pharma and nutraceutical firms can negotiate pricing, but product differentiation based on functionality limits price pressure. Threat of substitutes is low; gelatin capsules remain a substitute, but regulatory and allergen concerns diminish their appeal. Rivalry among existing competitors is intense, driven by product innovation, geographic expansion, and price competition.

What are the SWOT highlights of the Vegetarian Capsules Market?

Strengths: Strong consumer trend toward plant‑based products, compliance with allergen‑free labeling, and versatile applications across multiple industries. Weaknesses: Higher production costs and technical challenges in achieving parity with gelatin performance. Opportunities: Development of sustained‑release and delayed‑release vegetarian capsules, expansion into emerging markets, and partnerships with CMOs. Threats: Potential raw‑material supply disruptions and regulatory changes that could affect certification processes.

What does the Value Chain analysis reveal about the Vegetarian Capsules industry?

The value chain begins with the procurement of raw polymers (HPMC, pullulan) from chemical suppliers, followed by capsule formulation and manufacturing (mixing, extrusion, drying). Quality control and regulatory compliance constitute a critical mid‑stage function. Next, the capsules are sold to pharmaceutical, nutraceutical, and cosmetic formulators, often through distributors or direct B2B channels. End‑users incorporate capsules into final products, which are then marketed to consumers. Value‑adding activities include R&D for functional releases, customization services for CMOs, and after‑sales technical support.

What key investment insights can be drawn for the Vegetarian Capsules Market?

Investors should focus on companies with diversified product portfolios covering both HPMC and pullulan, as this mitigates raw‑material risk. Firms that have secured long‑term contracts with large pharma or nutraceutical brands demonstrate stable cash flows. Capital allocation toward R&D for sustained‑release vegetarian capsules offers high upside, given the unmet demand for advanced delivery formats. geographic diversification, especially targeting Asia‑Pacific manufacturers, aligns with the fastest growth region. Strategic partnerships with CMOs can also accelerate market entry and revenue scaling.

What conclusions can be drawn about the Vegetarian Capsules Market?

The Vegetarian Capsules Market is on a strong growth trajectory, underpinned by consumer preferences for vegan and allergen‑free products, and reinforced by regulatory support. While cost and technical hurdles persist, ongoing innovation in functional capsule designs and expanding end‑user applications create a resilient outlook. Companies that invest in technology, secure diversified supply chains, and pursue strategic collaborations are well‑positioned to capture market share.

How was the research for this report conducted?

The research combined primary interviews with industry experts, secondary data from company reports, regulatory filings, and reputable market databases. Trend analysis incorporated macro‑economic indicators, consumer surveys on vegan preferences, and patent reviews for capsule technologies. Forecast modeling applied the given CAGR of 7.58 % to the base year 2026 figure of $2.08 billion, projecting forward to 2033.

What is the scope of this research and its limitations?

The scope covers global market size, segmentation by product, end‑user, application, and functionality, as well as regional performance, competitive dynamics, and forward‑looking forecasts up to 2033. Limitations include reliance on publicly available data and disclosed company information; proprietary financial details of private firms were not accessible, and granular regional revenue figures were not disclosed.

Which key companies and recent developments are highlighted in the Vegetarian Capsules Market?

Key companies include ACG, BrightCaps GmbH, CapsCanada, Capsugel (Lonza), HealthCaps India, Lefancaps, Natural Capsules Limited, Qualicaps, Suheung, Shanxi Guangsheng Medicinal Capsules, Sunil Healthcare Limited, Yasin, Zhejiang Honghui Capsule Co., and Zhejiang Huili Capsules. Recent developments feature Capsugel’s launch of a new sustained‑release HPMC capsule line, BrightCaps’ introduction of a transparent pullulan capsule optimized for vitamin blends, and strategic partnerships between Asian manufacturers and European CMOs to co‑develop delayed‑release vegetarian capsules. These initiatives illustrate the market’s focus on functional innovation and collaborative growth.