What is the Medical Writing Market Overview – definition, scope, and significance?

The Medical Writing Market comprises professional services that create scientifically accurate, regulatory‑compliant, and audience‑focused documents for the life‑science ecosystem. Its scope covers clinical trial documentation (protocols, investigator brochures, clinical study reports), regulatory submissions (INDs, NDA/BLA dossiers, post‑approval safety reports), scientific communications (manuscripts, conference posters, abstracts), as well as medical journalism, education materials, and marketing content. The market’s significance lies in its role as a critical bridge between research findings and stakeholders such as regulators, healthcare professionals, investors, and patients, ensuring that complex data are communicated clearly, ethically, and in a manner that accelerates product development, market entry, and informed clinical practice.

What are the Medical Writing Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include the expanding pipeline of pharmaceuticals and biologics, heightened regulatory scrutiny demanding high‑quality documentation, and the rise of outsourcing to specialist firms that offer speed, expertise, and cost efficiencies. Restraints arise from stringent data confidentiality requirements and the limited pool of highly qualified scientific writers, which can constrain capacity. Challenges involve rapid changes in regulatory guidelines across regions, the need for multilingual capabilities, and integrating advanced technologies such as AI‑assisted drafting while maintaining compliance. Opportunities are emerging in niche therapeutic areas (gene therapy, cell therapy), digital transformation of documentation workflows, and the growing demand for medical education and marketing content driven by patient‑centric care models.

What Growth Trends are shaping the Medical Writing Market?

Current trends feature an accelerated shift toward outsourced medical writing services, driven by pharma and biotech firms focusing on core R&D activities. Digitalization is reshaping the workflow, with cloud‑based platforms enabling real‑time collaboration and version control. AI and natural‑language processing tools are being piloted to streamline routine drafting, allowing writers to concentrate on high‑value interpretation. Additionally, the increasing importance of real‑world evidence (RWE) studies expands the need for specialized regulatory and scientific writing services. Emerging therapeutic modalities, such as mRNA vaccines and advanced therapies, demand novel documentation approaches, creating fresh growth avenues.

How did COVID‑19 impact the Medical Writing Market, and what is the recovery trajectory?

The pandemic triggered a surge in clinical trial activity and accelerated regulatory submissions for vaccines and therapeutics, boosting demand for rapid, high‑quality medical writing. Remote work adoption forced firms to adopt secure digital collaboration tools, which have since become standard practice. While early‑pandemic disruptions slowed some non‑COVID projects, the overall market rebounded quickly, and the heightened focus on speed and compliance persists. The recovery trajectory is positive, with the market now poised for sustained growth as post‑pandemic R&D pipelines expand and organisations retain the efficiencies gained from virtual collaboration.

Who are the major competitors and what is the competitive landscape like?

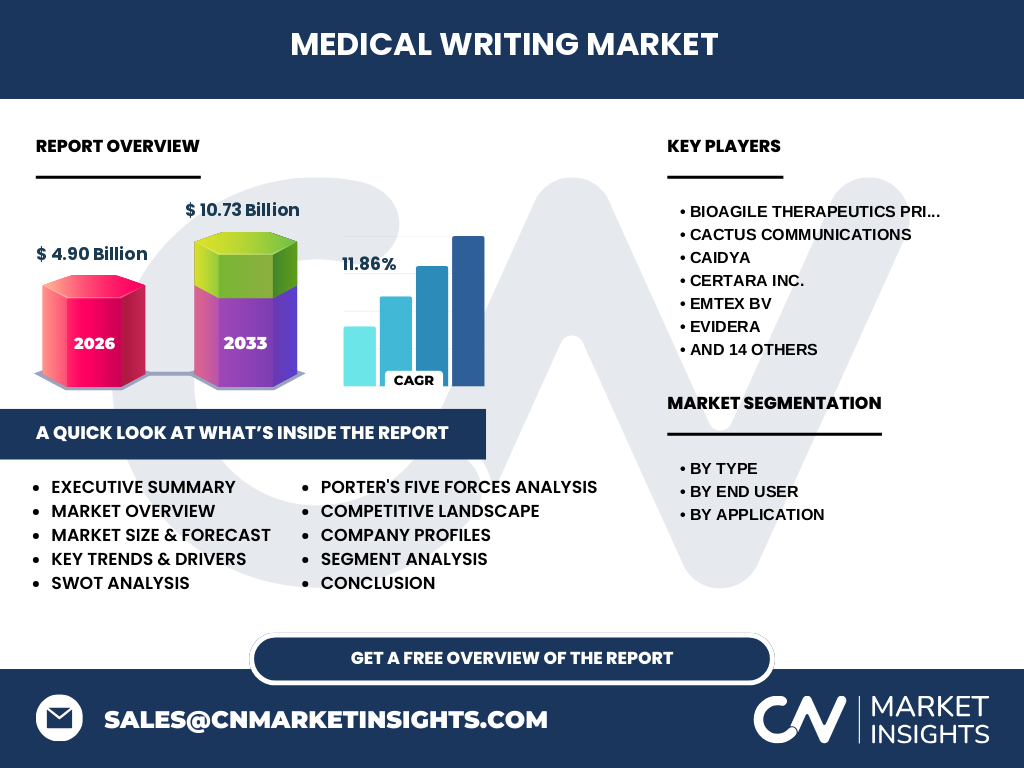

The market is fragmented, featuring a mix of global service providers, specialized boutique firms, and in‑house capabilities of large pharma. Major competitors include BioAgile Therapeutics Private Limited, Cactus Communications, Certara Inc., Evidera, Indegene Ltd, Parexel International Corp, SGS SA, Tata Consultancy Services Ltd, TransPerfect Life Sciences, and Wipro Ltd, among others. Consolidation is moderate, with larger firms acquiring niche specialists to broaden service portfolios and geographic reach. Competitive advantage hinges on domain expertise, regulatory knowledge across regions, technology integration, and the ability to deliver high‑quality output within compressed timelines.

What are the key findings in the Executive Summary?

The Medical Writing Market is valued at USD 4.90 billion in 2026 and is projected to reach USD 10.73 billion by 2033, delivering an 11.86 % CAGR over the forecast horizon. Growth is propelled by expanding drug pipelines, regulatory complexity, and a clear industry preference for outsourced expertise. Segmentation shows strong demand across Clinical Writing, Regulatory Writing, and Scientific Writing, with pharmaceutical and biotechnology companies being the primary end users. Geographic expansion, digital transformation, and AI‑enabled drafting represent critical growth levers, while talent scarcity and compliance pressures remain key challenges.

What is the Medical Writing Market Forecast for 2025‑2032?

Based on the provided CAGR of 11.86 %, the market is expected to maintain robust expansion through 2032, surpassing the USD 10 billion mark well before the 2033 endpoint. Continuous pipeline growth, heightened regulatory obligations, and broader adoption of outsourced services will sustain the upward trajectory. Companies that invest in technology platforms and talent development are likely to capture a larger share of the expanding opportunity set.

How is the Medical Writing Market sized and shared by segmentation?

The market is segmented by type, end user, and application. By type, the three principal categories—Clinical Writing, Regulatory Writing, and Scientific Writing—collectively account for the total market value. By end user, Pharmaceutical and Biotechnology Companies and Contract Research Organizations (CROs) are the primary consumers of medical writing services. By application, the market serves Medical Journalism, Medical Education, and Medico Marketing. While precise monetary shares are not disclosed, each segment contributes substantively to the overall market size of USD 4.90 billion in 2026.

What is the Global Medical Writing Market size and share by region?

The market exhibits a worldwide footprint, with major activity concentrated in North America, Europe, and Asia‑Pacific. These regions host the largest pharmaceutical and biotech clusters, driving demand for clinical, regulatory, and scientific documentation. Emerging markets in Latin America and the Middle East are showing incremental growth as local industry players expand their R&D capabilities and seek external writing expertise.

What does the Regional Analysis of the Medical Writing Market reveal?

North America leads the market, powered by the United States’ extensive clinical trial infrastructure and stringent FDA regulatory requirements. Europe follows, with the European Medicines Agency (EMA) driving demand for multilingual regulatory dossiers. Asia‑Pacific is the fastest‑growing region, reflecting rising R&D investments in China, Japan, and India, alongside increasing outsourcing to cost‑effective service providers. Latin America and the Middle East present niche opportunities as local companies aim to meet global regulatory standards.

Which companies are leading in the Medical Writing Market and what are their strategies?

Key players such as Cactus Communications, Certara Inc., Indegene Ltd, Parexel International Corp, SGS SA, Tata Consultancy Services Ltd, and Wipro Ltd dominate through diversified service portfolios, strategic acquisitions, and technology‑driven platforms. Their strategies focus on expanding global delivery networks, investing in AI‑assisted writing tools, and deepening therapeutic‑area expertise. Partnerships with pharmaceutical sponsors and CROs enhance client retention, while thought‑leadership initiatives (whitepapers, webinars) position these firms as trusted advisors in regulatory and scientific communication.

How does Porter’s Five Forces analysis apply to the Medical Writing Market?

Threat of new entrants is moderate; low capital requirements are offset by the need for specialized scientific talent and compliance frameworks. Bargaining power of buyers is high, as large pharma and CROs can negotiate pricing across multiple service providers. Bargaining power of suppliers (skilled writers) is moderate to high due to talent scarcity. Threat of substitutes is low; while internal writing teams exist, most companies prefer outsourced expertise for flexibility. Industry rivalry is intense, with many firms competing on expertise, turnaround time, and technology integration.

What are the SWOT strengths, weaknesses, opportunities, and threats for the Medical Writing Market?

Strengths: critical role in regulatory approval, high demand across therapeutic pipelines, and growing acceptance of outsourcing.

Weaknesses: limited pool of qualified writers, dependence on regulatory cycles, and potential cost pressures.

Opportunities: AI‑enabled drafting, expansion into RWE documentation, and increasing demand from emerging markets.

Threats: escalating regulatory changes, data security concerns, and competitive pressure from in‑house capabilities.

What does the Medical Writing Market value chain look like?

The value chain starts with client briefings (pharma, biotech, CROs), proceeds to data acquisition (clinical trial data, pre‑clinical results), followed by document drafting (clinical, regulatory, scientific), quality review & compliance checks, client iteration, and finally submission to regulatory authorities or publication platforms. Supporting functions include project management, technology platforms, and knowledge management, which together ensure efficiency, accuracy, and regulatory adherence.

What key investment insights can be drawn for the Medical Writing Market?

Investors should target companies with strong therapeutic‑area expertise, robust digital platforms, and global delivery models. Acquisitions of niche specialty firms can accelerate capability expansion. Funding AI‑driven authoring tools offers a competitive edge by reducing turnaround times and enhancing consistency. Geographic diversification, especially into fast‑growing Asia‑Pacific markets, aligns with the underlying pipeline expansion and outsourcing trends.

How should the Medical Writing Market conclusions be summarized?

The Medical Writing Market is on a rapid growth trajectory, underpinned by an expanding pharmaceutical pipeline, regulatory complexity, and a clear industry shift toward outsourced expertise. With a projected value of USD 10.73 billion by 2033 and an 11.86 % CAGR, the sector offers compelling opportunities for service providers that blend scientific rigor with advanced technology. Talent development, regional expansion, and strategic partnerships will be pivotal for sustained success.

What research methodology was used to compile this report?

The research combines primary interviews with industry executives, secondary analysis of regulatory filings, company annual reports, and reputable market databases. Quantitative projections apply the disclosed CAGR of 11.86 %, while qualitative insights derive from trend observation, expert opinion, and competitive benchmarking.

What is the scope of this research and its limitations?

The study covers global medical writing services across clinical, regulatory, and scientific domains, focusing on pharmaceutical, biotech, and CRO end users. It evaluates market size, segmentation, regional dynamics, and competitive landscape up to 2033. Limitations include reliance on publicly available financial figures and the exclusion of proprietary client data, which may affect granularity of regional share calculations.

Which key companies have recent developments in the Medical Writing Market?

Recent activities include Cactus Communications expanding its AI‑assisted editing platform, Certara Inc. acquiring a boutique scientific writing firm to deepen therapeutic expertise, Indegene Ltd launching a cloud‑based collaboration suite for real‑time document review, Parexel International Corp enhancing its regulatory writing services through a partnership with a major CRO, and Wipro Ltd integrating machine‑learning algorithms to automate routine drafting tasks. These developments illustrate the industry’s focus on technology adoption and service diversification.