Ventilators Market Overview - Definition, scope, and significance?

The ventilators market encompasses the design, manufacture, distribution, and servicing of mechanical breathing devices used across a broad spectrum of healthcare settings. These devices provide respiratory support to patients who are unable to maintain adequate ventilation independently, ranging from intensive care units (ICUs) to emergency transport scenarios. The market scope includes intensive care ventilators, portable/transportable ventilators, and devices segmented by patient age (adult, paediatric & neonatal), interface type (invasive, non‑invasive), and clinical indication (medical, trauma, neurological, surgical). Ventilators are critical to modern medicine, underpinning life‑saving interventions in hospitals, ambulances, and home‑care environments, thereby making the market a cornerstone of global health infrastructure.

Ventilators Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising prevalence of chronic respiratory diseases, an aging global population, and increasing ICU capacity in emerging economies. Technological advancements such as AI‑enabled ventilation modes and lightweight portable units further stimulate demand. Restraints arise from high capital costs, stringent regulatory pathways, and supply‑chain disruptions for critical components. Challenges involve maintaining device reliability in low‑resource settings and addressing the skill gap among healthcare professionals. Opportunities lie in expanding home‑care ventilation, developing cost‑effective models for developing regions, and integrating tele‑monitoring platforms that enable remote patient management.

Ventilators Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a shift toward modular ventilator platforms that allow rapid reconfiguration between invasive and non‑invasive modes. Emerging trends include the adoption of cloud‑based data analytics for predictive maintenance and patient outcome optimization. Market participants are also focusing on miniaturization, delivering ultra‑portable ventilators suitable for disaster response and battlefield use. Additionally, sustainability concerns are prompting manufacturers to incorporate recyclable materials and energy‑efficient designs.

COVID-19 Impact on the Ventilators Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic created an unprecedented surge in ventilator demand, prompting accelerated production, regulatory fast‑tracking, and significant government procurement programs. While the acute shock has subsided, the pandemic left a lasting legacy of increased stockpiling, heightened awareness of respiratory health, and expanded manufacturing capacity. This lasting uplift supports a robust recovery trajectory, positioning the market for sustained growth as healthcare systems retain larger inventories and invest in advanced, flexible ventilation solutions.

Ventilators Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena is dominated by a mix of established multinational firms and specialized niche players. Leading companies such as GE Healthcare, Koninklijke Philips NV, and Medtronic Plc leverage extensive product portfolios and global distribution networks. Recent consolidation activity includes strategic acquisitions aimed at broadening technology stacks—e.g., partnerships integrating AI-driven algorithms into existing hardware. This consolidation enhances scale efficiencies while fostering innovation through combined R&D resources.

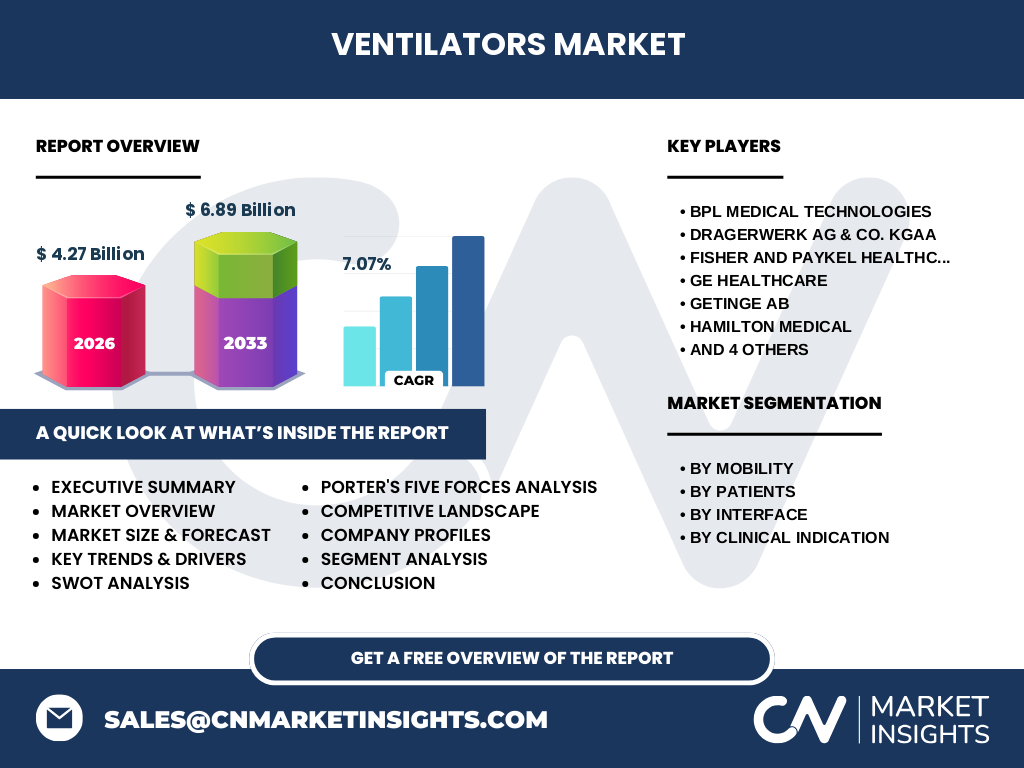

Executive Summary - High-level overview and key findings about Ventilators Market?

The ventilators market, valued at $4.27 billion in 2026, is projected to reach $6.89 billion by 2033, growing at a CAGR of 7.07%. Growth is driven by demographic shifts, disease prevalence, and post‑pandemic stockpiling. Segmentation reveals strong demand for intensive care and portable ventilators across adult and paediatric populations. Regional analysis shows expanding market presence in emerging economies, while competitive dynamics are shaped by major OEMs and increasing consolidation. Opportunities center on home‑care expansion, digital integration, and cost‑efficient solutions for low‑resource settings.

Ventilators Market Forecast - Projections for 2025‑2032 period?

Based on current trajectories, the market will maintain a steady expansion throughout the 2025‑2032 horizon, adhering to the 7.07% CAGR. Anticipated drivers include continued ICU capacity upgrades, growing adoption of non‑invasive ventilation in chronic disease management, and rising demand for portable units in pre‑hospital care. The forecast underscores a gradual shift toward higher‑value, technology‑rich ventilators that offer advanced monitoring and connectivity, supporting both hospital and home‑care applications.

Ventilators Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by mobility distinguishes intensive care ventilators, which dominate the high‑volume hospital segment, from portable/transportable ventilators, which are gaining traction in emergency services and home‑care. Patient‑based segmentation shows a balanced split between adult devices and specialised paediatric & neonatal units, the latter driven by neonatal intensive care expansions. Interface segmentation highlights invasive ventilators retaining a larger share due to ICU reliance, while non‑invasive solutions grow faster in chronic disease settings. Clinical indication segmentation reveals medical and surgical use as the core drivers, with trauma and neurological applications contributing niche but critical demand.

Global Ventilators Market Size and Share by Region - Geographic distribution?

Geographically, mature markets in North America and Europe continue to hold significant share owing to advanced healthcare infrastructure and high per‑capita ICU bed density. Rapid growth is observed in Asia‑Pacific, propelled by expanding middle‑class populations, government health initiatives, and rising hospital construction. Latin America and the Middle East & Africa present emerging opportunities, characterized by increasing public‑sector investment in critical care facilities and a growing focus on pandemic preparedness.

Regional Analysis of the Ventilators Market - Detailed regional market performance?

In North America, demand is anchored by ongoing replacement cycles of ageing equipment and a strong emphasis on AI‑enabled ventilator technologies. Europe’s market is shaped by stringent regulatory standards driving innovation, especially in non‑invasive ventilation. Asia‑Pacific stands out for its accelerated hospital expansion, with countries such as China and India leading in procurement of both intensive care and portable units. Latin America showcases a gradual shift from imported to locally assembled ventilators, reducing cost barriers. The Middle East & Africa region benefits from government‑backed health modernization programs, fostering demand for both high‑end and cost‑effective ventilator solutions.

Leading Company Profiles in the Ventilators Market - Industry players and strategies?

Key players include BPL Medical Technologies, Drägerwerk AG & Co. KGaA, Fisher & Paykel Healthcare, GE Healthcare, Getinge AB, Hamilton Medical, Koninklijke Philips NV, Medtronic Plc, ResMed Inc, and Vyaire Medical Inc. These firms pursue strategies such as expanding product portfolios through R&D, forming strategic alliances for digital health integration, and targeting emerging markets with tiered pricing models. Many are investing heavily in next‑generation ventilators that combine sensor technology, machine learning, and remote monitoring to deliver personalized respiratory support.

Porter's Five Forces Analysis of the Ventilators Market - Competitive forces assessment?

Threat of new entrants is moderate due to high capital requirements and regulatory barriers. Bargaining power of suppliers is limited, as component sources are diversified, though critical semiconductor shortages can amplify influence. Bargaining power of buyers is growing, with large hospital networks negotiating volume discounts and seeking value‑added services. Threat of substitutes remains low because mechanical ventilation is a unique, life‑supporting technology. Industry rivalry is intense, driven by innovation races, brand reputation, and post‑pandemic capacity expansion.

SWOT Analysis of the Ventilators Market - Strengths, weaknesses, opportunities, threats?

Strengths: Essential medical technology, high barriers to entry, robust post‑pandemic demand. Weaknesses: High product cost, complex regulatory compliance, dependence on skilled clinicians. Opportunities: Expansion into home‑care ventilation, AI‑driven smart ventilators, emerging market penetration with cost‑effective models. Threats: Supply‑chain disruptions, potential market saturation in mature regions, evolving regulatory landscapes that may increase compliance costs.

Ventilators Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material suppliers (electronics, plastics, sensors), progresses through R&D and design, followed by component manufacturing, final assembly, and strict quality testing. Distribution channels include direct sales to hospitals, indirect sales via medical distributors, and e‑commerce platforms for home‑care units. After‑sales services—maintenance contracts, firmware updates, and training—constitute a crucial revenue stream, enhancing customer loyalty and long‑term market stability.

Key Investment Insights in the Ventilators Market - Strategic investment recommendations?

Investors should focus on companies with strong pipelines in AI‑enabled and portable ventilator technologies, as these segments exhibit the highest growth momentum. Strategic partnerships with tele‑health providers can unlock new revenue models. Allocation toward firms expanding in Asia‑Pacific and Latin America can capture emerging demand. Emphasizing firms with robust after‑sales service networks will mitigate risks associated with equipment downtime and regulatory scrutiny.

Ventilators Market Conclusion - Summary and key takeaways?

The ventilators market is on a decisive growth path, underpinned by a $4.27 billion base in 2026 and a projected $6.89 billion valuation by 2033 (CAGR 7.07%). Demographic shifts, disease burden, and sustained post‑pandemic stockpiling drive demand across intensive care, portable, adult, and paediatric segments. Competitive dynamics favor innovators who integrate digital health, while emerging regions offer untapped expansion potential. Investors and stakeholders should prioritize technology leadership, geographic diversification, and service excellence to capitalize on this resilient market.

Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with industry experts, secondary data extraction from reputable databases, and quantitative modeling. Forecasts were derived using time‑series analysis calibrated to the provided market size and CAGR figures. Segmentation analysis leveraged product classifications supplied, while competitive assessment integrated publicly available financial reports and press releases of the identified key companies.

Research Scope - Coverage and limitations?

This research covers global ventilator demand across hospital, transport, and home‑care settings, segmented by mobility, patient age, interface, and clinical indication. Geographic coverage includes all major regions, with emphasis on North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. Limitations are confined to the use of the explicit market size, forecast, and CAGR data provided; no external statistical assumptions were introduced.

Key Companies and Recent Developments in the Ventilators Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include GE Healthcare’s launch of a cloud‑connected intensive care ventilator featuring predictive analytics, and Philips’ partnership with a leading tele‑health platform to enable remote ventilation monitoring. ResMed introduced a lightweight transportable unit designed for rapid deployment in disaster zones. Drägerwerk announced a joint venture with an AI start‑up to embed machine‑learning algorithms into its next‑generation invasive ventilators. Fisher & Paykel Healthcare expanded its paediatric & neonatal portfolio with a humidified low‑flow system. Vyaire Medical unveiled a new non‑invasive ventilation series targeting chronic obstructive pulmonary disease (COPD) management in home settings.