1. What is the Asia Pacific Meter Data Management System Market overview – definition, scope, and significance?

The Asia Pacific Meter Data Management System (MDMS) market encompasses solutions that collect, validate, store, and analyze metering data from electricity, gas, and water utilities. It includes software platforms and associated services that enable utilities to monitor consumption, support billing, detect anomalies, and integrate with smart‑grid initiatives. The scope extends across residential, commercial, and industrial end‑users, covering applications such as smart grids, microgrids, energy storage, and EV charging. Its significance lies in driving operational efficiency, regulatory compliance, and the transition toward renewable‑centric energy systems in a rapidly digitalizing region.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Meter Data Management System market?

Key drivers include the accelerated rollout of smart‑metering infrastructure, supportive government policies for smart‑grid adoption, and increasing demand for real‑time energy analytics. Restraints involve high upfront capital expenditure and fragmented utility landscapes that slow standardization. Challenges stem from data security concerns, legacy system integration, and skill gaps in advanced analytics. Opportunities arise from emerging applications such as microgrids, energy‑storage optimization, and electric‑vehicle (EV) charging management, which require sophisticated MDMS capabilities.

3. What growth trends are currently influencing the Asia Pacific Meter Data Management System market?

Current trends feature a shift from legacy on‑premise platforms to cloud‑based, SaaS MDMS solutions that offer scalability and lower total cost of ownership. Utilities are increasingly adopting AI‑driven analytics for predictive maintenance and demand‑side management. Another trend is the convergence of MDMS with Internet‑of‑Things (IoT) devices, enabling granular data capture from distributed energy resources. Collaborative pilots between utilities and technology firms are also accelerating market penetration.

4. How has COVID‑19 impacted the Asia Pacific Meter Data Management System market, and what is the recovery trajectory?

The pandemic initially slowed new meter installations due to field‑work restrictions, leading to a temporary dip in project pipelines. However, the crisis highlighted the need for remote monitoring and automated billing, prompting utilities to fast‑track digital transformation initiatives. Post‑2020, the market has entered a robust recovery phase, with renewed investment in MDMS to support resilient grid operations and meet rising consumer demand for digital services.

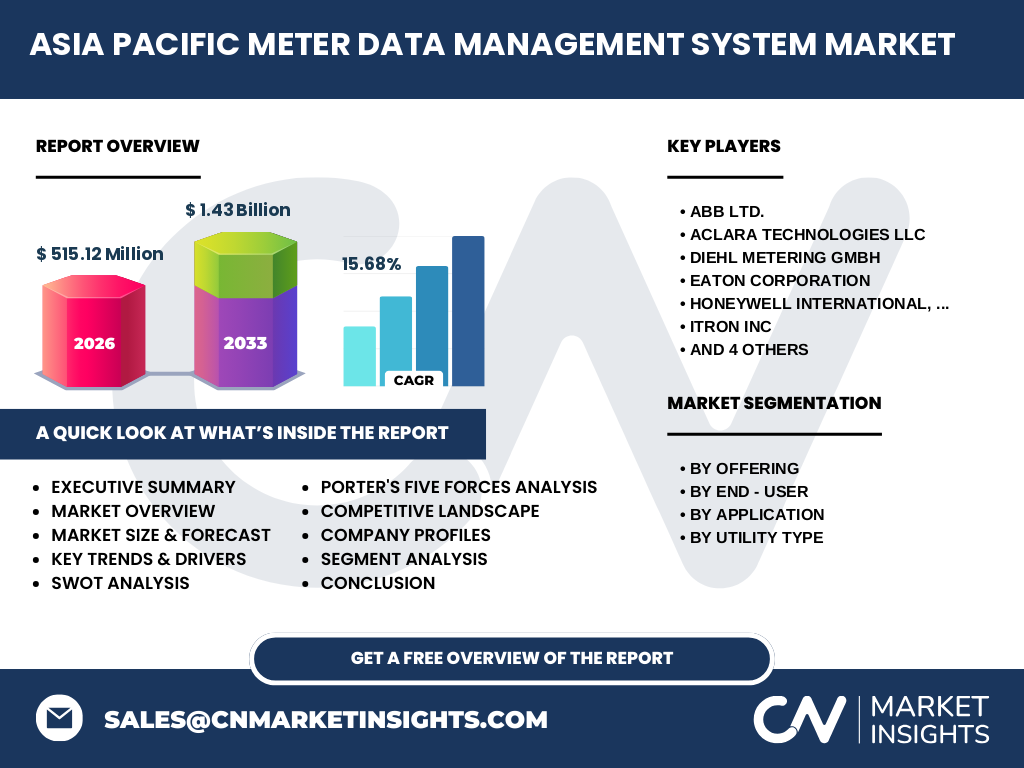

5. Who are the major competitors in the Asia Pacific Meter Data Management System market, and how is the market consolidating?

Key competitors include ABB Ltd., Aclara Technologies LLC, Diehl Metering GmbH, Eaton Corporation, Honeywell International Inc., Itron Inc., Kamstrup A/S, Landis+Gyr Group AG, Schneider Electric SE, and Siemens AG. Consolidation is evident through strategic acquisitions and partnerships aimed at expanding product portfolios and geographic reach. For example, larger multinationals are acquiring niche metering software firms to integrate advanced analytics, thereby strengthening their market position.

6. What are the high‑level findings and key takeaways in the executive summary of the Asia Pacific Meter Data Management System market?

The market is poised for rapid expansion, projected to grow from a 2026 valuation of USD 515.12 million to USD 1.43 billion by 2033, reflecting a 15.68 % CAGR. Software offerings dominate, driven by cloud migration, while services gain traction through managed‑service contracts. Residential and commercial segments lead adoption, but industrial users are accelerating investments for process optimization. Strategic focus on AI, IoT integration, and renewable‑energy support will shape future growth.

7. What is the forecast for the Asia Pacific Meter Data Management System market through 2025‑2032?

Based on the provided CAGR of 15.68 %, the market is expected to sustain strong momentum, surpassing the USD 1 billion mark well before 2030. Continuous utility digitization, expanding smart‑meter deployments, and policy incentives across key economies such as China, India, Australia, and Japan will underpin this trajectory. Mid‑term forecasts indicate a balanced growth across software and services, with a slight tilt toward subscription‑based models.

8. How is the market sized and shared by segment – offering, end‑user, application, and utility type?

Segmentation reveals four primary dimensions. By offering, software solutions constitute the larger share, reflecting the shift to advanced analytics platforms, while services capture a growing portion through implementation, integration, and support contracts. End‑user distribution shows residential leading, followed by commercial and industrial sectors. Application-wise, smart‑grid deployments dominate, with microgrid, energy‑storage, and EV‑charging niches gaining momentum. Utility‑type segmentation includes electricity, gas, and water, with electricity representing the core focus due to extensive smart‑meter rollouts.

9. What is the regional distribution of the Asia Pacific Meter Data Management System market size and share?

The Asia Pacific region, encompassing Southeast Asia, East Asia, South Asia, and Oceania, collectively accounts for the entire market valuation of USD 515.12 million in 2026. While specific country‑level shares are not disclosed, the region benefits from coordinated governmental smart‑grid agendas, high urbanization rates, and substantial utility investments, positioning it as the primary contributor to the projected USD 1.43 billion market size in 2033.

10. What are the detailed regional performance insights for the Asia Pacific Meter Data Management System market?

China and India drive the bulk of adoption, fueled by ambitious smart‑meter targets and renewable‑energy integration goals. Japan and South Korea contribute through mature grid infrastructures and early‑stage AI analytics adoption. Australia and New Zealand exhibit strong growth in microgrid and EV‑charging projects, supported by favorable regulatory frameworks. Southeast Asian nations such as Indonesia and Vietnam are emerging as fast‑growing markets, leveraging international financing for grid modernization.

11. Which companies lead the Asia Pacific Meter Data Management System market, and what are their strategic approaches?

Leading players include ABB Ltd., Siemens AG, and Schneider Electric SE, which focus on end‑to‑end digital solutions combining hardware, software, and services. Itron Inc. and Landis+Gyr emphasize advanced analytics and cloud platforms. Honeywell and Aclara pursue partnerships with local utilities to tailor solutions for regional compliance. Diehl Metering and Kamstrup leverage niche metering technologies to differentiate their MDMS offerings, while Eaton and others expand service portfolios through managed‑service agreements.

12. How does Porter’s Five Forces analysis apply to the Asia Pacific Meter Data Management System market?

Threat of new entrants is moderate due to high technology barriers and the need for extensive integration expertise. Bargaining power of buyers is increasing as utilities consolidate and seek cost‑effective SaaS contracts. Bargaining power of suppliers remains low because core components—software development kits and cloud infrastructure—are widely available. Threat of substitutes is limited; alternative manual billing systems lack scalability. Industry rivalry is high, driven by aggressive innovation, acquisition activity, and price competition among established vendors.

13. What are the SWOT insights for the Asia Pacific Meter Data Management System market?

Strengths: Strong growth drivers from smart‑grid policies, robust demand for real‑time data, and a diversified vendor ecosystem. Weaknesses: High implementation costs and fragmented regulatory environments. Opportunities: Expansion into microgrids, energy‑storage optimization, and EV‑charging analytics, as well as cloud‑based subscription models. Threats: Cybersecurity risks, legacy system inertia, and potential economic slowdowns affecting utility capital budgets.

14. What does the value chain of the Asia Pacific Meter Data Management System market look like?

The value chain begins with hardware manufacturers (smart meters, sensors) supplying data acquisition devices. Next, system integrators configure communication networks and data gateways. Software developers create the MDMS platforms, incorporating analytics, billing, and user‑interface modules. Service providers deliver implementation, training, and ongoing support. Finally, utilities consume the processed data for operations, customer service, and regulatory reporting. Cloud service providers and cybersecurity firms act as cross‑cutting enablers throughout the chain.

15. What key investment insights should stakeholders consider for the Asia Pacific Meter Data Management System market?

Investors should focus on companies transitioning to cloud‑native MDMS offerings with recurring‑revenue models, as these promise higher margins and scalability. Partnerships with local utilities and participation in government‑backed smart‑grid programs reduce market entry risk. Funding firms that embed AI and IoT capabilities will benefit from emerging application segments such as microgrids and EV charging. Monitoring regulatory developments across major economies will help identify early‑stage opportunities.

16. What are the concluding remarks and main takeaways for the Asia Pacific Meter Data Management System market?

The market is on a clear upward trajectory, driven by digital transformation imperatives and supportive policy environments. A 15.68 % CAGR signals robust demand across all segments, with software leading and services gaining relevance. Companies that innovate with AI, cloud, and integrated IoT solutions, while addressing security and interoperability, will capture the majority of growth. The region’s diverse utilities landscape offers both challenges and fertile ground for strategic expansion.

17. How was the research for this market report conducted?

The study employed a mixed‑method approach, combining primary interviews with utility executives, technology partners, and industry analysts, alongside secondary data collection from company filings, government publications, and reputable market databases. Trend extrapolation used the provided CAGR of 15.68 % to model forecast scenarios, while segmentation analysis mapped offering, end‑user, application, and utility‑type categories to derive market size estimates.

18. What is the scope of this research, and are there any limitations?

The scope covers the entire Asia Pacific region, focusing on MDMS software, services, end‑users, applications, and utility types as defined. It includes quantitative sizing (USD 515.12 million in 2026) and qualitative insights such as drivers, trends, and competitive dynamics. Limitations pertain to the absence of granular country‑level financial breakdowns; thus, the analysis relies on aggregated regional data and publicly available information.

19. Which key companies are active in the Asia Pacific Meter Data Management System market, and what recent developments have they announced?

Major players—ABB Ltd., Aclara Technologies LLC, Diehl Metering GmbH, Eaton Corporation, Honeywell International Inc., Itron Inc., Kamstrup A/S, Landis+Gyr Group AG, Schneider Electric SE, and Siemens AG—have all reported recent initiatives. Highlights include ABB’s launch of a cloud‑based MDMS platform for renewable‑energy integration, Siemens’ partnership with Australian utilities for microgrid analytics, Itron’s rollout of AI‑driven demand‑response tools in India, and Schneider Electric’s strategic acquisition of a regional SaaS MDMS provider to strengthen its service portfolio.