What is the Asia Pacific Micro Mobile Data Center Market Overview – definition, scope, and significance?

The Asia Pacific Micro Mobile Data Center (MMDC) market encompasses compact, pre‑engineered data center solutions that can be rapidly deployed on wheels, trailers, or modular frames to provide compute, storage, and networking capabilities at the edge. These units range from small 25 RU racks to larger configurations exceeding 40 RU and serve diverse applications such as instant‑DC, high‑density networks, remote office support, and mobile computing. Their significance lies in enabling low‑latency services, disaster recovery, and rapid scalability for enterprises across the fast‑growing Asia‑Pacific region.

What are the key drivers, restraints, challenges, and opportunities influencing the Asia Pacific Micro Mobile Data Center Market?

Drivers include the surge in data traffic, 5G rollout, and the need for edge‑centric infrastructure to support IoT and AI workloads. Rapid urbanization and the growth of sectors such as BFSI, retail, and healthcare further fuel demand. Restraints stem from high upfront capital costs and regulatory hurdles in certain countries. Challenges involve logistics of transporting large units and ensuring reliable power in remote sites. Opportunities arise from government initiatives promoting smart cities and the increasing adoption of temporary or disaster‑recovery data centers.

What growth trends are currently shaping the Asia Pacific Micro Mobile Data Center Market?

Trend 1: Migration toward containerized and trailer‑based MMDCs for faster deployment. Trend 2: Integration of renewable energy sources and battery‑back‑up to meet sustainability goals. Trend 3: Adoption of AI‑driven monitoring tools to enhance operational efficiency. Trend 4: Expansion of services beyond telecom, entering manufacturing and logistics for on‑site data processing.

How has COVID‑19 impacted the Asia Pacific Micro Mobile Data Center Market and what is the recovery trajectory?

The pandemic accelerated digital transformation, prompting enterprises to decentralize IT assets and adopt mobile data centers for remote work support and business continuity. Initial supply‑chain disruptions slowed deliveries, but post‑2022 the market rebounded strongly as organizations prioritized resilient edge infrastructure. Recovery is now evident in sustained investment, reflected in the robust forecast through 2033.

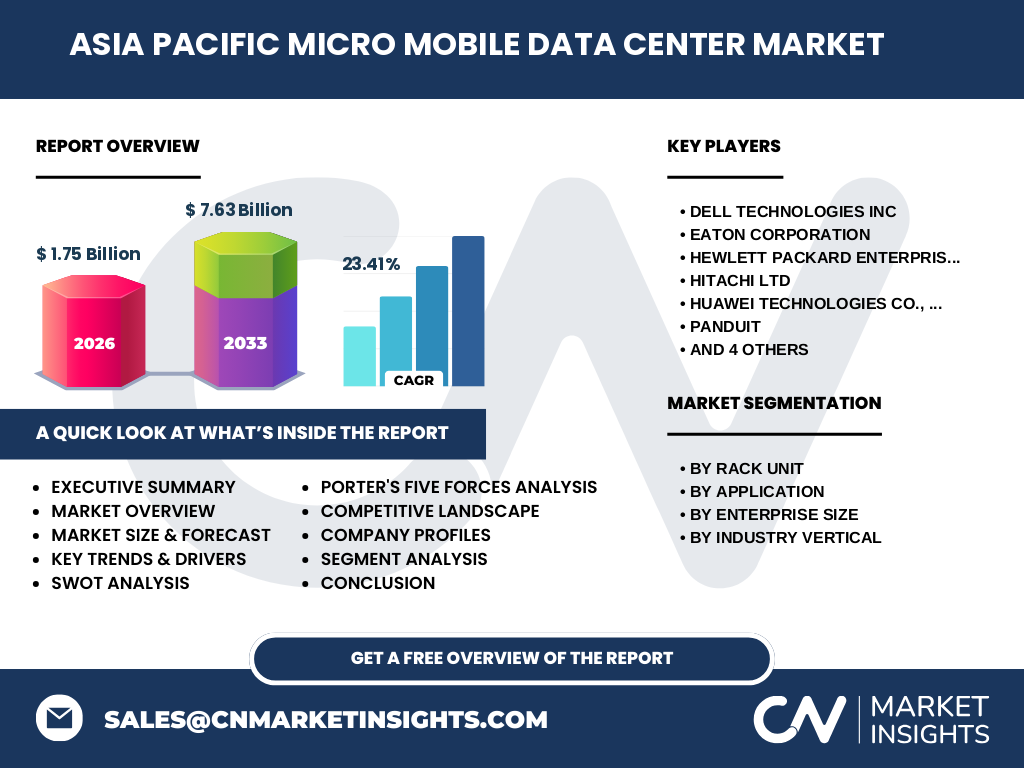

What does the competitive landscape of the Asia Pacific Micro Mobile Data Center Market look like?

The market is fragmented with several global and regional players vying for market share. Major competitors include Dell Technologies, Eaton Corporation, Hewlett Packard Enterprise (HPE), Hitachi, Huawei, Panduit, Rittal, Schneider Electric, VERTIV, and Zellabox. Companies are pursuing strategic partnerships, expanding service portfolios, and investing in R&D to differentiate their modular solutions, leading to moderate consolidation through joint ventures and acquisitions.

What are the key findings in the executive summary of the Asia Pacific Micro Mobile Data Center Market?

The market was valued at USD 1.75 billion in 2026 and is projected to reach USD 7.63 billion by 2033, delivering a CAGR of 23.41 %. Growth is driven by edge‑computing demand, 5G expansion, and sectoral adoption across BFSI, retail, healthcare, IT & telecom, and manufacturing. Large enterprises lead adoption, while SMEs increasingly seek scalable solutions. Competitive dynamics are intensifying, with innovation focused on sustainability and rapid deployment.

What are the market forecasts for the Asia Pacific Micro Mobile Data Center Market from 2025 to 2032?

Based on the provided CAGR of 23.41 %, the market is expected to expand from the 2026 baseline of USD 1.75 billion to approximately USD 7.63 billion by 2033. This trajectory indicates sustained double‑digit growth throughout 2025‑2032, underscoring strong demand for edge‑oriented, mobile data center solutions across the region.

How is the market sized and shared by segmentation?

By Rack Unit, the market is split among three size categories: up to 25 RU, 25‑40 RU, and above 40 RU, catering to varying capacity needs. Application‑wise, segments include instant DC & retrofit, high‑density networks, remote office support, and mobile computing. Enterprise size segmentation distinguishes large enterprises from SMEs, while industry verticals cover BFSI, retail, healthcare, IT & telecom, and manufacturing. Each segment contributes to the overall market growth by addressing specific use cases.

What is the global Asia Pacific Micro Mobile Data Center market size and share by region?

The Asia Pacific region represents the primary geographic focus of this report, accounting for the entire market valuation of USD 1.75 billion in 2026 and the projected USD 7.63 billion in 2033. While the study concentrates on Asia Pacific, comparable growth patterns are observed in other regions, positioning the area as a leading hub for MMDC adoption.

What does the regional analysis of the Asia Pacific Micro Mobile Data Center Market reveal?

East Asia (China, Japan, South Korea) leads in deployment owing to advanced telecom infrastructure and manufacturing bases. Southeast Asia (Singapore, Malaysia, Indonesia) shows rapid uptake driven by smart‑city projects and mobile broadband expansion. Oceania, particularly Australia, contributes through enterprise‑level deployments in mining and remote operations. Each sub‑region demonstrates distinct drivers but shares a common trend toward edge‑first architectures.

Who are the leading companies in the Asia Pacific Micro Mobile Data Center Market and what are their strategies?

Key players include Dell Technologies, Eaton, HPE, Hitachi, Huawei, Panduit, Rittal, Schneider Electric, VERTIV, and Zellabox. Strategies focus on expanding product portfolios with higher‑density rack designs, enhancing energy‑efficiency features, and forming ecosystem partnerships with telecom operators. Many are investing in localized manufacturing and service centers to improve after‑sales support and reduce lead times.

How does Porter’s Five Forces analysis apply to the Asia Pacific Micro Mobile Data Center Market?

Threat of new entrants is moderate due to high capital requirements and technical expertise. Bargaining power of suppliers is relatively low as component sources are diversified. Buyers wield strong influence, especially large enterprises demanding customized solutions. The threat of substitutes is limited; traditional stationary data centers cannot match the mobility and rapid deployment of MMDCs. Competitive rivalry is intense, with frequent product launches and price competition.

What are the SWOT insights for the Asia Pacific Micro Mobile Data Center Market?

Strengths: High growth rate, flexibility, and alignment with edge computing trends. Weaknesses: Elevated initial investment and logistical complexities. Opportunities: Government smart‑city funding, renewable‑energy integration, and expansion into emerging verticals like autonomous logistics. Threats: Regulatory variations across countries and potential supply‑chain disruptions.

What does the value chain analysis reveal about the Asia Pacific Micro Mobile Data Center Market?

The value chain begins with component suppliers (servers, cooling, power modules), moves to system integrators who assemble the modular units, followed by logistics providers handling transportation to sites. Service layers include installation, monitoring, and maintenance, often offered by the OEM or third‑party contractors. End‑users span enterprises and service providers that operate the MMDCs for specific workloads.

What key investment insights can be drawn for the Asia Pacific Micro Mobile Data Center Market?

Investors should focus on companies with strong R&D pipelines for high‑density, energy‑efficient designs and those establishing regional service networks. Partnerships with telecom carriers and participation in smart‑city initiatives can accelerate market penetration. Funding in renewable‑energy integration within MMDCs offers differentiation and aligns with sustainability mandates.

What conclusions can be drawn about the Asia Pacific Micro Mobile Data Center Market?

The market is on a clear upward trajectory, moving from a niche solution to a mainstream component of edge infrastructure. Robust growth, driven by 5G, IoT, and industry digitalization, is supported by a diverse set of applications and verticals. Competitive intensity will foster innovation, particularly in sustainability and rapid deployment capabilities.

What research methodology was used for this market study?

The study employed a mixed‑method approach, combining primary interviews with industry experts, secondary data collection from reputable databases, and quantitative modeling to project future market size. Trend analysis, competitive benchmarking, and scenario planning were applied to ensure reliability of the forecasts.

What is the scope of this research?

The research covers the Asia Pacific MMDC market from 2026 to 2033, segmenting by rack unit size, application, enterprise size, and industry vertical. Geographic coverage includes major sub‑regions within Asia Pacific. Limitations are confined to publicly available data and disclosed company information.

Which key companies and recent developments are shaping the Asia Pacific Micro Mobile Data Center Market?

Leading firms such as Dell Technologies, HPE, and Huawei have announced new high‑density trailer solutions with integrated solar power options. Schneider Electric launched a modular cooling system tailored for tropical climates. VERTIV reported a strategic partnership with a Southeast Asian telecom operator to provide instant‑DC services. Hitachi introduced a rapid‑deployment MMDC for disaster‑recovery, while Rittal unveiled a scalable rack system targeting SMEs.