1. What is the Asia Pacific Deep Learning Chip Market Overview – definition, scope, and significance?

The Asia Pacific Deep Learning Chip Market comprises semiconductor devices specifically engineered to accelerate deep‑learning workloads such as neural‑network inference and training. It includes GPUs, ASICs, FPGAs, and CPUs, as well as advanced packaging technologies like System‑on‑Chip (SoC), System‑in‑Package (SiP), and Multi‑chip Modules (MCM). The scope extends to all end‑use verticals where artificial‑intelligence (AI) solutions are deployed, ranging from media & advertising to automotive. The market’s significance lies in its role as the hardware backbone for AI transformation across the region, enabling faster processing, lower latency, and energy‑efficient deployment of AI models that power everything from autonomous vehicles to predictive finance.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Asia Pacific Deep Learning Chip Market?

Key drivers include explosive AI adoption across industries, strong government AI initiatives in China, Japan, South Korea, and India, and rising data‑center capacity fueled by cloud providers. The surge in edge computing and 5G rollout further pushes demand for power‑efficient chips. Major restraints involve high R&D costs, intellectual‑property complexities, and supply‑chain bottlenecks for advanced packaging materials. Challenges stem from talent scarcity in AI‑hardware design and geopolitical tensions affecting cross‑border technology transfers. Opportunities arise from emerging applications such as generative AI, AI‑enabled healthcare diagnostics, and the transition to customized ASIC solutions that promise superior performance‑per‑watt.

3. What growth trends are currently influencing the Asia Pacific Deep Learning Chip Market?

Current trends include a shift toward heterogeneous computing architectures that combine GPUs with ASICs for optimized workloads. Edge AI chips are gaining traction as enterprises move processing closer to data sources to reduce latency. Another trend is the adoption of advanced packaging (SoC, SiP, MCM) to overcome traditional Moore’s Law limits, delivering higher bandwidth and integration density. Finally, open‑source AI frameworks are driving a broader developer ecosystem, encouraging semiconductor vendors to provide optimized libraries and toolchains.

4. How has COVID‑19 impacted the Asia Pacific Deep Learning Chip Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and delayed capital spending, but it also accelerated digital transformation as organizations sought automation and remote‑work solutions. AI workloads surged, prompting data‑center expansion and higher demand for deep‑learning chips. Post‑2020, the market rebounded strongly, with a rapid build‑out of cloud infrastructure and a pronounced shift to edge AI in health and logistics, positioning the region for sustained growth.

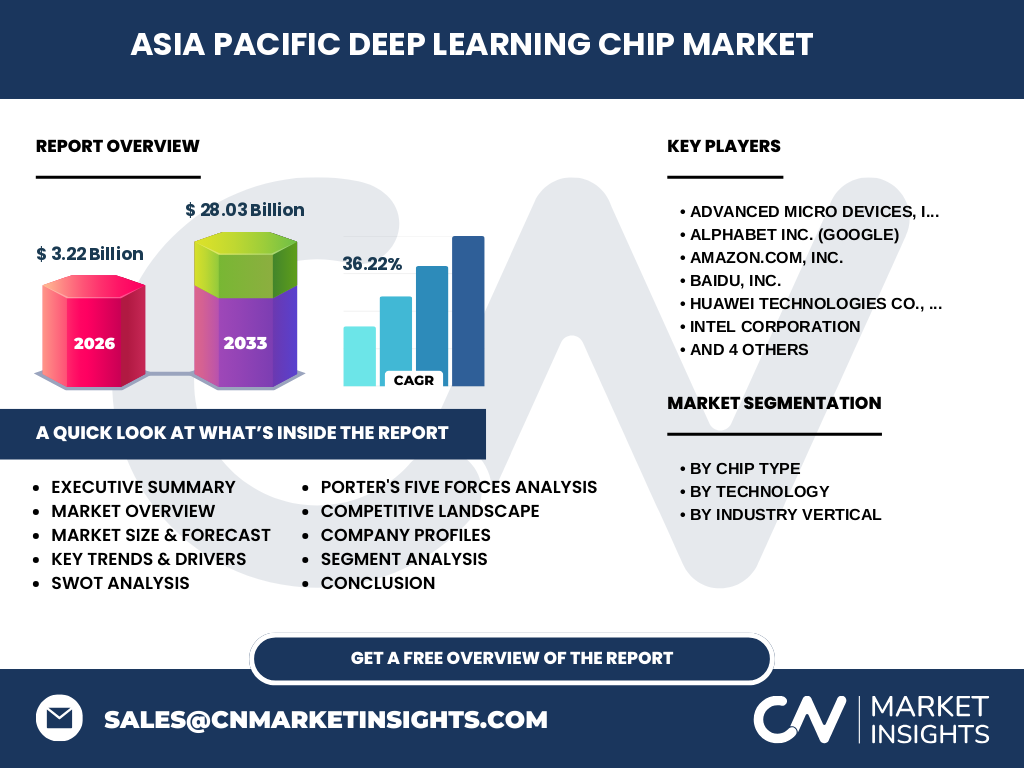

5. Who are the major competitors in the Asia Pacific Deep Learning Chip Market and how is the competitive landscape evolving?

Leading players include NVIDIA Corporation, Advanced Micro Devices (AMD), Intel Corporation, Huawei Technologies, Samsung Electronics, Qualcomm, Xilinx, Alphabet (Google) with its Tensor Processing Units, Amazon Web Services with custom ASICs, and Baidu. The landscape is marked by strategic acquisitions (e.g., Xilinx’s integration into AMD), joint R&D collaborations, and aggressive IP‑portfolio expansion. Competition intensifies around performance benchmarks, power efficiency, and integration of AI software stacks.

6. What are the key findings highlighted in the executive summary of the Asia Pacific Deep Learning Chip Market?

The market is projected to expand from a 2026 valuation of $3.22 billion to $28.03 billion by 2033, delivering a robust CAGR of 36.22 % over the forecast horizon. Growth is driven by cross‑industry AI adoption, rapid expansion of data‑center and edge infrastructure, and the emergence of advanced packaging solutions. Competitive dynamics are shifting toward specialization, with ASIC and customized FPGA solutions gaining market share against traditional GPUs. The region’s strong manufacturing base and supportive policy environment underpin the upward trajectory.

7. What are the forecast expectations for the Asia Pacific Deep Learning Chip Market from 2025 to 2032?

Based on the provided CAGR of 36.22 %, the market is expected to maintain double‑digit expansion throughout 2025‑2032, consistently outpacing broader semiconductor growth. Forecasts indicate sustained investment in AI‑ready data centres, heightened demand for edge AI in smart cities, and an accelerating pipeline of AI‑driven services that will fuel chip consumption across all verticals.

8. How is the market sized and shared by chip type, technology, and industry vertical?

Segmentation by chip type includes GPU, ASIC, FPGA, and CPU. By technology, the market is divided into System‑on‑Chip, System‑in‑Package, and Multi‑chip Module solutions. Industry verticals span Media & Advertising, BFSI, IT & Telecom, Retail, Healthcare, and Automotive & Transportation. While exact numeric shares are not disclosed, the trend shows GPUs currently dominate the data‑center segment, ASICs are gaining prominence in edge and specialized workloads, and advanced packaging technologies are increasingly adopted across all chip types to meet performance and power targets.

9. What is the geographic distribution of the Asia Pacific Deep Learning Chip Market?

The market covers key sub‑regions such as Greater China, Japan, South Korea, India, and the ASEAN economies. China remains the largest contributor, driven by massive AI research investment and domestic chip design capabilities. Japan and South Korea contribute strong manufacturing capacity, while India’s fast‑growing digital economy creates expanding demand for cost‑effective AI solutions.

10. How do individual regions within Asia Pacific perform in the deep learning chip market?

Greater China leads in both design and volume production, supported by government subsidies and a vibrant AI start‑up ecosystem. Japan focuses on high‑precision manufacturing and automotive AI applications. South Korea emphasizes memory‑centric AI hardware and 5G integration. India’s growth is propelled by the services sector and increasing adoption of AI in fintech and e‑commerce. ASEAN nations, particularly Singapore and Vietnam, are emerging hubs for AI start‑ups and edge deployments.

11. Which companies are leading the Asia Pacific Deep Learning Chip Market and what are their strategic focuses?

NVIDIA continues to dominate GPU‑based deep‑learning acceleration, expanding its AI software ecosystem. AMD leverages its Ryzen and Instinct product lines, targeting mixed workloads. Intel pursues a heterogeneous portfolio with Xeon processors, Habana Labs ASICs, and FPGA acquisitions. Huawei focuses on AI‑optimized SoCs for both consumer devices and edge servers. Samsung integrates AI accelerators into its Exynos and memory products. Qualcomm drives AI at the edge with Snapdragon processors. Xilinx (now part of AMD) emphasizes adaptable FPGA solutions, while Alphabet and Amazon develop proprietary ASICs for their cloud services. Baidu invests in custom AI chips to power its search and autonomous‑driving platforms.

12. What does Porter’s Five Forces analysis reveal about the Asia Pacific Deep Learning Chip Market?

Threat of new entrants: Moderate – high R&D costs and complex IP barriers limit newcomers, but emerging fabless start‑ups with AI‑focused funding pose a niche risk. Bargaining power of suppliers: High – scarcity of advanced lithography and packaging materials gives suppliers leverage. Bargaining power of buyers: Increasing – large cloud providers and OEMs demand volume discounts and customized solutions. Threat of substitutes: Low to moderate – software optimizations can reduce hardware dependence, yet performance constraints keep specialized chips essential. Industry rivalry: Intense – major players compete on performance per watt, ecosystem integration, and price, driving rapid innovation cycles.

13. What are the SWOT findings for the Asia Pacific Deep Learning Chip Market?

Strengths: Robust AI adoption, strong manufacturing ecosystem, abundant talent pool in certain hubs. Weaknesses: Dependence on a limited number of advanced‑process fabs, geopolitical supply‑chain risks. Opportunities: Growth of generative AI, expansion of edge AI in smart‑city projects, rising demand for AI‑enabled healthcare diagnostics. Threats: Trade restrictions, escalating R&D expenditures, potential market saturation in data‑center GPUs.

14. How does the value chain of the Asia Pacific Deep Learning Chip Market operate?

The value chain begins with chip design (IP cores, architecture), proceeds to fabrication (foundries such as TSMC and SMIC), followed by packaging & testing (advanced SoC/SiP/MCM processes). Next, software enablement (toolkits, SDKs) integrates AI frameworks. Finally, distribution reaches system integrators, OEMs, and cloud service providers. Services like design‑for‑AI, application‑specific optimization, and post‑sale support constitute value‑added layers that differentiate vendors.

15. What investment insights can be drawn for stakeholders interested in the Asia Pacific Deep Learning Chip Market?

Investors should prioritize companies that demonstrate a clear AI‑hardware roadmap, strong IP portfolios, and partnerships with leading cloud platforms. Funding opportunities exist in niche ASIC and FPGA developers targeting edge applications, as well as in firms advancing packaging technologies that unlock higher bandwidth. Allocation toward firms with diversified geographic exposure can mitigate regional supply‑chain risks, while participation in joint R&D consortia can accelerate time‑to‑market for next‑generation AI chips.

16. What are the concluding takeaways from the Asia Pacific Deep Learning Chip Market analysis?

The market is on a rapid expansion trajectory, underpinned by a 36.22 % CAGR and a projected $28.03 billion valuation by 2033. AI‑driven demand across multiple verticals, combined with the region’s manufacturing strengths, positions Asia Pacific as the global epicenter for deep‑learning hardware. Success will depend on mastering advanced packaging, delivering ASIC‑level efficiency, and navigating geopolitical dynamics.

17. Which research methodology was applied to compile this market report?

The study employed a mixed‑method approach, integrating primary interviews with industry executives, secondary data extraction from company filings, analyst reports, and reputable databases. Quantitative forecasts used compound annual growth rate modeling based on the provided baseline (2026) and forward projection (2027‑2033). Qualitative insights derived from trend analysis, competitive benchmarking, and expert opinion synthesis.

18. What is the scope of this research and its coverage limitations?

The scope encompasses chip types, packaging technologies, and end‑use verticals relevant to deep‑learning applications within the Asia Pacific region. It covers market size, growth forecasts, competitive dynamics, and value‑chain assessment. Limitations include reliance on publicly disclosed financials and the absence of granular market‑share percentages beyond the supplied aggregate figures.

19. Which key companies are highlighted and what recent developments have they announced?

NVIDIA unveiled its Hopper architecture, targeting massive AI training workloads. AMD launched the MI300 series, integrating GPU and CPU cores for heterogeneous AI processing. Intel announced its next‑gen Habana Gaudi2 ASICs for data‑center inference. Huawei introduced the Ascend 910 Pro, emphasizing energy efficiency for edge AI. Samsung revealed AI‑enhanced Exynos chips with embedded neural‑processing units. Qualcomm expanded its Snapdragon AI Engine to support on‑device generative AI. Xilinx (AMD) introduced adaptive AI accelerators for low‑latency edge inference. Alphabet rolled out newer TPU v5e pods for its cloud AI services, while Amazon disclosed a custom Graviton‑based ASIC for inference acceleration in AWS. Baidu launched the Kunlun chip series, focusing on autonomous driving and cloud AI workloads.