What is the North America Deep Learning Chip Market Overview – Definition, scope, and significance?

The North America Deep Learning Chip Market comprises semiconductor components specifically engineered to accelerate neural network training and inference across a range of applications. The market scope includes GPUs, ASICs, FPGAs, and CPUs, as well as system‑on‑chip (SoC), system‑in‑package (SiP), and multi‑chip module (MCM) technologies. Its significance lies in powering AI‑driven services—such as autonomous vehicles, intelligent healthcare diagnostics, and real‑time recommendation engines—thereby cementing North America’s role as a hub for AI innovation and high‑performance computing.

What are the main drivers, restraints, challenges, and opportunities influencing the North America Deep Learning Chip Market?

Key drivers include escalating AI adoption in cloud data centers, the surge in edge‑computing deployments, and strong R&D investments from leading chip manufacturers. Restraints stem from high development costs and supply‑chain bottlenecks for advanced lithography. Challenges involve intense competition among GPU and ASIC vendors and the need for energy‑efficient designs. Opportunities arise from emerging verticals such as automotive AI, healthcare imaging, and the rollout of 5G‑enabled edge devices, which demand specialized, low‑latency chips.

Which growth trends are currently shaping the North America Deep Learning Chip Market?

Current trends feature a migration toward heterogeneous computing architectures that combine GPUs with specialized ASICs for optimal performance‑per‑watt. There is also a noticeable rise in proprietary AI accelerators from cloud providers, as well as increased adoption of FPGA re‑configurability for rapid algorithm iteration. Moreover, the market is witnessing a push toward integrated SoC and SiP solutions that embed AI cores directly into edge devices, shortening time‑to‑market for AI‑enabled products.

How did COVID‑19 impact the North America Deep Learning Chip Market and what is the recovery trajectory?

The pandemic initially disrupted semiconductor fab capacity, causing temporary supply shortages. Simultaneously, accelerated remote work and digital transformation spurred demand for AI‑enhanced collaboration tools and cloud services, offsetting the slowdown. Recovery has been robust, with demand rebounding faster than the broader semiconductor segment, as enterprises continue to scale AI workloads for post‑pandemic growth, reinforcing a strong upward trajectory.

What does the competitive landscape of the North America Deep Learning Chip Market look like?

The market is highly consolidated around a handful of technology leaders—NVIDIA, AMD, Intel, and Google—each leveraging extensive ecosystems and strategic alliances. Recent consolidation activity includes acquisitions of AI‑focused startups and joint ventures aimed at co‑developing next‑generation ASICs. Competitive intensity is driven by rapid product cycles, aggressive pricing, and the pursuit of exclusive partnerships with major cloud and hyperscale customers.

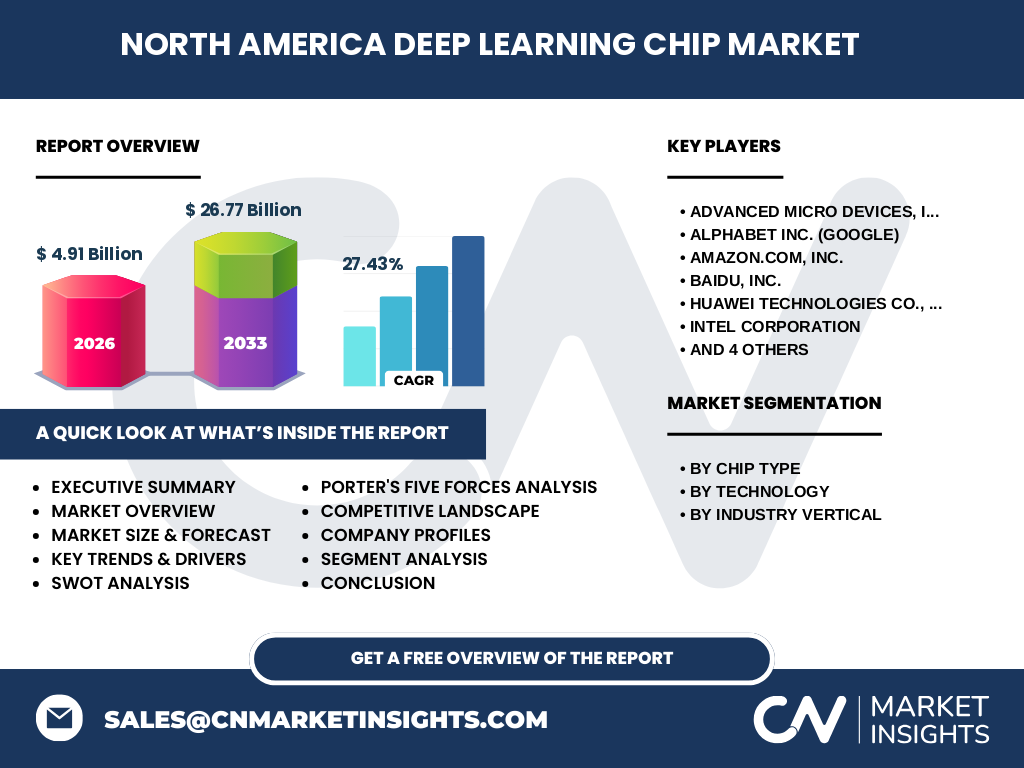

Can you provide an executive summary of the North America Deep Learning Chip Market?

The North America Deep Learning Chip Market is projected to reach USD 4.91 billion in 2026, expanding to USD 26.77 billion by 2033 with a compound annual growth rate of 27.43 %. Growth is propelled by expanding AI applications across multiple verticals, continued investment in custom ASICs, and the emergence of edge‑centric AI chips. While supply‑chain constraints and high R&D costs pose challenges, the market offers substantial upside for innovators and investors targeting high‑performance AI acceleration.

What are the forecast expectations for the North America Deep Learning Chip Market from 2025 to 2032?

Forecasts indicate a sustained acceleration in market size, maintaining the 27.43 % CAGR through 2032. Demand from cloud providers, autonomous systems, and AI‑enabled consumer electronics will drive incremental revenue across all chip categories. The forecast underscores a shift toward energy‑efficient ASIC and SoC offerings, while GPU and FPGA segments will retain relevance for flexible AI workloads and high‑throughput training environments.

How is the North America Deep Learning Chip Market sized and shared by segmentation?

By chip type, the market is divided among GPUs, ASICs, FPGAs, and CPUs, each serving distinct performance and flexibility needs. Technology segmentation includes SoC, SiP, and MCM architectures, reflecting the move toward integration and miniaturization. Industry vertical segmentation covers Media & Advertising, BFSI, IT & Telecom, Retail, Healthcare, and Automotive & Transportation, highlighting the broad applicability of deep‑learning accelerators across the economy.

What is the geographical distribution of the North America Deep Learning Chip Market?

Geographically, the market is concentrated in the United States, which hosts the majority of AI research labs, data‑center operators, and semiconductor foundries. Canada contributes through its strong AI research ecosystem and growing startup scene. The regional split reflects the concentration of major chip designers and cloud service providers, ensuring that North America remains the primary demand engine for deep‑learning chips.

Can you detail the regional analysis of the North America Deep Learning Chip Market?

The United States accounts for the bulk of market revenue, driven by large cloud platforms, autonomous‑vehicle projects, and extensive R&D budgets. Canadian markets show steady growth, particularly in healthcare AI and fintech solutions. Regional trends include increased collaboration between academia and industry, government incentives for AI hardware development, and the expansion of specialized semiconductor fabs that support advanced node manufacturing.

What are the leading company profiles and their strategies in the North America Deep Learning Chip Market?

Key players include NVIDIA (dominant GPU ecosystem and AI software stack), AMD (competitive GPU and CPU offerings), Intel (integration of Xeon CPUs with AI accelerators), Alphabet (Google TPU development), Amazon (custom inferencing chips for AWS), Qualcomm (mobile AI accelerators), Samsung (advanced process technology), Xilinx (reconfigurable FPGA solutions), and emerging entrants focusing on ASIC innovation. Strategies revolve around vertical integration, strategic alliances with cloud providers, and aggressive patent portfolios to lock in ecosystem lock‑in.

How does Porter’s Five Forces analysis apply to the North America Deep Learning Chip Market?

Threat of new entrants is moderate due to high capital requirements, yet start‑ups with niche ASIC designs can penetrate niche segments. Bargaining power of suppliers remains high because advanced lithography equipment is limited to a few vendors. Bargaining power of buyers is strong; cloud providers consolidate purchases, demanding volume discounts and customized features. Threat of substitutes is low, as few alternative technologies match the performance of dedicated AI chips. Industry rivalry is intense, driven by rapid innovation cycles and competition for strategic partnerships.

What are the SWOT findings for the North America Deep Learning Chip Market?

Strengths: Robust AI ecosystem, world‑class semiconductor infrastructure, and high R&D spend. Weaknesses: Dependence on a limited number of fab capacity and high development costs. Opportunities: Expansion into edge computing, vertical‑specific ASICs, and AI‑driven healthcare and automotive applications. Threats: Geopolitical trade tensions affecting supply chains and the rapid pace of technology obsolescence.

How is the value chain structured in the North America Deep Learning Chip Market?

The value chain begins with silicon design (IP cores, architecture definition), proceeds to wafer fabrication (foundry services), followed by assembly, testing, and packaging (including SiP and MCM). Afterwards, chips are integrated into platforms by OEMs and cloud providers, who add software stacks and AI frameworks. Final distribution occurs through direct sales to hyperscalers, system integrators, and enterprise customers, with after‑sales support and firmware updates completing the loop.

What key investment insights can be drawn for stakeholders in the North America Deep Learning Chip Market?

Investors should prioritize companies with diversified product portfolios spanning GPUs, ASICs, and edge‑focused SoCs, as this mitigates reliance on a single segment. Funding R&D pipelines that target energy‑efficient architectures offers long‑term upside. Strategic partnerships with cloud platforms or automotive OEMs can accelerate market adoption. Monitoring supply‑chain resilience, especially fab capacity, is essential for risk management.

What conclusions can be drawn about the North America Deep Learning Chip Market?

The market is on a steep growth trajectory, underpinned by pervasive AI adoption across multiple sectors. While supply constraints and high development expenditures pose challenges, the high CAGR and expanding vertical applications create a compelling landscape for innovators and investors. North America’s strong tech ecosystem and concentration of AI leaders ensure it will remain the premier market for deep‑learning chips through 2033.

What research methodology was employed for this market study?

The study combined primary interviews with industry executives, technology analysts, and key customers, alongside secondary data collection from company filings, market reports, and reputable databases. Trend analysis, CAGR extrapolation, and peer benchmarking were applied to forecast the market to 2033. All figures presented align with the provided base‑year data and projected growth rates.

What is the scope of this research and its limitations?

The research covers the North American region, focusing on chip types (GPU, ASIC, FPGA, CPU), technology formats (SoC, SiP, MCM), and vertical applications listed. It excludes detailed country‑level breakdowns beyond the United States and Canada, and does not quantify market share percentages beyond the aggregate size and forecast values supplied.

Which key companies have made recent developments in the North America Deep Learning Chip Market?

Recent highlights include NVIDIA’s launch of next‑gen Hopper GPUs, AMD’s rollout of AI‑optimized Instinct accelerators, Intel’s integration of Habana AI processors, Alphabet’s expansion of TPU v4 in its data centers, Amazon’s announcement of new Trainium and Inferentia chips for AWS, Qualcomm’s unveiling of Snapdragon AI‑enhanced SoCs, Samsung’s partnership with a leading AI startup for edge AI modules, and Xilinx’s acquisition of a reconfigurable AI IP portfolio. These moves underscore intense innovation and strategic positioning within the market.