What is the Pharmacy Management System Market Overview - Definition, scope, and significance?

The Pharmacy Management System (PMS) market encompasses software and services that enable pharmacies to automate core operations such as prescription processing, inventory control, billing, and regulatory compliance. The scope of the market includes solutions for both small‑ and medium‑sized pharmacies as well as large pharmacy chains, delivered through cloud‑based or on‑premise deployments. Its significance lies in improving patient safety, reducing dispensing errors, enhancing operational efficiency, and supporting reimbursement processes in an increasingly regulated healthcare environment.

What are the Pharmacy Management System Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include the rising demand for digital health solutions, increasing pharmacy automation, and the need for integrated patient data across care settings. Restraints involve high upfront costs for large‑scale implementations and concerns over data security, particularly for on‑premise systems. Challenges stem from fragmented legacy infrastructures and the varying regulatory requirements across regions. Opportunities arise from the expansion of cloud‑based services, the integration of AI for medication adherence monitoring, and the growth of value‑added services such as telepharmacy.

What are the Pharmacy Management System Market Growth Trends?

Current trends feature a shift toward cloud‑native architectures that offer scalability and lower total cost of ownership. Emerging trends include the incorporation of predictive analytics for inventory optimization, mobile‑first interfaces for pharmacists, and interoperability standards that connect PMS with electronic health records (EHR) and health information exchanges. The market is also witnessing a rise in subscription‑based pricing models, enabling smaller pharmacies to adopt advanced functionality without large capital expenditures.

How has COVID‑19 impacted the Pharmacy Management System Market?

The COVID‑19 pandemic accelerated digital adoption as pharmacies sought contact‑less dispensing, remote refill capabilities, and real‑time inventory visibility. Demand surged for cloud‑based solutions that could be quickly provisioned, leading to increased subscription revenues. The recovery trajectory continues to be positive, with pharmacies maintaining higher levels of automation and patients expecting seamless digital experiences established during the pandemic.

What does the Pharmacy Management System Market Competitive Landscape look like?

The competitive landscape is characterized by a mix of established healthcare IT giants and specialized pharmacy solution providers. Major players such as McKesson Corporation, Cerner Corporation, and Epicor Software Corporation dominate the large‑pharmacy segment, while firms like ACG Infotech Ltd. and Talyst LLC focus on niche functionalities and services. Recent market consolidation includes strategic acquisitions aimed at expanding cloud capabilities and integrating advanced analytics.

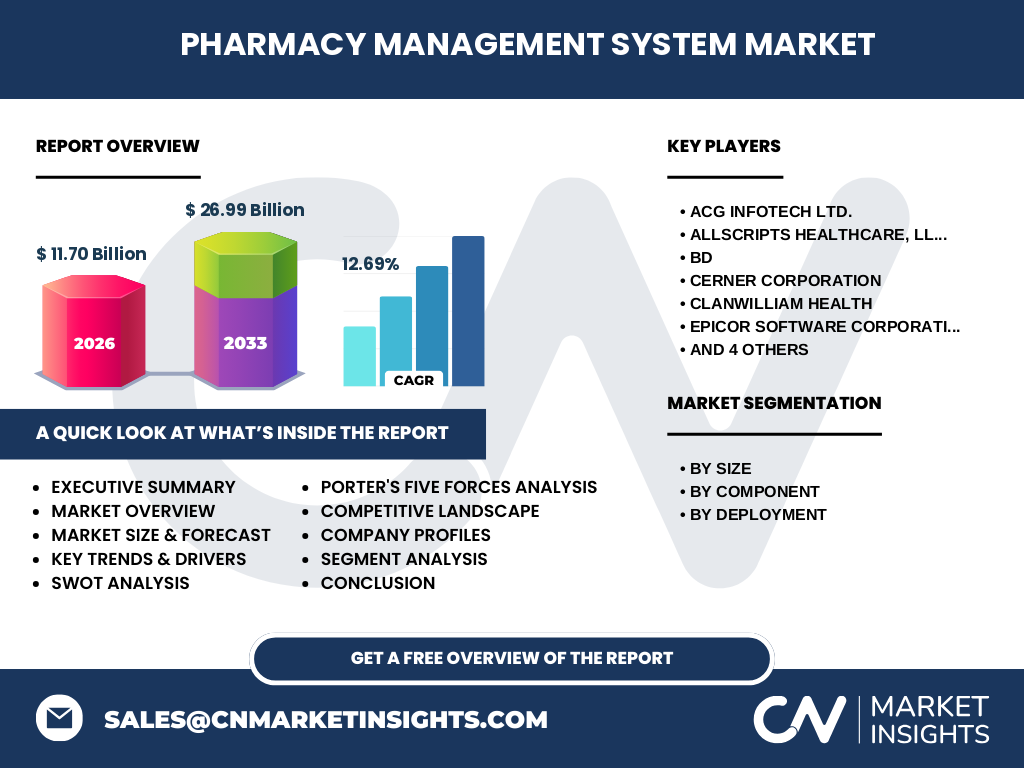

What are the key findings in the Executive Summary of the Pharmacy Management System Market?

The market is valued at $11.70 billion in 2026 and is projected to reach $26.99 billion by 2033, reflecting a robust CAGR of 12.69 %. Growth is driven by digital transformation, regulatory pressure, and the expanding role of pharmacies in chronic disease management. Cloud deployment is outpacing on‑premise solutions, and the services component is gaining traction as providers add value‑added support and maintenance.

What is the Pharmacy Management System Market Forecast for 2025‑2032?

Based on the provided CAGR of 12.69 %, the market is expected to continue its rapid expansion through 2032, maintaining double‑digit growth each year. This trajectory suggests a steady increase in adoption across both small‑ and medium‑sized pharmacies and large pharmacy chains, with a notable shift toward subscription‑based cloud services that drive recurring revenue streams for vendors.

How is the Pharmacy Management System Market Size and Share by Segmentation?

Segmentation by size divides the market into Small‑ and Medium‑sized Pharmacies and Large Pharmacy. By component, the market is split between Solutions and Services, with Solutions representing the core software functionality and Services encompassing implementation, training, and support. Deployment segmentation includes Cloud‑based and On‑premise offerings, where cloud solutions are gaining higher share due to lower entry barriers and faster upgrades.

What is the Global Pharmacy Management System Market Size and Share by Region?

The global market is measured at $11.70 billion in 2026, with a forecasted expansion to $26.99 billion by 2033. While specific regional dollar amounts are not disclosed, the market’s growth is expected to be widespread, reflecting the universal need for pharmacy automation across North America, Europe, Asia‑Pacific, and emerging markets.

What does the Regional Analysis of the Pharmacy Management System Market reveal?

Regional analysis indicates that mature markets such as North America and Europe lead in early adoption of cloud‑based PMS due to advanced healthcare infrastructures and stringent regulatory frameworks. Asia‑Pacific shows high growth potential, driven by expanding retail pharmacy networks and increasing government initiatives for digital health. Emerging economies are beginning to invest in PMS to modernize fragmented pharmacy operations.

Who are the leading companies in the Pharmacy Management System Market and what are their strategies?

Key players include McKesson Corporation, Cerner Corporation, Epicor Software Corporation, ACG Infotech Ltd., and Talyst LLC (Swisslog Healthcare). Strategies focus on expanding cloud portfolios, forming strategic alliances with EHR vendors, and investing in AI‑driven analytics to enhance medication adherence. Companies are also pursuing acquisitions to broaden service offerings and strengthen market presence in both developed and emerging regions.

What does Porter’s Five Forces Analysis reveal about the Pharmacy Management System Market?

• Threat of New Entrants: Moderate, due to high development costs and regulatory compliance requirements. • Bargaining Power of Buyers: Increasing, as pharmacies demand flexible pricing and integration capabilities. • Bargaining Power of Suppliers: Low to moderate; software components are widely available, but specialized talent for AI integration can be scarce. • Threat of Substitutes: Low, because PMS provides unique functionality not easily replicated by generic ERP systems. • Industry Rivalry: High, driven by multiple vendors competing on innovation, service quality, and pricing models.

What are the SWOT strengths, weaknesses, opportunities, and threats for the Pharmacy Management System Market?

Strengths: Established demand, proven impact on safety and efficiency, and strong vendor expertise. Weaknesses: High implementation costs for large enterprises and varying regulatory landscapes. Opportunities: Expansion of cloud services, integration with telehealth, and AI‑driven predictive analytics. Threats: Data security concerns, potential regulatory changes, and competitive pressure from emerging tech startups.

How does the Pharmacy Management System Value Chain operate?

The value chain starts with research and development of core software modules, followed by customization and integration services. Vendors then provide deployment – either cloud or on‑premise – and ongoing support, including training, maintenance, and upgrades. End‑users (pharmacies) generate value through improved workflow efficiency, reduced errors, and enhanced patient engagement, which in turn drives vendor revenue through subscription or service contracts.

What key investment insights can be drawn for the Pharmacy Management System Market?

Investors should prioritize companies with strong cloud portfolios, proven integration capabilities, and a diversified service offering. Look for firms that demonstrate consistent revenue growth, strategic partnerships with EHR providers, and a pipeline of AI‑enhanced features. The sector’s double‑digit CAGR and expanding addressable market across all pharmacy sizes present attractive long‑term upside, especially for firms leading in subscription‑based models.

What are the main conclusions of the Pharmacy Management System Market study?

The market is on a rapid growth path, supported by digital health trends, regulatory pressures, and the increasing role of pharmacies in patient care. Cloud adoption and services revenue are key growth engines, while the competitive environment pushes continuous innovation. Stakeholders can expect sustained demand across all regions, making the sector a compelling focus for strategic investment and partnership development.

Which research methodology was employed for this market study?

The research combines primary interviews with industry executives, technology providers, and pharmacy operators, complemented by secondary data from reputable industry reports, financial statements, and regulatory publications. Market sizing utilizes a top‑down approach anchored on the provided 2026 market value and projected CAGR, while segmentation analysis is based on vendor product catalogs and deployment trends.

What is the scope of this Pharmacy Management System market research?

The scope covers global market size, segmentation by pharmacy size, component, and deployment model, as well as regional distribution, competitive landscape, and forward‑looking forecasts through 2033. It excludes detailed pricing analysis, country‑specific regulatory cost breakdowns, and niche sub‑segments not directly related to the core PMS offerings.

Which key companies and recent developments are shaping the Pharmacy Management System Market?

Prominent companies such as McKesson Corporation, Cerner Corporation, and Epicor Software Corporation have announced cloud expansion initiatives and AI‑driven analytics modules. ACG Infotech Ltd. launched a new mobile‑first solution for rural pharmacies, while Talyst LLC (Swisslog Healthcare) secured a partnership with a major European pharmacy chain to deploy automated dispensing units integrated with their PMS. These developments highlight ongoing innovation and collaborative growth strategies across the market.