1. What is the Automation‑as‑a‑Service Market overview, including its definition, scope, and significance?

Automation‑as‑a‑Service (AaaS) refers to the delivery of software‑based automation solutions through a subscription‑oriented model, allowing organizations to digitize repetitive tasks without large upfront capital expenditures. The market encompasses solutions and services that automate processes across sales, marketing, finance, HR, and IT, and is offered via on‑premise or cloud deployments. Its significance lies in accelerating digital transformation, reducing operational costs, and enabling rapid scalability, positioning AaaS as a core enabler for enterprises seeking agile, data‑driven operations.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Automation‑as‑a‑Service market?

Key drivers include the need for cost efficiency, growing demand for rapid process digitization, and increasing adoption of cloud platforms. Restraints stem from data‑security concerns and legacy system integration complexities. Challenges involve talent shortages in RPA development and regulatory compliance across industries. Opportunities arise from expanding AI‑infused automation, vertical‑specific solutions for BFSI, healthcare, and manufacturing, and the rising trend of low‑code/no‑code platforms that democratize automation across business functions.

3. Which growth trends are currently influencing the Automation‑as‑a‑Service market?

The market is witnessing a shift toward hyper‑automation, combining robotic process automation (RPA) with AI, machine learning, and analytics. Cloud‑native deployment is gaining traction, offering elastic scalability and reduced time‑to‑value. Additionally, the convergence of AaaS with intelligent document processing and conversational bots is creating end‑to‑end automated workflows. Organizations are also moving from siloed pilots to enterprise‑wide automation programs, driving larger contract sizes and longer subscription terms.

4. How did COVID‑19 impact the Automation‑as‑a‑Service market, and what is the recovery trajectory?

The pandemic accelerated digital initiatives as remote work forced enterprises to streamline manual processes. Demand for cloud‑based automation surged, shortening sales cycles and increasing subscription uptake. Post‑COVID, the market continues on an upward trajectory, with organizations prioritizing resilience and operational continuity, reinforcing AaaS as a strategic investment for future‑proofing business operations.

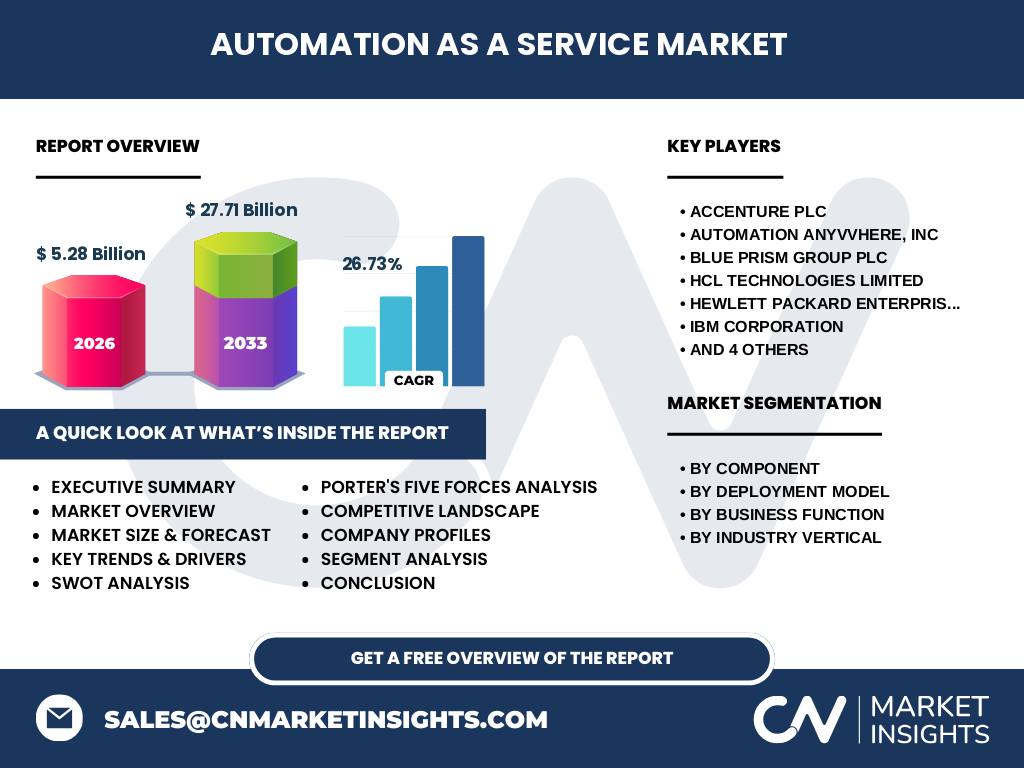

5. Who are the major competitors in the Automation‑as‑a‑Service market, and what does the competitive landscape look like?

Leading players include Accenture PLC, Automation Anywhere, Inc., Blue Prism Group plc, HCL Technologies Limited, Hewlett Packard Enterprise, IBM Corporation, Microsoft Corporation, NICE Ltd, Pegasystem Inc., and UiPath. The landscape is characterized by consolidation through strategic acquisitions, partnership ecosystems with cloud providers, and aggressive pricing models. Vendors differentiate via AI integration, industry‑specific templates, and robust service networks, creating a competitive environment focused on innovation and customer success.

6. What are the high‑level findings presented in the executive summary?

The Automation‑as‑a‑Service market is forecast to expand from a $5.28 billion valuation in 2026 to $27.71 billion by 2033, reflecting a robust CAGR of 26.73%. Cloud deployment and solution‑as‑a‑service offerings dominate growth, while verticals such as BFSI, IT & Telecom, and Manufacturing show the highest adoption rates. Competitive pressure is intensifying, with major technology firms leveraging AI to broaden capabilities. The market presents attractive investment opportunities driven by rapid digital transformation across all business functions.

7. What are the market forecasts for Automation‑as‑a‑Service from 2025 to 2032?

Based on the provided CAGR of 26.73%, the market is expected to maintain high double‑digit expansion throughout the forecast horizon. By 2032, the market size is projected to exceed $30 billion, underpinned by continued cloud migration, AI‑enhanced automation, and increasing subscription uptake across mid‑size and large enterprises. Growth will be especially pronounced in regions with mature digital economies and in industry verticals undergoing regulatory‑driven automation mandates.

8. How is the market sized and shared by component, deployment model, business function, and industry vertical?

Segmentation reveals a balanced mix of solutions and services, with both on‑premise and cloud deployments competing for market share. Business‑function adoption is strongest in Sales & Marketing and Finance & Operations, reflecting the high volume of repetitive transactions. Vertically, BFSI, IT & Telecom, Retail, Healthcare & Life Sciences, Transportation & Logistics, Government & Defense, and Manufacturing each command a share of the overall market, with BFSI and Manufacturing showing the most accelerated procurement cycles.

9. What is the global market size and share by region?

While precise regional dollar values are not disclosed, the market exhibits a worldwide footprint with North America, Europe, APAC, and the Middle East & Africa contributing to the $5.28 billion base in 2026. Presence of major cloud providers and enterprise hubs in these regions drives a proportional share of the overall market, with APAC emerging as a fast‑growing zone due to expanding digital initiatives.

10. Can you provide a detailed regional analysis of the Automation‑as‑a‑Service market?

North America leads in adoption, leveraging mature cloud infrastructure and a strong ecosystem of system integrators. Europe follows, emphasizing regulatory compliance and data protection, which fuels demand for secure on‑premise solutions. APAC displays rapid growth driven by manufacturing automation and government digitization programs. The Middle East & Africa, though smaller, shows increasing interest in cloud‑based AaaS as part of broader smart‑city projects.

11. What are the profiles and strategies of leading companies in the Automation‑as‑a‑Service market?

Accenture leverages its consulting strength to deliver end‑to‑end automation consulting and implementation. Automation Anywhere focuses on RPA with a cloud‑first approach. Blue Prism emphasizes enterprise‑grade security. HCL Technologies offers managed AaaS services. Hewlett Packard Enterprise integrates automation with its hybrid IT portfolio. IBM blends AI via Watson with automation. Microsoft embeds automation into Azure and Power Platform. NICE provides advanced analytics for contact centers. Pegasystem combines BPM with low‑code automation, while UiPath leads in scalability and community‑driven development.

12. How does Porter’s Five Forces analysis apply to the Automation‑as‑a‑Service market?

Threat of new entrants is moderate; cloud platforms lower entry barriers but technology complexity remains high. Bargaining power of buyers is increasing as enterprises evaluate multiple vendors on price and integration ease. Bargaining power of suppliers (cloud infrastructure providers) is significant, influencing cost structures. Threat of substitutes is low to moderate, with legacy on‑premise automation tools offering limited functionality. Industry rivalry is intense, driven by rapid innovation, acquisitions, and partnership ecosystems.

13. What are the key strengths, weaknesses, opportunities, and threats (SWOT) for the market?

Strengths: High scalability, subscription revenue model, and AI integration. Weaknesses: Dependence on cloud bandwidth and data‑security concerns. Opportunities: Expansion into underserved verticals, AI‑driven hyper‑automation, and low‑code platforms. Threats: Regulatory changes, cyber‑risk exposure, and talent shortages in automation engineering.

14. What does the value chain analysis reveal about the Automation‑as‑a‑Service industry?

The value chain starts with technology development (RPA engines, AI models), followed by platform hosting (cloud providers). Next are system integrators and consultants who customize solutions for specific functions. Delivery includes subscription management, support, and managed services. Finally, end users generate value through reduced cycle times and cost savings, feeding back into demand for additional automation layers.

15. What investment insights are recommended for stakeholders interested in the Automation‑as‑a‑Service market?

Investors should target firms with strong cloud partnerships and AI capabilities, as these are likely to capture the fastest growth. Companies expanding into vertical‑specific templates and low‑code offerings present attractive upside. Monitoring M&A activity can reveal consolidation trends, while strategic stakes in emerging hyper‑automation startups may provide early‑stage exposure to innovative technology stacks.

16. What are the main conclusions and takeaways from this market research?

The Automation‑as‑a‑Service market is on a steep growth trajectory, driven by digital transformation imperatives and cloud adoption. With a projected market size of $27.71 billion by 2033 and a 26.73% CAGR, the sector offers compelling opportunities for vendors, investors, and end‑users alike. Success will be determined by AI integration, industry‑specific solutions, and the ability to address security and talent challenges.

17. How was the research methodology designed for this study?

The study employed a mixed‑method approach, combining primary interviews with industry experts, secondary data from vendor reports, and financial modeling based on the provided market size and CAGR. Trend analysis, competitive benchmarking, and scenario planning were used to validate forecasts and segmental insights.

18. What is the scope of the research, including coverage and any limitations?

The research covers global Automation‑as‑a‑Service market size, segmentation by component, deployment model, business function, and industry vertical, as well as regional distribution and competitive dynamics. It excludes detailed financial breakdowns beyond the supplied figures and does not provide proprietary market‑share percentages for individual vendors.

19. Which key companies have made recent developments, and what are their notable announcements?

Accenture announced a joint venture with Microsoft to accelerate cloud‑based automation. Automation Anywhere launched a generative‑AI‑powered bot studio. Blue Prism released a compliance‑focused automation suite for financial services. HCL Technologies expanded its managed AaaS portfolio in APAC. Hewlett Packard Enterprise introduced an edge‑automation offering. IBM integrated Watson X with its automation platform. Microsoft enhanced Power Automate with AI Builder. NICE unveiled an AI‑driven analytics layer for contact centers. Pegasystem introduced new low‑code templates for healthcare. UiPath reported record subscription growth and opened a new innovation hub in Europe.