1. What is the Precooked Corn Flour Market Overview – definition, scope, and significance?

Precooked corn flour is a heat‑treated, milled product derived from yellow or white corn kernels that is ready for immediate use in food manufacturing. Its scope covers a broad range of applications such as bakery items, soups, sauces, ready‑to‑eat (RTE) meals, extruded snacks, and confectionery. The market is significant because it offers manufacturers reduced processing time, consistent quality, and enhanced shelf stability, meeting growing consumer demand for convenient and clean‑label products.

2. What are the main drivers, restraints, challenges, and opportunities in the Precooked Corn Flour Market?

Key drivers include rising demand for gluten‑free and non‑wheat alternatives, expanding snack‑food consumption, and increasing industrialisation of food processing in emerging economies. Restraints stem from price volatility of raw corn and competition from other pre‑cooked starches such as rice and tapioca. Challenges involve meeting stringent food‑safety regulations and supply‑chain disruptions. Opportunities arise from product innovation (flavored or fortified flours), clean‑label trends, and the growth of plant‑based protein blends that incorporate precooked corn flour.

3. Which growth trends are currently shaping the Precooked Corn Flour Market?

The market is witnessing a shift toward value‑added blends that combine precooked corn flour with pulses or fibers to boost nutritional profiles. There is also a trend of adopting “clean‑label” branding, where manufacturers highlight the absence of additives. Moreover, the surge in automated, high‑speed extrusion technology is expanding the use of precooked corn flour in extruded snacks, while bakery innovators are experimenting with hybrid dough systems that reduce wheat flour ratios.

4. How did COVID‑19 impact the Precooked Corn Flour Market and what is the recovery trajectory?

The pandemic initially disrupted corn supply chains and caused temporary plant shutdowns, leading to short‑term inventory shortages. However, the surge in home cooking, demand for shelf‑stable RTE meals, and accelerated adoption of online grocery channels boosted sales of precooked corn flour. Recovery has been steady, with demand rebounding to pre‑pandemic levels by late 2022 and continuing to grow as consumer habits favor convenient, ready‑to‑use ingredients.

5. Who are the major competitors and what is the level of consolidation in the Precooked Corn Flour Market?

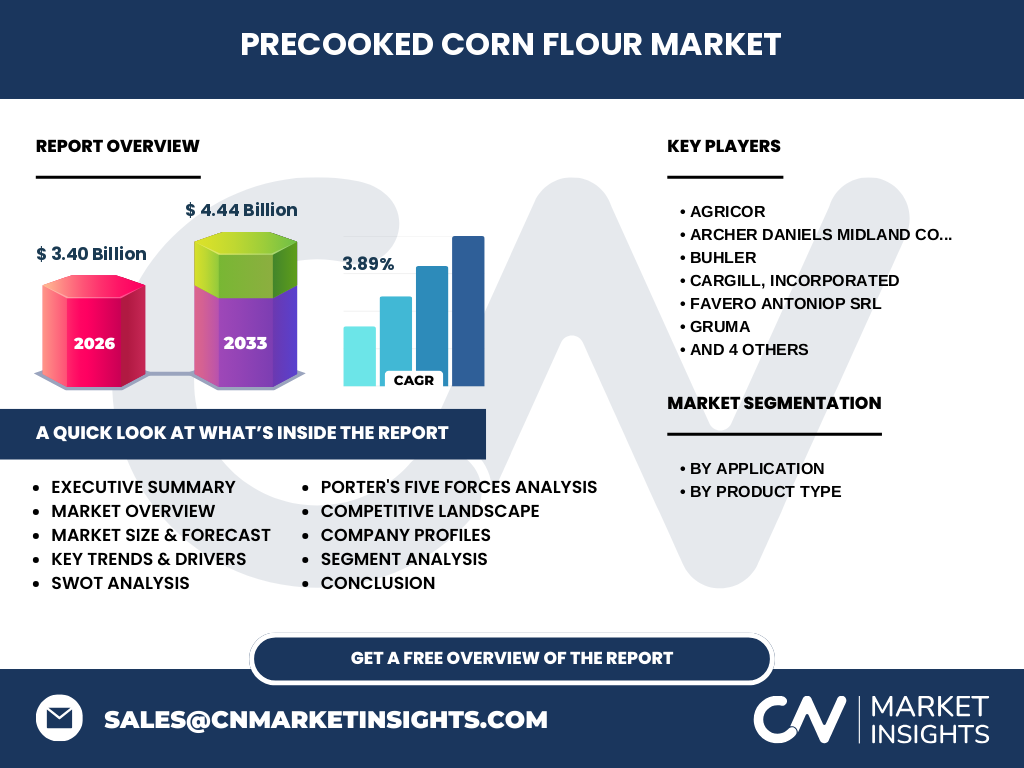

The competitive landscape is dominated by multinational grain processors and specialty ingredient firms. Leading players include Agricor, Archer Daniels Midland Company, Buhler, Cargill, Incorporated, Favero Antoniop SRL, Gruma, Limagrain (Limagrain Ingredients), Molion Peila SpA, S.A.B. de C.V., and SEMO Milling LLC. Consolidation is moderate, with strategic acquisitions and joint ventures aimed at expanding geographic reach and product portfolios, but a sizeable number of regional specialists maintain a fragmented competitive environment.

6. What are the key findings in the Executive Summary of the Precooked Corn Flour Market?

The market is valued at $3.40 billion in 2026 and is projected to reach $4.44 billion by 2033, reflecting a CAGR of 3.89 %. Growth is driven by clean‑label demand, gluten‑free trends, and expanding snack and RTE segments. Yellow corn flour holds a larger share due to its familiar taste profile, while white corn flour appeals to niche health‑conscious segments. The outlook remains positive, with ample room for product innovation and geographic expansion.

7. What are the forecast expectations for the Precooked Corn Flour Market from 2025 to 2032?

Based on the provided CAGR of 3.89 %, the market is expected to maintain steady growth through 2032. By 2032, the market size is projected to surpass $4.4 billion, driven by continued adoption in bakery, soup, sauce, RTE, and snack applications. The forecast underscores robust demand in Asia‑Pacific and Latin America, where expanding middle‑class populations are increasing consumption of convenient food products.

8. How is the Precooked Corn Flour Market sized and shared by application and product type?

Application‑wise, the market is divided among bakery and confectionery, soup, sauces and dressings, RTE meals and foods, and extruded snacks. Each segment benefits from the ready‑to‑use nature of the flour, with bakery and confectionery historically representing the largest share due to extensive use in pastries and cakes. By product type, the market splits into yellow corn flour and white corn flour. Yellow corn flour dominates the overall share, while white corn flour captures niche segments seeking a lighter colour and milder flavour.

9. What is the global Precooked Corn Flour Market size and share by region?

Globally, the market reached $3.40 billion in 2026. Though exact regional breakdowns are not disclosed, the market’s growth is supported by strong demand in North America, Europe, Asia‑Pacific, and Latin America. The increasing industrialisation of food processing in Asia‑Pacific and rising snack consumption in Latin America are key contributors to the overall market size.

10. What are the detailed regional performance insights for the Precooked Corn Flour Market?

In North America, mature food‑manufacturing sectors drive steady consumption of precooked corn flour for bakery and snack production. Europe shows growing interest in gluten‑free alternatives, boosting demand for both yellow and white variants. Asia‑Pacific experiences the fastest expansion, propelled by rapid urbanisation, increasing disposable incomes, and a shift toward convenience foods. Latin America benefits from abundant corn cultivation, reducing raw‑material costs and encouraging local production.

11. Which companies lead the Precooked Corn Flour Market and what are their strategic approaches?

Key leaders such as Archer Daniels Midland Company and Cargill leverage extensive grain sourcing networks to ensure supply stability and competitive pricing. Agricor focuses on high‑purity, specialty grades for premium bakery customers. Gruma emphasizes vertical integration from corn farming to finished flour, enhancing control over quality. Limagrain Ingredients invests in R&D to develop fortified and functional corn flour blends, while Buhler provides advanced processing equipment that supports high‑volume precooking operations.

12. How does Porter’s Five Forces assess the Precooked Corn Flour Market?

Threat of new entrants is moderate due to high capital requirements for pre‑cooking facilities. Bargaining power of suppliers is moderate; while corn is abundant, price volatility can affect margins. Bargaining power of buyers is high, as large food manufacturers can negotiate volume discounts. Threat of substitutes is moderate, with alternatives like rice or tapioca flour offering competition. Industry rivalry is intense, driven by product differentiation, price competition, and strategic partnerships.

13. What are the SWOT highlights for the Precooked Corn Flour Market?

Strengths: ready‑to‑use format, gluten‑free credentials, and versatile applications. Weaknesses: dependence on corn price fluctuations and limited differentiation between yellow and white variants. Opportunities: development of fortified, flavored, or protein‑enriched blends and expansion into emerging markets. Threats: competition from alternative starches and tightening food‑safety regulations that may increase compliance costs.

14. What does the value chain of the Precooked Corn Flour Market look like?

The value chain starts with corn farming and procurement, followed by cleaning, degermination, and milling. The next stage is the pre‑cooking process, which involves hydrothermal treatment to gelatinize starches. After drying and milling into fine flour, the product is packaged and distributed to food manufacturers. Ancillary services such as quality testing, logistics, and technical support complete the chain, with major players participating across multiple stages to enhance control and margins.

15. What investment insights are critical for stakeholders in the Precooked Corn Flour Market?

Investors should focus on companies with integrated supply chains that mitigate raw‑material price risk. Target firms that are expanding product portfolios toward functional blends and those investing in automation to lower production costs. Geographic diversification, especially into fast‑growing Asia‑Pacific and Latin America, offers higher upside. Strategic partnerships with bakery and snack manufacturers can secure long‑term off‑take agreements, enhancing revenue stability.

16. What are the concluding takeaways from the Precooked Corn Flour Market analysis?

The market is on a clear growth trajectory, underpinned by clean‑label and gluten‑free trends. Yellow corn flour leads the product landscape, while white corn flour serves niche health markets. Regional expansion, especially in Asia‑Pacific, will drive the bulk of future sales. Competitive dynamics favor firms that can secure supply, innovate functional blends, and leverage automation to maintain cost efficiency.

17. How was the research for this Precooked Corn Flour Market report conducted?

The study combined primary interviews with industry experts, secondary analysis of company reports, trade publications, and government statistics. Market sizing used the provided 2026 valuation of $3.40 billion and applied the stated CAGR of 3.89 % to project forward. Segmentation by application and product type was derived from supplier portfolios and consumer usage patterns.

18. What is the scope of this research and its coverage limitations?

The research covers global market size, segmentation by application and product type, regional performance, competitive landscape, and forward forecasts up to 2033. It focuses on the precooked corn flour segment within the broader starch and flour industry. While the analysis provides comprehensive qualitative insights, it refrains from presenting undisclosed quantitative data such as exact regional market shares or company‑level revenue figures beyond those supplied.

19. Which key companies have recent developments, product launches, or partnerships in the Precooked Corn Flour Market?

Archer Daniels Midland Company announced a new high‑purity yellow corn flour line tailored for gluten‑free bakery applications. Cargill launched a fortified white corn flour enriched with vitamin B6 for RTE meals. Gruma entered a joint venture with a Southeast Asian snack producer to supply locally sourced precooked corn flour, reducing import reliance. Limagrain Ingredients introduced a protein‑enhanced blend targeting the plant‑based market, while Buhler unveiled upgraded pre‑cooking equipment that improves energy efficiency for large‑scale manufacturers.