1. What is the Custom Procedure Kits Market and why is it significant?

The Custom Procedure Kits (CPKs) market comprises specially assembled sets of medical devices, consumables, and accessories that are tailored to individual surgical or interventional procedures. These kits may be sterile or non‑sterile, disposable or reusable, and are configured for specific specialties such as bariatric, orthopedic, cardiac, and ophthalmology surgeries. By bundling all required items into a single, ready‑to‑use package, CPKs streamline operating‑room workflow, reduce instrument handling errors, and improve patient safety. Their significance lies in enabling hospitals and clinics to lower procedural time, minimize inventory complexity, and achieve cost efficiencies—factors that are increasingly critical in value‑based care environments.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Custom Procedure Kits market?

Drivers include rising surgical volumes worldwide, a shift toward minimally invasive techniques, and growing demand for standardized, cost‑effective operating‑room solutions. Health systems are also seeking to reduce postoperative complications, which fuels adoption of pre‑validated kit configurations. Restraints involve high upfront customization costs for manufacturers and the need for rigorous regulatory compliance across multiple jurisdictions. Challenges stem from integrating CPKs into existing supply‑chain logistics and convincing surgeons to transition from traditional instrument sets. Nonetheless, significant opportunities exist in expanding kit offerings for emerging procedure categories, leveraging digital technologies for kit design, and forming strategic partnerships with hospitals to develop procedure‑specific kits.

3. Which current and emerging trends are influencing growth in the Custom Procedure Kits market?

Key trends include the rise of data‑driven kit optimization, where analytics identify the most frequently used items and eliminate redundancies. Another trend is the incorporation of smart packaging—RFID tags and barcoding—to enhance traceability and inventory management. Manufacturers are increasingly offering kits that combine disposable and reusable components, balancing sustainability with clinical performance. Finally, the emergence of robotic‑assisted surgeries is prompting the development of specialized kits that integrate with robotic platforms, creating a new growth niche.

4. How has COVID‑19 impacted the Custom Procedure Kits market and what is the recovery trajectory?

The pandemic caused an initial slowdown as elective surgeries were postponed, leading to a temporary dip in CPK demand. However, the crisis also highlighted the value of pre‑assembled, sterile kits that reduce set‑up time and limit staff exposure. Post‑2020, hospitals accelerated adoption of CPKs to streamline workflow and support the rapid restart of surgical services. Recovery has been robust, with demand rebounding faster than pre‑pandemic levels, driven by pent‑up surgical volume and heightened focus on infection control.

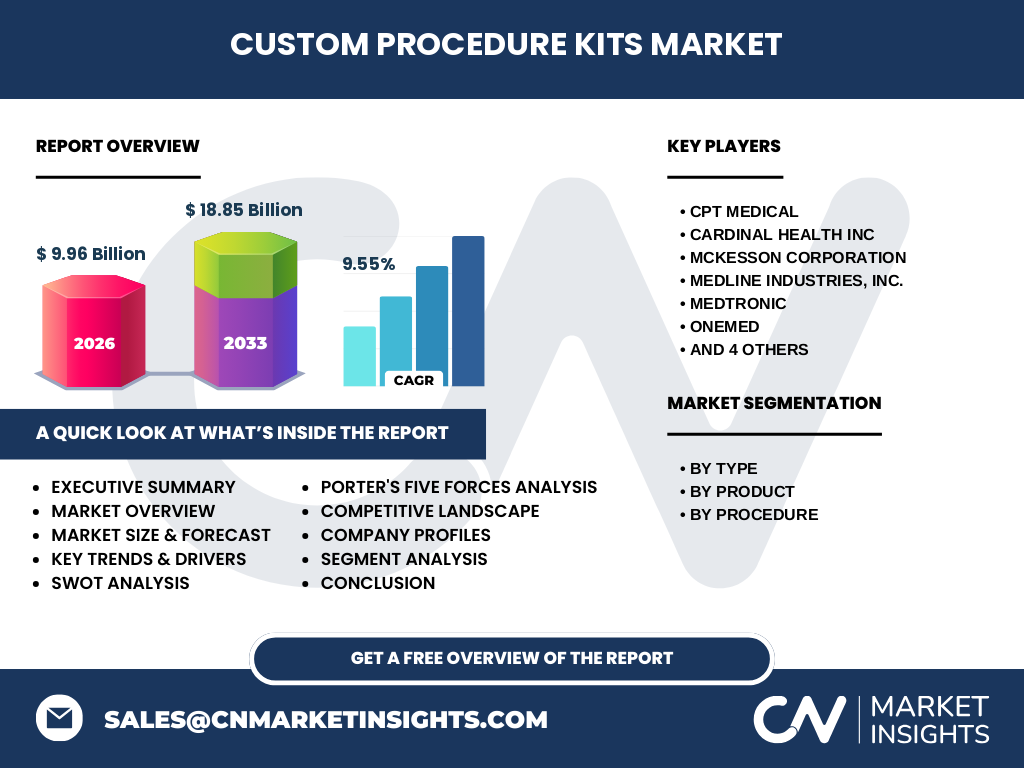

5. Who are the major competitors and what is the level of consolidation in the Custom Procedure Kits market?

The market features a mix of large medical‑device distributors and specialty manufacturers. Prominent players include CPT Medical, Cardinal Health Inc., McKESSON CORPORATION, Medline Industries, Inc., Medtronic, OneMed, Owens & Minor Inc., Smiths Medical, Teleflex Incorporated, and Terumo Cardiovascular Systems Corporation. Over the past three years, there has been moderate consolidation as larger distributors acquire niche kit designers to broaden product portfolios and achieve economies of scale. Competitive dynamics are shaped by innovation in kit content, pricing flexibility, and the ability to provide end‑to‑end logistics services.

6. What are the high‑level findings of the Custom Procedure Kits market?

The market is valued at $9.96 billion in 2026 and is projected to reach $18.85 billion by 2033, reflecting a robust CAGR of 9.55 %. Growth is driven by increasing surgical case loads, a push for efficiency, and the adoption of technology‑enabled kits. Sterile kits dominate the type segment, while disposable kits lead the product segment due to convenience and infection‑control considerations. Procedure‑specific kits—particularly in orthopedic, cardiac, and spine surgery—show the strongest demand. The market remains fragmented but is trending toward consolidation as major distributors expand their custom‑kit capabilities.

7. What is the forecast for the Custom Procedure Kits market from 2025 to 2032?

Based on the provided CAGR of 9.55 %, the market is expected to continue expanding at a double‑digit pace through 2032. By 2032, the market size is anticipated to be well above the 2033 projection of $18.85 billion, indicating sustained momentum. Growth will be supported by ongoing investments in surgical technology, increasing adoption of bundled payment models that reward efficiency, and the rollout of new procedure‑specific kits across emerging economies.

8. How is the Custom Procedure Kits market sized and shared by segment?

Segmentation is structured across three dimensions. By type, kits are classified as Sterile and Non‑Sterile, with sterile kits accounting for the larger share due to regulatory and infection‑control imperatives. By product, the market splits into Disposable and Reusable kits; disposable kits currently lead because of their ease of use and reduced reprocessing costs. By procedure, the market covers Bariatric, Colorectal, Thoracic, Orthopedic, Ophthalmology, Spine Surgery, and Cardiac Surgery. Orthopedic, Cardiac, and Spine Surgery kits represent the highest demand, reflecting the volume of procedures and the complexity of instrument sets required.

9. What is the geographic distribution of the Global Custom Procedure Kits market?

The market exhibits a worldwide footprint, with North America leading due to advanced healthcare infrastructure and early adoption of bundled surgical solutions. Europe follows, driven by strong regulatory standards and a focus on operating‑room efficiency. The Asia‑Pacific region shows the fastest growth rate, propelled by expanding hospital networks and rising surgical volumes in China, India, and Japan. Latin America and the Middle East & Africa present emerging opportunities as they upgrade surgical capabilities.

10. What are the detailed regional performances in the Custom Procedure Kits market?

In North America, high per‑procedure spending and extensive adoption of value‑based care models sustain strong demand for both sterile and disposable kits. Europe benefits from harmonized EU medical‑device regulations, facilitating cross‑border kit distribution. Asia‑Pacific leverages cost‑conscious purchasing while investing in modern OR suites, creating a fertile environment for both reusable and disposable kit offerings. Latin America is gradually moving from fragmented, physician‑ordered supplies toward standardized kits, while Middle East & Africa are seeing increased government‑driven hospital modernization projects that incorporate CPK solutions.

11. Which companies lead the Custom Procedure Kits market and what are their key strategies?

Leading firms such as CPT Medical, Cardinal Health, Medtronic, and Teleflex focus on expanding their custom‑kit portfolios through strategic acquisitions and partnerships with surgical societies. Medline Industries and Owens & Minor leverage extensive distribution networks to offer turnkey kit services, including sterilization and inventory management. Terumo emphasizes integration of its cardiovascular devices into cardiac‑surgery kits, while Smiths Medical targets infection‑control by promoting single‑use disposable kits. Innovation, end‑to‑end logistics, and collaborative product development are common strategic themes.

12. How do Porter’s Five Forces shape the Custom Procedure Kits market?

Threat of new entrants is moderate; high regulatory barriers and the need for sophisticated supply‑chain capabilities deter casual entrants. Bargaining power of buyers is strong, as large hospital systems can negotiate pricing and demand customization. Supplier power is moderate; manufacturers rely on a limited pool of high‑quality component suppliers, but competition among them keeps prices in check. Threat of substitutes is low because alternative solutions—such as ad‑hoc instrument sets—lack the efficiency gains of pre‑assembled kits. Competitive rivalry is intense, driven by product differentiation, pricing strategies, and value‑added services such as inventory analytics.

13. What are the SWOT elements for the Custom Procedure Kits market?

Strengths: Proven cost and time efficiencies, strong demand from value‑based care models, and growing acceptance across specialties. Weaknesses: High customization costs and dependence on regulatory approvals. Opportunities: Expansion into emerging markets, integration with digital OR platforms, and development of eco‑friendly reusable kits. Threats: Potential price pressure from large healthcare purchasers and rapid regulatory changes that could increase compliance costs.

14. How does the value chain of the Custom Procedure Kits market operate?

The value chain begins with clinical insight and kit design, where surgeons and manufacturers define procedure‑specific requirements. Next, component sourcing involves procurement of sterile devices, consumables, and reusable instruments from specialized suppliers. The assembly and sterilization stage creates the final kit, followed by quality assurance to meet regulatory standards. Distribution leverages both vendor‑managed inventory and hospital‑direct supply chains, and post‑sale services such as re‑sterilization, kit tracking, and data analytics complete the loop, providing feedback for continuous improvement.

15. What investment insights are recommended for stakeholders in the Custom Procedure Kits market?

Investors should prioritize companies with strong digital capabilities, as data‑driven kit optimization is a growing differentiator. Firms that demonstrate global distribution reach and regulatory expertise are positioned to capture emerging‑market demand. Partnerships with hospital networks for bundled purchasing agreements can lock in long‑term revenue streams. Finally, capital allocation toward sustainable reusable kits may yield both cost savings for customers and a competitive edge in environmentally conscious markets.

16. What are the key takeaways from the Custom Procedure Kits market analysis?

The market is on a clear growth trajectory, nearly doubling from $9.96 billion in 2026 to $18.85 billion by 2033, driven by efficiency demands, procedural volume growth, and technology integration. Sterile, disposable kits dominate, especially in high‑complexity surgeries such as orthopedic and cardiac procedures. Regional dynamics show mature adoption in North America and Europe, with rapid expansion in Asia‑Pacific. Competitive pressure is high, encouraging innovation in kit design, smart packaging, and service models. Stakeholders who combine regulatory agility with digital analytics are best positioned to capitalize on the market’s momentum.

17. How was the research for this report conducted?

The study employed a mixed‑method approach, combining primary interviews with key opinion leaders, hospital procurement heads, and senior executives from leading CPK manufacturers. Secondary data were gathered from industry databases, regulatory filings, and reputable market‑analysis publications. Quantitative forecasts were derived using compound‑annual‑growth calculations anchored to the provided baseline (2026) and projected (2033) values, while qualitative insights were triangulated across multiple sources to ensure robustness.

18. What is the scope of this research and its limitations?

The scope covers global market size, segmentation by type, product, and procedure, as well as regional performance, competitive landscape, and future outlook up to 2033. The analysis focuses on the specified companies and procedure categories. Limitations include the reliance on publicly available financial figures and the exclusion of proprietary data that may exist within individual corporations. Forecast accuracy is contingent upon the continuation of current economic and healthcare trends.

19. Which key companies have recent developments in the Custom Procedure Kits market?

Recent highlights include CPT Medical’s launch of a digital‑tracking platform for orthopedic kits, Cardinal Health’s acquisition of a niche reusable‑kit manufacturer to broaden its sustainability portfolio, and Medtronic’s collaboration with leading cardiac centers to develop procedure‑specific cardiac surgery kits integrated with its device ecosystem. Teleflex announced a partnership with a major hospital network to pilot RFID‑enabled disposable kits for spine surgery, while Terumo introduced a new line of cardiac procedure kits featuring its latest valve technologies. These initiatives underscore the market’s emphasis on innovation, digital integration, and strategic alliances.