What is the Big Data as a Service (BDaaS) Market Overview - Definition, scope, and significance?

Big Data as a Service (BDaaS) refers to cloud‑based platforms that deliver end‑to‑end big‑data capabilities—including ingestion, storage, processing, analytics, and visualization—through subscription models. The scope covers solutions and services across public and private clouds, targeting enterprises of all sizes and multiple industries such as BFSI, IT & Telecom, Healthcare, Manufacturing, and Media & Entertainment. Its significance lies in enabling organizations to unlock actionable insights without the heavy upfront investment in infrastructure, thereby accelerating digital transformation and competitive advantage.

What are the Big Data as a Service (BDaaS) Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include exponential data growth, the need for real‑time analytics, and rapid cloud adoption that lower barriers to entry. Restraints involve data‑privacy regulations and concerns over latency in multi‑tenant environments. Challenges stem from integration complexity with legacy systems and talent shortages in data science. Opportunities arise from emerging use cases such as AI‑driven predictive maintenance, personalized customer experiences, and expansion into underserved mid‑market segments.

What are the Big Data as a Service (BDaaS) Market Growth Trends?

Current trends show a shift toward hybrid deployment models that combine public and private clouds for flexibility and compliance. Edge‑enabled BDaaS is gaining traction as IoT devices generate massive streams of data. Additionally, the integration of machine‑learning frameworks within BDaaS platforms is becoming a standard offering, enabling self‑service analytics and automated insight generation.

How has COVID‑19 impacted the Big Data as a Service (BDaaS) Market?

The pandemic accelerated cloud migration as organizations sought resilient, remote‑ready data infrastructures. Demand for real‑time analytics surged to support supply‑chain visibility and pandemic‑related forecasting. While initial disruptions slowed some projects, the overall trajectory remained upward, positioning BDaaS as a critical enabler of post‑COVID recovery and resilience planning.

What does the Big Data as a Service (BDaaS) Market Competitive Landscape look like?

The market is dominated by major cloud and enterprise software players, including Amazon Web Services, Microsoft, Google, IBM, Oracle, SAP, Dell Technologies, Hewlett Packard Enterprise, SAS, and Teradata. Consolidation is evident through strategic acquisitions and partnerships that expand service portfolios and geographic reach. Competitive differentiation focuses on platform scalability, integrated AI capabilities, and industry‑specific solution templates.

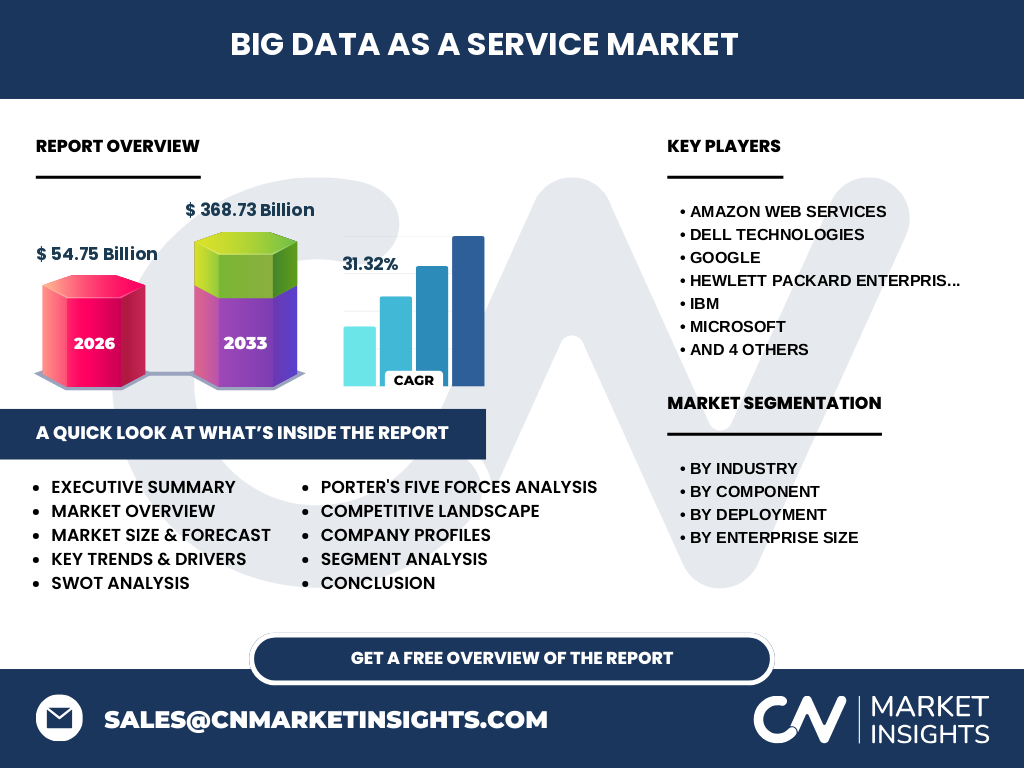

What are the key findings in the Executive Summary of the Big Data as a Service (BDaaS) Market?

The BDaaS market is valued at $54.75 billion in 2026 and is projected to reach $368.73 billion by 2033, reflecting a robust CAGR of 31.32 %. Growth is driven by cross‑industry data explosion, cloud‑first strategies, and the need for agile analytics. Leading vendors are expanding AI‑enabled services, while regional adoption varies with North America and APAC leading deployment.

What are the Big Data as a Service (BDaaS) Market Forecasts for 2025‑2032?

Based on the provided CAGR of 31.32 %, the market is expected to continue its rapid expansion through 2032, maintaining strong momentum as enterprises scale analytics workloads. The forecast underscores sustained investment in both solution and services components, with increasing demand from large enterprises and a growing foothold among SMEs seeking cost‑effective analytics platforms.

How is the Big Data as a Service (BDaaS) Market Size and Share distributed by segmentation?

Segmentation by industry shows balanced interest across BFSI, IT & Telecom, Healthcare, Manufacturing, and Media & Entertainment, each leveraging BDaaS for domain‑specific analytics. By component, solutions (platforms, tools, and analytics engines) account for a substantial share, while services (implementation, migration, and managed support) complement adoption. Deployment splits between public cloud (favored for scalability) and private cloud (preferred for compliance). Enterprise size segmentation highlights growing uptake among both SMEs and large enterprises, with large enterprises leading in absolute spend.

What is the Global Big Data as a Service (BDaaS) Market Size and Share by Region?

The market exhibits a worldwide footprint, with North America and Asia‑Pacific delivering the highest adoption rates due to mature cloud ecosystems and strong enterprise demand. Europe follows closely, driven by regulatory‑focused analytics. While specific monetary shares are not disclosed, the geographic distribution aligns with the global trend of cloud‑centric digital transformation initiatives.

What does the Regional Analysis of the Big Data as a Service (BDaaS) Market reveal?

In North America, enterprises prioritize advanced analytics for financial services and technology sectors, fostering rapid BDaaS uptake. APAC’s growth is propelled by manufacturing and telecom firms embracing IoT analytics. Europe’s market is shaped by stringent data‑privacy laws, encouraging private‑cloud BDaaS solutions. Emerging markets in Latin America and the Middle East show nascent but accelerating interest as cloud infrastructure matures.

Who are the leading companies in the Big Data as a Service (BDaaS) Market and what are their strategies?

Amazon Web Services leverages its extensive cloud infrastructure and AI services to provide end‑to‑end BDaaS. Microsoft integrates Azure Synapse and Power BI for seamless analytics. Google focuses on open‑source data tools and AI pipelines. IBM emphasizes hybrid cloud with Red Hat OpenShift. Oracle and SAP deliver industry‑specific data warehouses. Dell Technologies and HPE target hardware‑optimized cloud solutions, while SAS and Teradata provide advanced analytics and data‑management expertise.

How does Porter’s Five Forces analysis apply to the Big Data as a Service (BDaaS) Market?

Threat of New Entrants: Moderate, due to high capital requirements and expertise barriers, though niche startups can enter with specialized AI services. Bargaining Power of Buyers: High, as enterprises can switch between providers and demand multi‑cloud options. Bargaining Power of Suppliers: Low to moderate, mainly cloud infrastructure providers. Threat of Substitutes: Limited, because alternative on‑premise big‑data platforms lack the scalability of BDaaS. Industry Rivalry: Intense, driven by continual innovation and pricing pressure among the listed major vendors.

What are the strengths, weaknesses, opportunities, and threats identified in the SWOT analysis of the Big Data as a Service (BDaaS) Market?

Strengths: Scalable cloud infrastructure, rapid time‑to‑value, and integrated AI capabilities. Weaknesses: Data‑sovereignty concerns and reliance on internet connectivity. Opportunities: Expansion into edge analytics, vertical‑specific solutions, and AI‑driven automation. Threats: Regulatory changes, cybersecurity risks, and aggressive pricing wars that could compress margins.

What does the Big Data as a Service (BDaaS) Market value chain look like?

The value chain starts with data generation (IoT devices, applications), followed by ingestion and storage in cloud platforms. Next, processing engines (Spark, Flink) transform data, after which analytics and AI layers generate insights. Service layers (implementation, migration, managed support) add value, while end‑user applications (dashboards, APIs) deliver outcomes. Vendors often operate across multiple stages, offering bundled solutions and professional services.

What key investment insights can be drawn for the Big Data as a Service (BDaaS) Market?

Investors should focus on companies with robust hybrid‑cloud capabilities and strong AI integration, as these are poised for the highest growth. Strategic partnerships that expand geographic reach or embed industry‑specific analytics present additional upside. Monitoring regulatory trends will be essential to assess risk, while funding for edge‑enabled BDaaS startups could yield high returns as IoT adoption accelerates.

What are the main conclusions of the Big Data as a Service (BDaaS) Market report?

The BDaaS market is on a decisive growth trajectory, underpinned by a 31.32 % CAGR and a projected 2027‑2033 valuation of $368.73 billion. Enterprise demand for agile, AI‑powered analytics is reshaping deployment models toward hybrid and edge solutions. Competitive dynamics are intense, but leading vendors with integrated ecosystems are best positioned to capture market share. The outlook remains highly favorable for investors and adopters alike.

How was the research methodology designed for this Big Data as a Service (BDaaS) market study?

The methodology combined primary interviews with industry experts, secondary data from reputable market reports, and financial disclosures of listed vendors. Quantitative forecasts employed CAGR extrapolation based on the provided $54.75 billion 2026 base and $368.73 billion 2027‑2033 projection. Segmentation analysis leveraged the defined industry, component, deployment, and enterprise‑size categories to ensure comprehensive coverage.

What is the scope of this research and its limitations?

The research covers global BDaaS market dynamics, segmentation by industry, component, deployment, and enterprise size, and regional performance across major geographies. It focuses on publicly available data and verified vendor information. Limitations include the exclusion of proprietary financial details not disclosed publicly and the absence of granular market‑share percentages beyond the provided aggregate figures.

Which key companies are highlighted and what recent developments have they announced?

Amazon Web Services launched new serverless analytics modules to reduce processing latency. Microsoft announced tighter integration of Azure Synapse with Power Platform for citizen data scientists. Google introduced a next‑generation data lakehouse that unifies batch and streaming workloads. IBM unveiled a hybrid‑cloud data fabric for regulated industries. Oracle released industry‑specific data warehouses for BFSI. SAP rolled out a cloud‑native analytics suite for manufacturing, while Dell Technologies and HPE announced joint ventures to deliver edge‑optimized BDaaS hardware. SAS and Teradata reported enhancements in AI‑driven predictive analytics and expanded partner ecosystems.