What is the Electric Insulator Market Overview – definition, scope, and significance?

The Electric Insulator Market encompasses the production and distribution of devices that prevent the unwanted flow of electric current between conductive components. These insulators are critical in power generation, transmission, and distribution systems, ensuring safety, reliability, and efficiency. The market’s scope covers a wide range of product types—shackle, pin, suspension—and material compositions such as ceramic, glass, and composite, serving end‑users like utilities, industrial plants, and other sectors. Their significance lies in safeguarding infrastructure, minimizing outage risks, and supporting the electrification of emerging economies.

What are the Electric Insulator Market drivers, restraints, challenges, and opportunities?

Key drivers include the rapid expansion of power grids, rising renewable‑energy integration, and increased investment in smart‑grid technologies, all demanding higher‑performance insulators. Restraints stem from high material costs, especially for composite and specialty glass products, and regulatory compliance pressures. Challenges involve maintaining performance under harsh environmental conditions and addressing aging infrastructure in developed regions. Opportunities arise from the growth of ultra‑high voltage (UHV) transmission projects, demand for lightweight composite insulators, and the need for insulators in electric‑vehicle charging and data‑center power systems.

What are the current Electric Insulator Market growth trends?

Current trends feature a shift toward composite and polymer‑based insulators, driven by their superior mechanical strength and lower weight. Manufacturers are also investing in advanced ceramic formulations to improve dielectric strength. Digitalization is influencing design, with predictive analytics used to forecast failure rates and optimize maintenance schedules. Additionally, the adoption of modular and plug‑and‑play insulator designs is streamlining installation in transformer and switchgear applications, accelerating project timelines.

How has COVID‑19 impacted the Electric Insulator Market, and what is the recovery trajectory?

The pandemic caused temporary supply‑chain disruptions and project delays in 2020, leading to a short‑term decline in demand. However, stimulus packages for infrastructure and the acceleration of renewable‑energy projects have revitalized the market. Recovery gained momentum in 2021‑2022 as utilities resumed upgrades and new grid expansions. The trajectory remains positive, with demand expected to outpace pre‑COVID levels, bolstered by ongoing electrification initiatives worldwide.

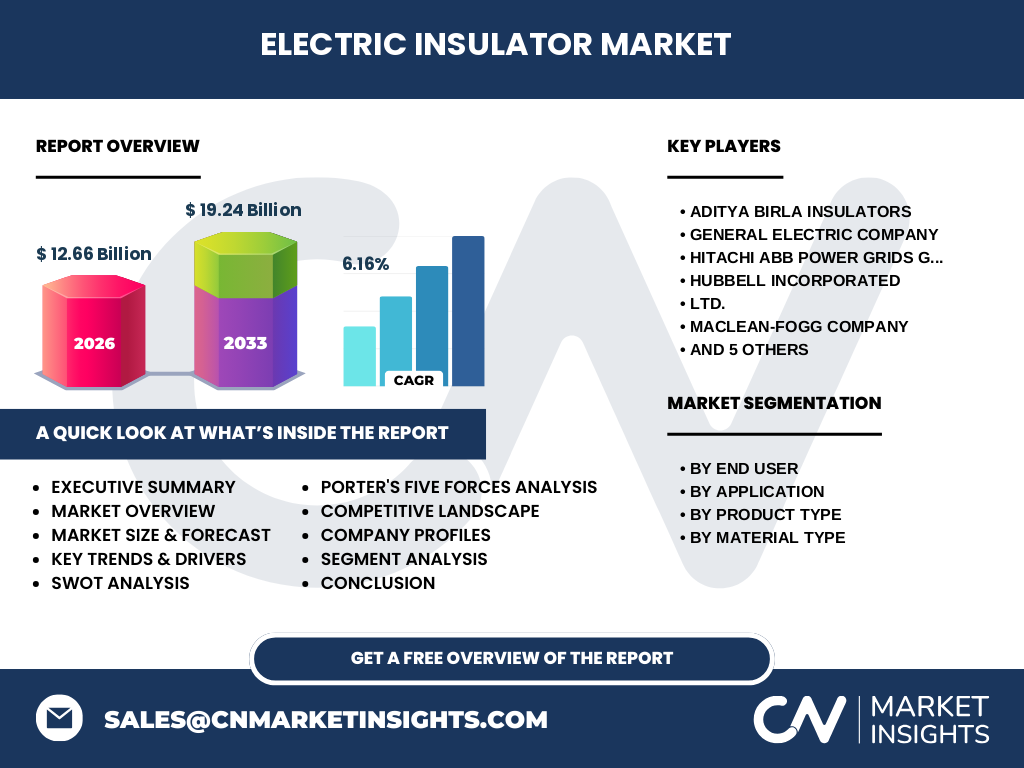

Who are the main competitors in the Electric Insulator Market, and what is the state of market consolidation?

Major players include Aditya Birla Insulators, General Electric Company, Hitachi ABB Power Grids Group, Hubbell Incorporated, MacLean‑Fogg Company, NGK Insulators, PFISTERER Holding AG, SEVES Group, Siemens AG, and TE Connectivity Ltd. The market shows moderate consolidation, with leading firms pursuing strategic acquisitions and joint ventures to broaden product portfolios and geographic reach. Consolidation efforts aim to achieve economies of scale, strengthen R&D capabilities, and secure long‑term supply contracts with utilities.

What are the key findings highlighted in the Executive Summary?

The Electric Insulator Market is valued at $12.66 billion in 2026 and is projected to reach $19.24 billion by 2033, delivering a 6.16 % CAGR. Growth is propelled by utility grid expansions, renewable‑energy integration, and the transition to composite insulators. Regional demand is strongest in emerging economies, while developed markets focus on upgrading aging infrastructure. Competitive dynamics are shaped by technology innovation, strategic partnerships, and an increasing emphasis on sustainability.

What are the Electric Insulator Market forecasts for 2025‑2032?

Based on the provided CAGR of 6.16 %, the market is expected to maintain steady growth throughout the 2025‑2032 period. Forecasts indicate incremental increases in demand across all product and material categories, with composite insulators experiencing the fastest adoption due to their lightweight characteristics. End‑user demand from utilities and industrial sectors will remain the primary revenue drivers, supported by ongoing grid modernization projects and new transmission line construction.

How is the Electric Insulator Market sized and shared by segmentation?

Segmentation analysis reveals three primary dimensions. By end‑user, utilities command the largest share, followed by industries and other end users. Application‑wise, transformer and busbar insulators dominate, with cable, switchgear, surge‑protection devices, and other applications contributing secondary volumes. Product‑type segmentation shows shackle, pin, and suspension insulators distributed according to specific installation requirements. Material segmentation indicates ceramic, glass, and composite insulators, each serving distinct performance and cost criteria across the market.

What is the global Electric Insulator Market size and share by region?

While exact regional monetary values are not disclosed, the market’s global footprint spans North America, Europe, Asia‑Pacific, Middle East & Africa, and Latin America. Asia‑Pacific leads in absolute volume due to extensive grid expansion and renewable‑energy projects, whereas North America and Europe exhibit higher per‑unit pricing driven by stringent safety standards and advanced material usage. Emerging markets in Latin America and the Middle East are showing accelerating growth rates.

What does the regional analysis of the Electric Insulator Market reveal?

Asia‑Pacific’s growth is fueled by China and India’s massive transmission‑line investments and the rollout of UHV networks. Europe focuses on replacing aging insulation with high‑performance composites to meet stricter environmental directives. North America is driven by utility modernization and the adoption of smart‑grid technologies. In the Middle East, oil‑rich nations are diversifying energy portfolios, while Latin America’s expansion is linked to rural electrification programs.

What are the leading company profiles and their strategies in the Electric Insulator Market?

Aditya Birla Insulators leverages cost‑effective ceramic production and strong distribution in emerging markets. General Electric emphasizes integrated solutions linking insulators with digital monitoring. Hitachi ABB Power Grids focuses on high‑voltage composite insulators for UHV projects. Hubbell Incorporated pursues niche applications in industrial switchgear. NGK Insulators drives innovation in glass‑fibre reinforced composites. Siemens AG integrates insulator offerings into its broader power‑system portfolio, while TE Connectivity expands through miniaturized insulator modules for telecom and data‑center use.

How does Porter’s Five Forces analysis apply to the Electric Insulator Market?

Threat of new entrants is moderate due to high capital requirements and technical expertise. Bargaining power of suppliers is limited as raw materials (ceramic, glass, polymer) are widely sourced, though specialty composites can be concentrated. Bargaining power of buyers is relatively strong; large utilities negotiate volume discounts and demand high reliability. Threat of substitutes is low because alternatives to physical insulators are not viable. Industry rivalry is intense, with several global players competing on technology, price, and service contracts.

What are the SWOT elements of the Electric Insulator Market?

Strengths: essential safety component, diversified material base, strong demand from grid expansion. Weaknesses: high material costs, dependence on capital‑intensive projects. Opportunities: composite‑insulator adoption, renewable‑energy integration, emerging‑market electrification. Threats: regulatory changes, supply‑chain disruptions, competition from low‑cost manufacturers.

What does the Electric Insulator Market value chain look like?

The value chain starts with raw‑material procurement (ceramic powders, glass, polymer resins), followed by R&D and product engineering. Manufacturing processes include forming, firing, and coating, after which quality testing ensures compliance. Distribution channels consist of direct sales to utilities, distributors, and OEM partnerships. After‑sales services encompass installation support, maintenance, and performance monitoring, creating recurring revenue streams for manufacturers.

What key investment insights can be drawn for the Electric Insulator Market?

Investors should focus on companies advancing composite technology, as this segment promises higher margins and growth. Partnerships with utilities for long‑term supply contracts can provide stable cash flow. Monitoring policy incentives for grid modernization and renewable‑energy projects will help identify regions with accelerated demand. Finally, firms that integrate digital insulator monitoring solutions are positioned to capture added‑value services.

What are the concluding takeaways from the Electric Insulator Market analysis?

The market is on a robust growth path, underpinned by global electrification and grid‑upgrade initiatives. A 6.16 % CAGR to 2033 reflects strong demand across utilities and industrial users. Technological shifts toward lightweight composites and digital monitoring are reshaping product offerings. Competitive pressure will intensify, rewarding innovators and firms with deep utility relationships. The outlook remains positive for stakeholders willing to invest in advanced materials and service‑centric business models.

How was the research methodology conducted for this report?

The study combined primary interviews with industry experts, surveys of key manufacturers, and secondary data collection from company reports, trade publications, and governmental statistics. Market sizing employed top‑down and bottom‑up approaches, cross‑validated against known financial figures (2026 size $12.66 billion, 2027‑2033 forecast $19.24 billion). Trend analysis utilized scenario modeling to derive the 6.16 % CAGR, while segmentation was built from product catalogs and end‑user usage patterns.

What is the scope of the research and its limitations?

The research covers global Electric Insulator Market dynamics, including product, material, end‑user, and application segments. Geographic coverage spans all major regions, with a focus on markets influencing demand trends. Limitations include reliance on publicly available financial disclosures for some companies and the exclusion of confidential contract values, which may affect precise regional revenue breakdowns.

Which key companies and recent developments are highlighted in the Electric Insulator Market?

Aditya Birla Insulators announced a new ceramic‑insulator plant in India aimed at serving domestic utility upgrades. General Electric launched an IoT‑enabled insulator monitoring platform for its grid customers. Hitachi ABB Power Grids reported a partnership with a Chinese utility to supply composite suspension insulators for a 1,200 kV line. NGK Insulators introduced a high‑strength glass‑fibre composite series for offshore wind farms. Siemens AG acquired a niche insulator‑testing firm to enhance its service portfolio, while TE Connectivity expanded its product line with miniature insulators for 5G infrastructure.