What is the Laminated Busbar Market Overview – definition, scope, and significance?

Laminated busbars are multilayered conductive strips composed of aluminum or copper conductors insulated with materials such as polyester film, heat‑resistant fiber, epoxy powder coating, polyamide film or epoxy glass. They are used to distribute electrical power efficiently in high‑density applications like data centers, telecom hubs, renewable energy converters, and aerospace systems. The market encompasses design, manufacturing, testing, and integration of these components, and its significance lies in enabling compact, lightweight, and high‑current solutions that meet growing demand for energy efficiency and space‑saving electrical infrastructure.

What are the key drivers, restraints, challenges, and opportunities shaping the Laminated Busbar Market?

Drivers include rising power density in data centers, the electrification of transport, and increased adoption of SiC power electronics. Regulatory pressure for greener energy and the need for lightweight aerospace components also boost demand. Restraints stem from high material costs for copper and advanced insulation films, and stringent safety certifications that lengthen time‑to‑market. Challenges involve managing thermal dissipation in compact designs and supply‑chain disruptions for specialty polymers. Opportunities arise from innovations in epoxy glass laminates, partnerships with renewable‑energy OEMs, and expanding applications in electric‑vehicle charging infrastructure.

What are the current growth trends in the Laminated Busbar Market?

The market is moving toward higher current‑carrying capacity using copper‑based cores combined with thin‑film polymer insulators to reduce stack height. Hybrid designs that integrate heat‑resistant fiber layers with epoxy powder coating are gaining traction for high‑temperature environments. Additionally, the adoption of SiC and GaN power modules is prompting the development of busbars with lower inductance and improved frequency response, driving a shift toward more sophisticated, application‑specific laminate structures.

How has COVID‑19 impacted the Laminated Busbar Market and what is the recovery trajectory?

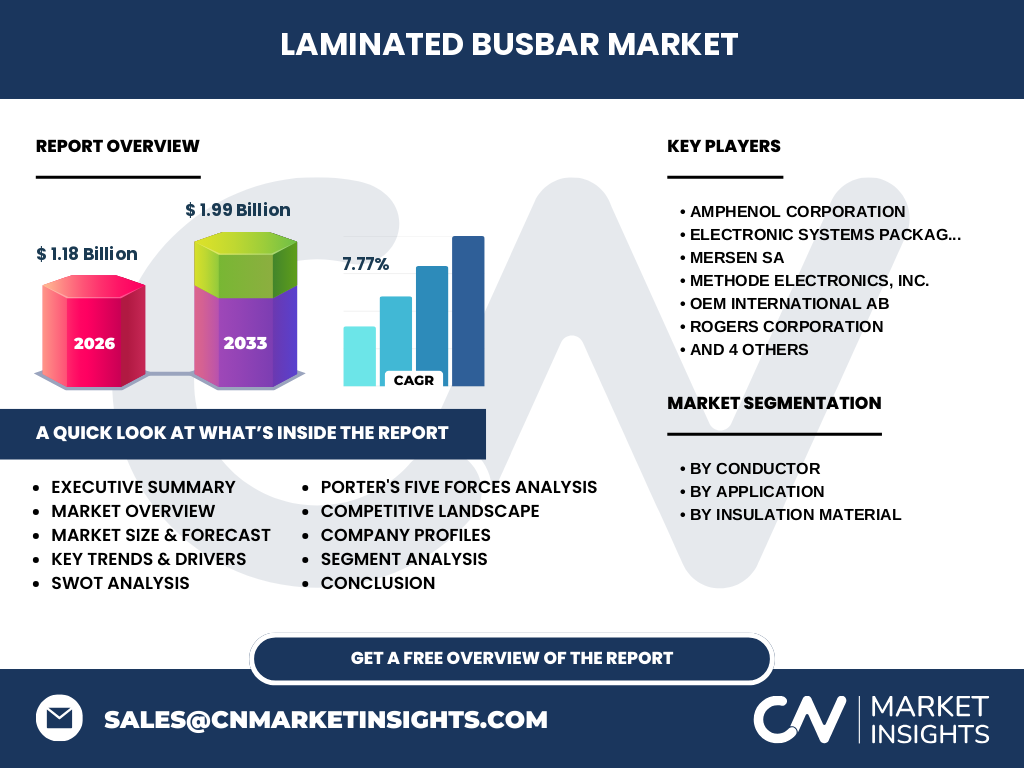

The pandemic caused temporary slowdowns in capital‑intensive projects such as new data‑center builds and aerospace programs, leading to a short‑term dip in orders. However, the rapid acceleration of cloud services and remote work later offset the slowdown, creating a surge in demand for high‑efficiency power distribution. Recovery is now robust, with the market expected to grow at a CAGR of 7.77% through 2033, reflecting a strong post‑pandemic rebound.

Who are the major competitors and what is the level of market consolidation in the Laminated Busbar Market?

Key players include Amphenol Corporation, Electronic Systems Packaging LLC (ESP), Mersen SA, Methode Electronics, Inc., OEM International AB, Rogers Corporation, Ryoden Kasei Co., Ltd., Storm Power Components, Suzhou West Deane Machinery Inc., and Zhuzhou CRRC Times Electric Co., Ltd. The competitive landscape is moderately consolidated, with a few large multinational firms holding significant technological expertise, while numerous specialist manufacturers compete on niche insulation materials and customized designs.

What are the high‑level takeaways presented in the Executive Summary?

The laminated busbar market is valued at $1.18 billion in 2026 and is projected to reach $1.99 billion by 2033, driven by a 7.77% CAGR. Growth is propelled by data‑center expansion, electrified transportation, and advanced power‑electronics applications. While material costs and certification hurdles pose challenges, emerging insulation technologies and strategic collaborations present ample opportunities. The market remains attractive for investors seeking exposure to high‑growth, technology‑intensive segments of the power‑distribution ecosystem.

What are the forecast expectations for the Laminated Busbar Market from 2025 to 2032?

Based on the provided CAGR of 7.77%, the market is expected to expand steadily from its 2026 baseline of $1.18 billion, reaching approximately $1.99 billion by 2033. Annual growth will be driven by continued infrastructure spending in data centers, scaling of electric‑vehicle charging networks, and the rollout of renewable‑energy converters that require compact, high‑current distribution solutions.

How is the Laminated Busbar Market sized and shared by segment?

Segmentation is based on conductor material, application, and insulation type. Conductors are split between aluminum and copper, with copper favored for high‑current, high‑reliability uses. Application categories include data centers, telecom, alternative energy, power electronics & SiC, transportation, aerospace & defense, and industrial sectors, each demanding specific performance characteristics. Insulation materials are diversified across polyester film, heat‑resistant fiber, epoxy powder coating, polyamide film, and epoxy glass, allowing manufacturers to tailor thermal and dielectric properties to distinct end‑use requirements.

What is the geographic distribution of the Global Laminated Busbar Market?

The market is globally distributed, with major demand coming from regions investing heavily in data‑center capacity and renewable‑energy infrastructure. While exact regional figures are not disclosed, North America, Europe, and Asia‑Pacific are primary contributors, reflecting the concentration of high‑tech manufacturing, aerospace programs, and electric‑vehicle adoption in these areas.

Can you provide a detailed regional analysis of the Laminated Busbar Market?

In North America, growth is fueled by large‑scale cloud‑service providers and defense contracts that require lightweight, high‑performance busbars. Europe’s focus on green energy transitions and stringent emissions standards drives demand in alternative‑energy and transportation sectors. Asia‑Pacific leads in manufacturing scale, with rapid expansion of telecom networks, data‑center builds, and electric‑vehicle production, positioning it as a key growth engine for the market.

What are the profiles of leading companies in the Laminated Busbar Market and their strategies?

Amphenol Corporation leverages its broad connector portfolio to cross‑sell laminated busbars to data‑center clients. ESP focuses on custom engineering for aerospace and defense, emphasizing lightweight designs. Mersen SA invests in high‑temperature insulation R&D, while Methode Electronics pursues integration with power‑module manufacturers. OEM International AB expands its footprint in the automotive EV segment, and Rogers Corporation differentiates through advanced polymer films. Ryoden Kasei, Storm Power Components, Suzhou West Deane Machinery, and Zhuzhou CRRC Times Electric add regional strength and specialized manufacturing capabilities.

How does Porter’s Five Forces analysis apply to the Laminated Busbar Market?

Threat of new entrants is moderate due to high capital requirements for precision laminating equipment and certification. Bargaining power of suppliers is moderate to high, especially for copper and specialty polymer films. Bargaining power of buyers is strong; large OEMs demand competitive pricing and customized solutions. Threat of substitutes is low, as alternatives like rigid copper bars cannot match the space‑saving benefits. Competitive rivalry is intense, driven by technology differentiation and price competition among the listed key players.

What are the SWOT insights for the Laminated Busbar Market?

Strengths: High power‑density capability, lightweight construction, and growing application base. Weaknesses: Dependence on costly raw materials and complex manufacturing processes. Opportunities: Expansion into EV charging, SiC power modules, and advanced aerospace programs. Threats: Supply‑chain volatility for copper and specialty insulators, and evolving safety regulations that could increase compliance costs.

What does the value‑chain analysis reveal for the Laminated Busbar Market?

The value chain begins with raw‑material sourcing (copper, aluminum, polymer films), followed by conductor extrusion and lamination processes, insulation coating, precision cutting, and testing for electrical and thermal performance. Afterward, the busbars are integrated into power‑distribution modules by OEMs, and finally sold to end‑users in data centers, automotive, or aerospace. Key value‑adding steps include material innovation and high‑precision lamination, which differentiate premium suppliers.

What key investment insights can be drawn from the Laminated Busbar Market?

Investors should focus on companies with strong R&D pipelines in heat‑resistant insulation and those securing long‑term contracts with data‑center operators or EV manufacturers. Partnerships that blend conductor expertise with advanced polymer technology can yield higher margins. Geographic diversification, especially into fast‑growing Asian markets, further enhances growth potential. Monitoring regulatory trends around energy efficiency will also help identify emerging demand pockets.

What are the concluding takeaways from the Laminated Busbar Market analysis?

The laminated busbar market is on a solid growth trajectory, underpinned by a 7.77% CAGR and a forecasted increase from $1.18 billion to $1.99 billion by 2033. Technological advances in insulation materials and rising demand across data‑center, EV, and aerospace sectors create a robust outlook. While material costs and certification remain challenges, the market offers compelling opportunities for companies that can innovate and secure strategic partnerships.

How was the research methodology designed for this report?

The study combined primary interviews with industry experts, secondary data collection from company filings, trade publications, and market databases, and quantitative modeling using the provided market size, forecast, and CAGR. Segmentation was validated against product catalogs and application briefs, while regional analysis leveraged macro‑economic indicators related to data‑center expansion, renewable‑energy investments, and automotive electrification.

What is the scope of the research and its limitations?

The research covers global laminated busbar production, application segments, conductor and insulation materials, and the competitive landscape up to 2033. It excludes detailed pricing forecasts, proprietary cost structures of individual players, and region‑specific regulatory nuances not publicly disclosed. The analysis is confined to the data points supplied and does not extrapolate beyond the given market size and growth rate.

Which key companies have made notable recent developments in the Laminated Busbar Market?

Amphenol announced a new line of copper‑core busbars optimized for high‑frequency data‑center applications. Mersen SA launched an epoxy‑glass insulated product targeting SiC power modules. Methode Electronics entered a joint venture with an EV‑charging firm to co‑develop lightweight busbars. Rogers Corporation introduced a polyamide‑film variant with enhanced thermal conductivity. These developments illustrate the industry’s focus on material innovation and strategic collaborations to capture emerging opportunities.