What is the Lawn Mower Market Overview – definition, scope, and significance?

The Lawn Mower Market encompasses the design, production, distribution, and sale of equipment used to cut grasses on residential, commercial, and municipal properties. It includes three primary types—push, robotic, and ride‑on mowers—across electric and non‑electric (gas‑powered) categories. The market is significant because lawn care is a core component of property maintenance, influencing real‑estate value, aesthetics, and environmental stewardship. With a 2026 market size of USD 27.78 billion, the sector represents a vital segment of the broader outdoor power equipment industry, driving employment, innovation, and downstream services such as maintenance and accessories.

What are the main drivers, restraints, challenges, and opportunities in the Lawn Mower Market?

Key drivers include rising disposable income, increased home ownership, and a growing preference for automated and eco‑friendly solutions, especially robotic and electric mowers. Urbanization fuels demand for compact, low‑emission equipment in dense residential zones. Restraints arise from seasonal demand fluctuations and rising fuel prices that affect gas‑powered models. Challenges involve strict emissions regulations, supply‑chain disruptions, and consumer hesitation toward high‑cost robotic units. Opportunities are found in battery‑technology advances, connectivity (IoT‑enabled mowers), and service‑based business models such as subscription mowing services.

What are the current growth trends shaping the Lawn Mower Market?

Trend analysis shows a pronounced shift toward electrification; electric and robotic mowers together are capturing a larger share of new sales, driven by sustainability concerns and lower operating costs. Smart features—GPS navigation, app control, and AI‑based grass detection—are becoming differentiators. Ride‑on mowers are gaining traction in commercial landscaping due to productivity gains. Additionally, manufacturers are expanding aftermarket services, offering extended warranties and remote diagnostics to enhance customer loyalty.

How did COVID‑19 impact the Lawn Mower Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and delayed manufacturing, leading to brief inventory shortages. However, lockdowns increased home improvement spending, boosting demand for residential mowers as homeowners invested in outdoor spaces. Post‑pandemic, the market has rebounded strongly, with sales returning to pre‑COVID levels and accelerating as consumers continue to prioritize yard upkeep. The recovery trajectory is positive, supported by strong pent‑up demand and ongoing trends toward automation.

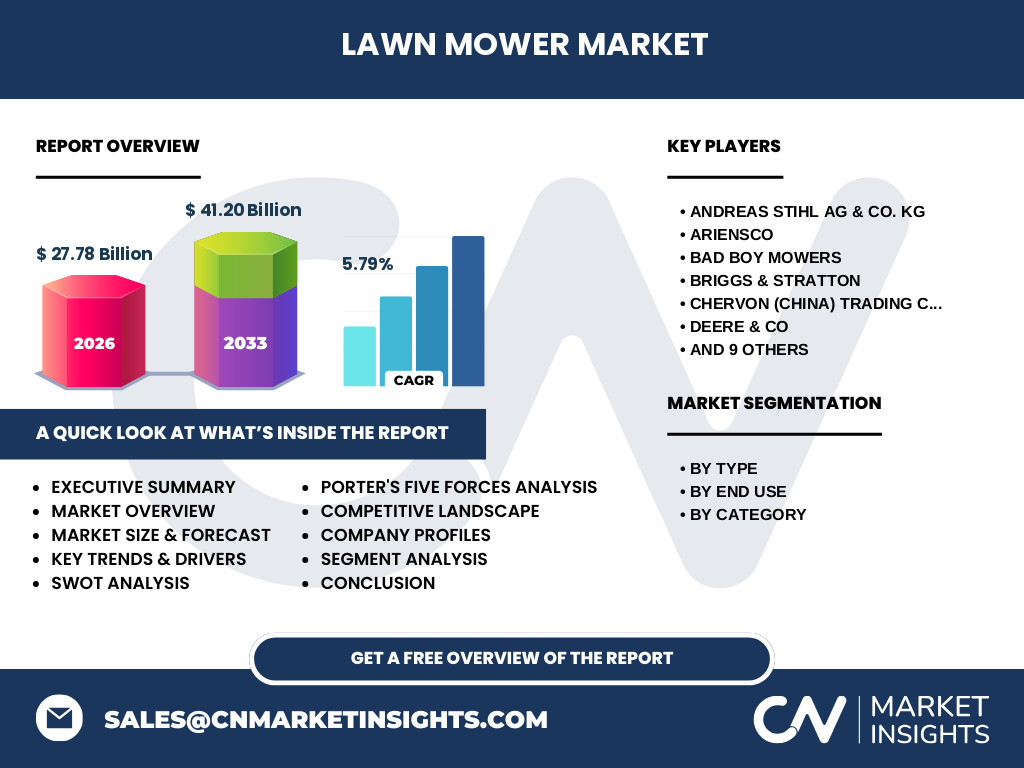

What does the competitive landscape of the Lawn Mower Market look like?

The market is moderately consolidated, with several global and regional players commanding significant brand recognition. Major competitors include Andreas Stihl AG & Co. KG, AriensCo, Bad Boy Mowers, Briggs & Stratton, CHERVON (China) Trading Co. Ltd., Deere & Co, ECHO INCORPORATED, Fiskars Group, Honda Motor Co Ltd, Husqvarna AB, Kubota Corp, Robert Bosch GmbH, Stanley Black & Decker Inc, The Toro Co, and WORX. Strategic moves such as mergers, joint ventures, and product line expansions are common, aiming to capture emerging segments like robotic and electric mowers.

What are the key findings in the Executive Summary of the Lawn Mower Market?

The Lawn Mower Market is valued at USD 27.78 billion in 2026 and is projected to reach USD 41.20 billion by 2033, reflecting a CAGR of 5.79 % over the forecast horizon. Growth is propelled by electrification, smart‑technology adoption, and expanding commercial landscaping activities. While gas‑powered models still dominate the non‑electric segment, regulatory pressure is accelerating the shift to electric and robotic alternatives. Competitive rivalry is intense, with leading manufacturers investing heavily in R&D to differentiate through connectivity and sustainability.

What is the forecast for the Lawn Mower Market from 2025 to 2032?

Based on the provided CAGR of 5.79 %, the market is expected to expand from its 2026 base of USD 27.78 billion to approximately USD 41.20 billion by 2033. This steady growth indicates consistent demand across residential and commercial end‑uses, with electric and robotic categories expected to outpace traditional gas‑powered units. The forecast underscores a robust outlook, encouraging stakeholders to allocate capital toward innovation and capacity expansion.

How is the Lawn Mower Market sized and shared by segmentation?

Segmentation is organized by type, end‑use, and power category. By type, push mowers dominate the residential segment, while ride‑on mowers are prevalent in commercial applications. Robotic mowers, though a smaller share today, are the fastest‑growing sub‑segment due to automation trends. By end‑use, residential customers account for the largest portion of sales, followed by commercial landscaping firms. Within the power category, non‑electric/gas‑powered models currently hold the bulk of volume, but electric units are gaining market share as battery costs decline and emissions standards tighten.

What is the global Lawn Mower Market size and share by region?

The global market reaches USD 27.78 billion in 2026, with the following regional contributions: North America leads due to high home‑ownership rates and advanced consumer preferences for smart equipment. Europe follows, driven by stringent environmental regulations that accelerate electric mower adoption. Asia‑Pacific shows the highest growth potential, propelled by rapid urbanization, expanding middle‑class populations, and increasing commercial landscaping projects. Latin America and the Middle East & Africa remain smaller but are emerging as niche markets for cost‑effective gas models.

What does the regional analysis reveal about the Lawn Mower Market performance?

In North America, demand for robotic and electric push mowers is strong, supported by mature distribution channels and consumer willingness to pay premium prices. Europe’s market is characterized by regulatory pressure, leading to a quicker transition toward zero‑emission mowers. Asia‑Pacific experiences the fastest volume growth, with manufacturers focusing on affordable electric and compact ride‑on models to serve densely populated cities. Latin America’s growth is tied to agricultural and municipal landscaping, favoring durable gas‑powered units.

Which companies lead the Lawn Mower Market and what are their strategies?

Key leaders include Husqvarna AB, known for its robust robotic line; Deere & Co, which leverages its agricultural expertise to dominate ride‑on mowers; and The Toro Co, focusing on residential push and electric models. Companies such as Briggs & Stratton and Honda are expanding into battery‑powered technology via partnerships and acquisitions. Many firms are increasing direct‑to‑consumer sales, investing in digital marketing, and launching subscription‑based mowing services to create recurring revenue streams.

How does Porter’s Five Forces analysis apply to the Lawn Mower Market?

Threat of new entrants is moderate; high capital requirements and brand loyalty deter newcomers, but the rise of smart‑tech startups adds pressure. Bargaining power of suppliers is low to moderate, as component sourcing (motors, batteries) is diversified globally. Bargaining power of buyers is growing, especially in residential segments where consumers compare features and prices online. Threat of substitutes is limited; alternatives like hiring professional services exist but do not replace ownership. Industry rivalry is high, with many established players competing on innovation, price, and after‑sales service.

What are the SWOT insights for the Lawn Mower Market?

Strengths: Established demand, broad product portfolio, and strong brand heritage. Weaknesses: Seasonal sales cycles and dependency on volatile fuel prices for gas models. Opportunities: Electrification, smart‑connected devices, and service‑based business models. Threats: Tightening emissions regulations, supply‑chain disruptions, and increasing competition from tech‑focused entrants.

How is the value chain structured in the Lawn Mower Market?

The value chain begins with raw‑material procurement (steel, plastics, batteries), followed by component manufacturing (engines, motor drives, sensors). Assembly plants—often located in Asia for cost efficiency—produce finished mowers, which are then distributed through wholesale dealers, big‑box retailers, and increasingly through e‑commerce platforms. After‑sales services, including parts, maintenance, and firmware updates for smart models, constitute the downstream segment, adding value and fostering brand loyalty.

What key investment insights can be drawn for the Lawn Mower Market?

Investors should consider allocating capital to companies excelling in electric and robotic technologies, as these segments promise higher margin growth. Partnerships with battery manufacturers or software firms can accelerate product differentiation. Acquiring niche players with proprietary AI or navigation systems offers a shortcut to market leadership. Additionally, targeting emerging markets in Asia‑Pacific through localized production can capture volume growth while mitigating trade‑tariff risks.

What conclusions can be drawn from the Lawn Mower Market analysis?

The Lawn Mower Market is on a clear trajectory of growth, moving from a traditionally gas‑centric industry toward electric and autonomous solutions. A 5.79 % CAGR through 2033 underscores strong demand fundamentals, while regulatory and consumer trends favor eco‑friendly, connected products. Companies that innovate in battery efficiency, IoT integration, and service models are poised to outpace peers and capture the expanding market share.

What research methodology was employed for this Lawn Mower Market report?

The study combines primary interviews with industry executives, distributors, and end‑users, alongside secondary data from company filings, trade journals, and market databases. Quantitative analysis utilizes trend extrapolation based on the provided CAGR of 5.79 % and the base 2026 market size of USD 27.78 billion. Qualitative insights derive from competitor strategy reviews and regulatory assessments.

What is the scope of the research and its limitations?

The research covers global market size, segmentation by type, end‑use, and power category, and regional performance across major geographies. It focuses on the period 2025–2032, using the provided financial figures. Limitations include reliance on publicly available data and the inability to disclose proprietary market share percentages beyond the supplied figures.

Which key companies have recent developments in the Lawn Mower Market?

Husqvarna AB launched a new line of AI‑enhanced robotic mowers with advanced obstacle detection. Deere & Co announced a partnership with a leading battery supplier to introduce a fully electric ride‑on mower for commercial use. The Toro Co expanded its subscription‑based mowing service in North America, bundling equipment leasing with maintenance. Bosch introduced a compact electric push mower featuring integrated smart‑home connectivity. WORX unveiled a cordless, battery‑swap system designed for rapid field exchanges, targeting residential power‑tool enthusiasts.