Thin Film and Printed Battery Market Overview - Definition, scope, and significance?

Thin film and printed batteries are lightweight, flexible energy storage devices fabricated by depositing active materials onto substrates using techniques such as sputtering, vapor deposition, or ink‑jet printing. Their scope spans a broad range of low‑power applications where form‑factor, bendability, and integration with electronics are critical. The market is significant because it enables novel product designs in wearable gadgets, smart packaging, and IoT sensors, driving a shift from rigid, bulkier lithium‑ion chemistries to ultra‑thin, customizable power sources.

Thin Film and Printed Battery Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include the rapid expansion of wearable consumer electronics, the proliferation of medical implantable devices, and increasing demand for smart packaging that requires embedded power. Opportunities arise from advances in printable electrolytes and high‑energy density thin‑film chemistries, as well as government incentives for flexible electronics. Restraints involve relatively low energy density compared with conventional batteries, higher manufacturing costs, and limited long‑term cycle life. Challenges stem from scaling production while maintaining uniformity and meeting stringent safety standards.

Thin Film and Printed Battery Market Growth Trends - Current and emerging trends shaping the market?

The market is witnessing a trend toward multi‑functional batteries that combine energy storage with sensing capabilities, enabling “self‑powered” smart tags. Another emerging trend is the integration of printed batteries directly onto flexible printed circuit boards, reducing assembly steps. Companies are also exploring hybrid architectures that pair thin‑film anodes with printed solid‑state electrolytes, enhancing voltage ratings and cycle stability. Lastly, sustainability initiatives are prompting the development of recyclable and bio‑based printable inks.

COVID-19 Impact on the Thin Film and Printed Battery Market - Pandemic effects and recovery trajectory?

During the pandemic, supply chain disruptions temporarily slowed raw‑material availability, but the surge in remote work and e‑health accelerated demand for wearable health monitors, partly offsetting the slowdown. Post‑2020, the market rebounded strongly, supported by renewed investment in IoT devices and smart packaging for contact‑less deliveries. The recovery trajectory is upward, contributing to the robust CAGR projected for the forecast period.

Thin Film and Printed Battery Market Competitive Landscape - Major competitors and market consolidation?

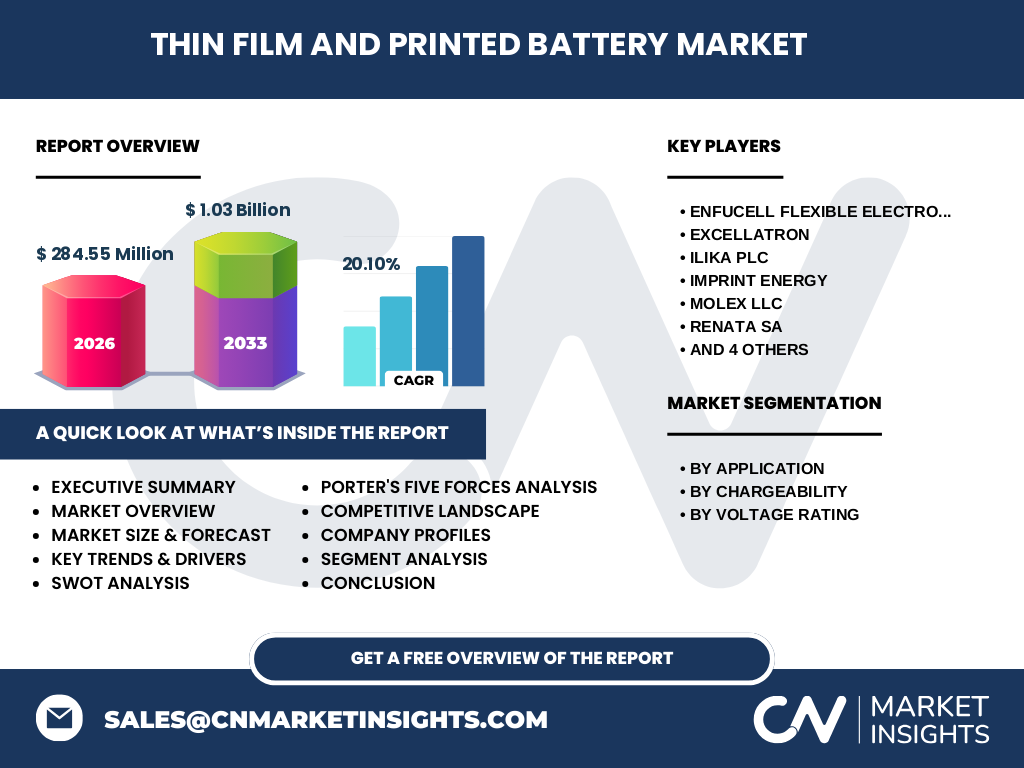

The competitive arena is characterized by a mix of specialized thin‑film innovators and large multinational battery manufacturers expanding into flexible formats. Prominent players include Enfucell Flexible Electronics Ltd, Excellatron, Ilika plc, Imprint Energy, Molex LLC, RENATA SA, STMicroelectronics NV, Samsung SDI Co Ltd, Ultralife Corp, and Varta AG. Consolidation activity is moderate, with strategic partnerships and joint ventures focused on scaling printing technologies and co‑developing high‑voltage chemistries.

Executive Summary - High-level overview and key findings about Thin Film and Printed Battery Market?

The Thin Film and Printed Battery Market is projected to grow from a 2026 valuation of USD 284.55 million to USD 1.03 billion by 2033, reflecting a compound annual growth rate of 20.10 %. Growth is fueled by demand across consumer electronics, medical devices, smart packaging, smart cards, and wireless sensors, as well as by innovations in printable electrolytes and hybrid architectures. Competitive dynamics involve both niche technology firms and established battery giants, creating a vibrant ecosystem poised for rapid expansion.

Thin Film and Printed Battery Market Forecast - Projections for 2025-2032 period?

Based on the current CAGR of 20.10 %, the market is expected to maintain strong momentum throughout the 2025‑2032 horizon. Annual growth will be driven by expanding applications in wearables and IoT, increasing adoption of flexible power sources in medical implants, and the rollout of smart packaging solutions in logistics. The forecast underscores a transition from early‑stage adoption to mainstream commercialization, with revenue crossing the USD 1 billion mark by the early 2030s.

Thin Film and Printed Battery Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by application shows consumer electronics leading, followed by medical devices, smart packaging, smart cards, and wireless sensors. By chargeability, rechargeable variants are gaining traction due to sustainability pressures, while single‑use formats remain important for disposable smart tags. Voltage rating segmentation reveals a concentration in the 1.5‑3 V range, suitable for most low‑power devices, with niche growth in above‑3 V solutions for higher‑performance wearables. Precise numeric shares are not disclosed, but the diversity of segments highlights multiple growth avenues.

Global Thin Film and Printed Battery Market Size and Share by Region - Geographic distribution?

The market exhibits a global footprint with strong activity in North America, Europe, and Asia‑Pacific. North America leads in R&D investments and early adoption in wearable electronics, while Europe emphasizes medical device integration and regulatory support for flexible electronics. Asia‑Pacific drives volume manufacturing, leveraging cost‑effective printing infrastructure and a large consumer base for smart packaging. Each region contributes to the overall market size of USD 284.55 million in 2026.

Regional Analysis of the Thin Film and Printed Battery Market - Detailed regional market performance?

In North America, collaborations between universities and startups accelerate prototype development for smart health monitors. European markets benefit from EU funding programs targeting sustainable electronics, fostering pilot projects in smart cards and secure identification. Asia‑Pacific’s advantage lies in mature printed circuit manufacturing ecosystems, enabling large‑scale production of printed batteries for consumer gadgets and smart packaging. Regional regulatory trends, such as stricter safety standards in Europe, influence product design and certification pathways.

Leading Company Profiles in the Thin Film and Printed Battery Market - Industry players and strategies?

Enfucell Flexible Electronics Ltd focuses on ultra‑thin lithium‑polymer films for wearables. Excellatron specializes in high‑energy printable electrolytes. Ilika plc markets solid‑state thin‑film cells for medical implants. Imprint Energy offers scalable roll‑to‑roll printing platforms. Molex LLC leverages its connector expertise to integrate printed batteries into modular systems. RENATA SA develops low‑voltage printed cells for smart cards. STMicroelectronics NV combines semiconductor know‑how with flexible battery modules. Samsung SDI Co Ltd expands its portfolio into flexible formats, while Ultralife Corp and Varta AG pursue rechargeable thin‑film solutions for industrial IoT.

Porter's Five Forces Analysis of the Thin Film and Printed Battery Market - Competitive forces assessment?

Threat of new entrants is moderate; while low‑cost printing lowers entry barriers, high R&D expenses and IP protection deter many. Bargaining power of suppliers is moderate, as specialty chemicals and substrates are limited to few vendors. Bargaining power of buyers is growing, especially large OEMs seeking customized form factors, driving price pressure. Threat of substitutes is low to moderate, with conventional lithium‑ion cells still dominant but unable to meet flexibility requirements. Industry rivalry is intense, with multiple innovators competing on performance, cost, and integration capabilities.

SWOT Analysis of the Thin Film and Printed Battery Market - Strengths, weaknesses, opportunities, threats?

Strengths: unique form‑factor, lightweight, amenable to integration with flexible electronics. Weaknesses: lower energy density and limited cycle life compared with bulk batteries. Opportunities: emerging wearables, medical implant power supplies, smart packaging, and regulatory pushes for recyclable power sources. Threats: rapid technology evolution could render current chemistries obsolete, and scaling manufacturing while preserving performance remains a critical risk.

Thin Film and Printed Battery Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material suppliers of printable inks, conductive polymers, and thin‑film substrates. Next, R&D firms develop cell architectures and electrochemical formulations. Manufacturing follows, employing roll‑to‑roll printing, vapor deposition, or sputtering lines. Integration partners embed batteries into devices, while system integrators handle testing and certification. Distribution channels include electronic component distributors and direct OEM contracts, culminating in end‑use applications across the five identified segments.

Key Investment Insights in the Thin Film and Printed Battery Market - Strategic investment recommendations?

Investors should prioritize firms with scalable printing platforms and strong IP portfolios in solid‑state electrolytes, as these address both performance and safety concerns. Strategic partnerships with consumer electronics OEMs can accelerate market entry. Funding rounds aimed at hybrid architectures—combining thin‑film anodes with higher‑voltage cathodes—present upside potential. Additionally, monitoring policy incentives for sustainable electronics can uncover grant‑backed growth opportunities.

Thin Film and Printed Battery Market Conclusion - Summary and key takeaways?

The Thin Film and Printed Battery Market is on a steep growth trajectory, projected to more than triple its 2026 size by 2033 with a 20.10 % CAGR. Diverse applications across consumer, medical, and smart‑technology sectors drive demand, while continuous material innovations improve performance. Competitive dynamics feature both specialized innovators and legacy battery giants, creating a fertile environment for investment and partnership. The market’s flexible form‑factor positions it as a cornerstone of next‑generation electronic design.

Research Methodology - How this research was conducted?

The study combined primary interviews with industry experts, technology developers, and key OEMs, together with secondary analysis of company reports, patents, and market databases. Trend extrapolation employed the supplied market size (USD 284.55 million in 2026) and forecast (USD 1.03 billion for 2027‑2033) to calculate the 20.10 % CAGR. Qualitative insights were cross‑validated against publicly available announcements from the listed companies.

Research Scope - Coverage and limitations?

The scope encompasses global market size, segmentation by application, chargeability, and voltage rating, and regional distribution across major geographies. It covers competitive landscape, value chain, and strategic analyses. Limitations include the absence of granular market‑share percentages for individual segments and regions, as these figures were not provided. The report focuses on the defined time horizon up to 2033.

Key Companies and Recent Developments in the Thin Film and Printed Battery Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Enfucell Flexible Electronics Ltd announced a new ultra‑thin cell architecture suitable for foldable smartphones. Excellatron launched a high‑conductivity printable electrolyte that reduces internal resistance. Ilika plc secured a partnership with a leading medical device maker to integrate solid‑state thin‑film batteries into implantable monitors. Imprint Energy unveiled a roll‑to‑roll production line capable of 10,000 m² per hour. Molex LLC introduced a modular connector system embedding printed batteries directly onto PCB panels. RENATA SA released a low‑voltage printed cell for secure smart cards. STMicroelectronics NV demonstrated a hybrid thin‑film module for automotive sensor arrays. Samsung SDI Co Ltd entered a joint venture with a Korean printer manufacturer to mass‑produce flexible batteries. Ultralife Corp expanded its rechargeable thin‑film portfolio for industrial IoT. Varta AG announced a strategic acquisition of a startup specializing in high‑voltage printable cathodes.