What is the Recycled Paper Market Overview – definition, scope, and significance?

The Recycled Paper Market comprises the production, distribution, and consumption of paper products derived from recovered waste fibers, both pre‑consumer (manufacturing scraps) and post‑consumer (used paper). The scope spans raw material sourcing, de‑inking, pulping, and conversion into end‑use categories such as writing and printing paper, containerboard, newsprint, and tissue. Its significance lies in reducing landfill pressure, conserving timber resources, lowering carbon emissions, and meeting growing regulatory and consumer demand for sustainable packaging and office supplies.

What are the main drivers, restraints, challenges, and opportunities in the Recycled Paper Market?

Key drivers include stringent environmental regulations, corporate sustainability goals, and rising consumer preference for eco‑friendly products. Cost advantages from lower virgin fiber prices in certain regions also support growth. Restraints involve the higher processing cost of contaminated waste streams and fluctuating quality of recovered fibers. Challenges stem from competition with virgin paper in niche applications requiring high brightness or strength. Opportunities arise from innovations in fiber‑blending technology, expanded collection infrastructure, and the incorporation of recycled content in new product categories such as e‑commerce packaging.

What are the current growth trends shaping the Recycled Paper Market?

Trend analysis shows a shift toward high‑grade recycled fibers enabling use in premium printing and packaging. The integration of digital printing drives demand for consistent quality recycled paper. Additionally, circular economy initiatives are prompting municipalities to invest in advanced sorting facilities, boosting the supply of clean post‑consumer waste. Companies are also exploring bio‑based additives to improve strength and printability of recycled grades, expanding their applicability across more end‑use segments.

How did COVID‑19 impact the Recycled Paper Market and what is the recovery trajectory?

The pandemic temporarily disrupted waste collection and paper mills due to lockdowns, leading to a short‑term dip in recycled fiber supply. Simultaneously, the surge in remote work increased demand for printing and office paper, partially offsetting the decline. Post‑2020, the market has rebounded as collection services normalized and e‑commerce growth spurred demand for sustainable containerboard. Recovery is steady, supported by renewed corporate sustainability commitments.

Who are the major competitors and what is the level of market consolidation in the Recycled Paper Market?

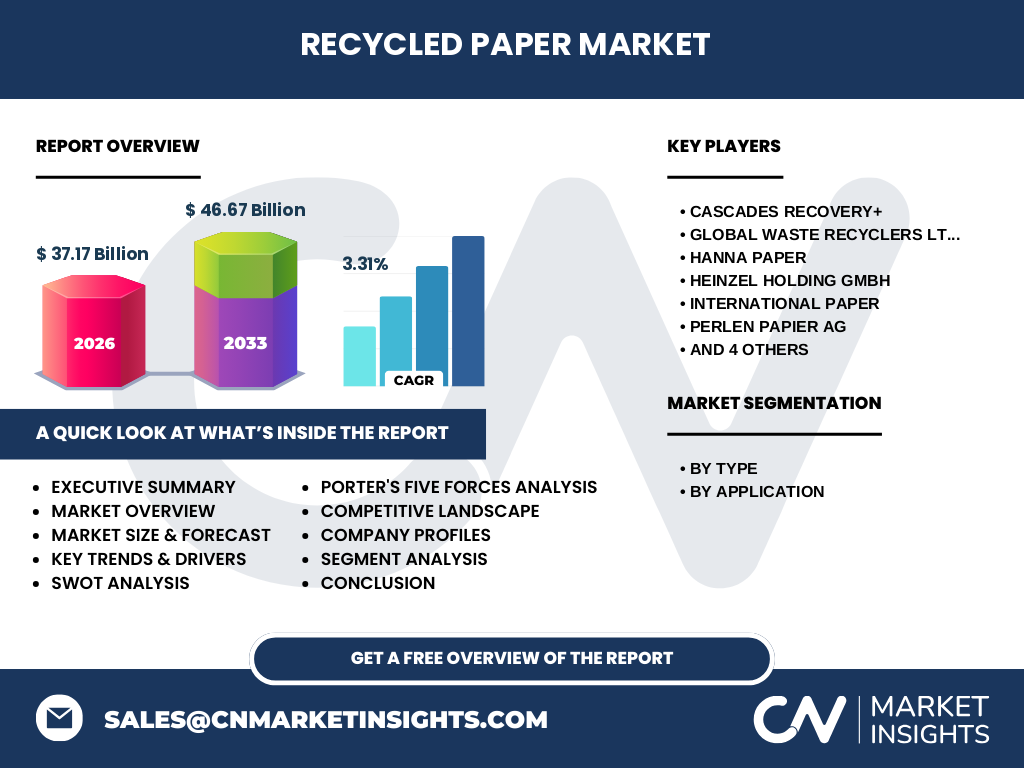

Prominent players include Cascades Recovery+, Global Waste Recyclers Ltd, Hanna Paper, Heinzel Holding GmbH, International Paper, Perlen Papier AG, Republic Services, Inc., ST PAPER RESOURCES PTE LTD, Sonoco Products Company, and WASCO. The market remains moderately fragmented, with a few large integrated recyclers and several regional specialists. Recent years have seen strategic mergers and acquisition activity aimed at expanding collection networks and adding processing capacity, indicating a gradual move toward consolidation.

What are the key findings presented in the Executive Summary of the Recycled Paper Market?

The executive summary highlights a market size of US $37.17 billion in 2026, projected to reach US $46.67 billion by 2033, reflecting a CAGR of 3.31 % over the forecast period. Growth is propelled by regulatory pressure, increasing recycled content mandates, and advances in fiber processing. The pre‑consumer waste segment holds a sizable share due to its higher purity, while containerboard emerges as the fastest‑growing application. Competitive dynamics focus on capacity expansion, product innovation, and vertical integration.

What are the market forecasts for the Recycled Paper Market between 2025 and 2032?

Based on the stated CAGR of 3.31 %, the market is expected to continue expanding steadily through 2032. By 2027, the market value will surpass US $40 billion, with incremental growth each subsequent year driven by escalating demand for sustainable packaging and printing solutions. The forecast underscores consistent year‑over‑year increases, suggesting a resilient market despite macroeconomic fluctuations.

How is the Recycled Paper Market sized and shared by segmentation?

Segmentation by type divides the market into pre‑consumer waste and post‑consumer waste. Pre‑consumer waste generally commands a larger share because of its cleaner feedstock and lower de‑inking costs. By application, the market is split among writing and printing paper, containerboard, newsprint paper, and tissue. Containerboard displays the strongest growth trajectory, driven by e‑commerce packaging, while writing and printing paper remains the largest volume segment due to ongoing office and educational needs.

What is the geographic distribution of the Global Recycled Paper Market size and share?

The global market encompasses North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. While specific regional monetary values are not disclosed, the overall size of US $37.17 billion in 2026 reflects contributions from mature markets such as North America and Europe, which benefit from stringent recycling regulations, as well as fast‑growing Asian economies where expanding packaging demand fuels recycled containerboard consumption.

What does the regional analysis reveal about the performance of the Recycled Paper Market?

North America leads in collection efficiency and infrastructure, supporting steady growth. Europe’s robust Extended Producer Responsibility (EPR) schemes drive high recycled content in paper products. Asia‑Pacific shows the highest growth potential, propelled by rapid industrialization, urbanization, and rising awareness of waste management. Latin America and the Middle East & Africa exhibit nascent but increasing recycling initiatives, suggesting future market entry opportunities.

Which companies are leading in the Recycled Paper Market and what are their strategic approaches?

International Paper leverages its integrated supply chain to offer high‑quality recycled grades. Cascades Recovery+ focuses on expanding its pre‑consumer collection network across North America. Sonoco Products Company invests in advanced de‑inking technologies to enhance product performance. Republic Services, Inc. diversifies into material recovery facilities, while Heinzel Holding GmbH emphasizes sustainable production in Europe. These leaders pursue capacity expansion, technology upgrades, and strategic partnerships to strengthen market position.

How does Porter’s Five Forces assessment apply to the Recycled Paper Market?

• Threat of new entrants: Moderate – capital‑intensive processing and regulatory compliance create barriers, yet growing demand encourages new recyclers. • Bargaining power of suppliers: Low to moderate – waste generators are abundant, but quality variance can affect pricing. • Bargaining power of buyers: Moderate – large paper converters can negotiate for lower recycled content prices. • Threat of substitutes: Low – alternative fibers exist but lack the same functional properties and recycling infrastructure. • Industry rivalry: High – many established players compete on price, quality, and service level.

What are the SWOT strengths, weaknesses, opportunities, and threats for the Recycled Paper Market?

Strengths: Environmental benefits, regulatory support, and increasing consumer demand. Weaknesses: Higher processing costs and variability in waste stream quality. Opportunities: Technological advances in fiber cleaning, expansion into high‑value applications, and emerging markets with developing recycling programs. Threats: Volatile virgin pulp prices, competition from alternative sustainable materials, and potential policy shifts affecting waste collection.

How is the value chain structured in the Recycled Paper Market?

The value chain begins with waste generation (pre‑consumer scraps, post‑consumer paper), followed by collection and sorting. Collected material undergoes transport to recovery facilities where de‑inking, pulping, and bleaching occur. The resulting recycled pulp is then sold to paper converters, who manufacture finished products for end‑users in printing, packaging, and hygiene segments. Ancillary services such as logistics, waste management, and recycling technology providers support the chain.

What key investment insights can be drawn for stakeholders in the Recycled Paper Market?

Investors should target companies with integrated collection‑to‑production capabilities, as they mitigate supply risk. Funding for advanced de‑inking and fiber‑enhancement technologies offers upside potential by unlocking higher‑margin applications. Geographic diversification, especially into Asia‑Pacific, aligns with the fastest growth trajectory. Partnerships with municipalities for guaranteed waste feedstock can provide stable long‑term returns.

What are the concluding takeaways from the Recycled Paper Market analysis?

The recycled paper sector is on a steady growth path, underpinned by sustainability mandates and evolving consumer expectations. With a projected market size of US $46.67 billion by 2033 and a CAGR of 3.31 %, the industry offers attractive opportunities for players that can optimize feedstock quality, innovate product performance, and expand into high‑growth regions. Strategic focus on technology and integrated operations will be critical to capture value.

How was the research methodology designed for this Recycled Paper Market report?

The study employed a mixed‑method approach, combining primary interviews with industry executives, waste management authorities, and key customers, alongside secondary data collection from company filings, government publications, and reputable market databases. Quantitative analysis used the provided market size (US $37.17 billion in 2026) and forecast (US $46.67 billion, CAGR 3.31 %) to model future growth, while qualitative insights informed the assessment of drivers, challenges, and competitive dynamics.

What is the scope of this research and its coverage limitations?

The scope encompasses global recycled paper production, segmentation by waste type and application, and regional performance across major geographies. It includes competitive profiling of the ten listed companies and evaluates macro‑environmental factors. Limitations arise from the reliance on publicly available data and the exclusion of proprietary financial details beyond the provided market figures, which may affect granularity of regional market share estimates.

Which key companies and recent developments are shaping the Recycled Paper Market?

International Paper announced a new high‑strength recycled containerboard line targeting e‑commerce packaging. Cascades Recovery+ expanded its North American pre‑consumer collection network through a partnership with major printing firms. Sonoco Products Company launched an eco‑friendly de‑inking technology that reduces water usage by 20 %. Republic Services, Inc. acquired a regional material recovery facility, enhancing its feedstock security. These developments illustrate a focus on capacity growth, sustainability innovation, and supply chain integration.