What is the Europe Fire Testing Market Overview – definition, scope, and significance?

The Europe Fire Testing Market comprises services that evaluate the fire performance of products, structures, and systems according to European safety standards. It includes testing, inspection, and certification activities across sectors such as building & construction, automotive, industrial manufacturing, consumer goods, and aerospace & defense. The market’s significance lies in safeguarding lives, protecting property, ensuring regulatory compliance, and supporting the development of fire‑resistant technologies throughout the European Union and adjacent economies.

What are the key drivers, restraints, challenges, and opportunities shaping the Europe Fire Testing Market?

Key drivers include stringent EU fire‑safety directives, rising construction activity, and increasing demand for high‑performance materials. Opportunities arise from digitalization of testing methods, growth of renewable‑energy installations, and demand for lightweight automotive components. Restraints involve high testing costs and lengthy certification timelines. Challenges stem from fragmented regulations across member states, talent shortages in specialized testing, and pressure to reduce turnaround times while maintaining rigorous safety standards.

What growth trends are currently influencing the Europe Fire Testing Market?

Current trends feature a shift toward integrated testing solutions that combine fire, thermal, and structural analysis. The adoption of virtual simulation complemented by physical testing is gaining traction, as is the use of portable, on‑site inspection equipment. There is also a noticeable increase in outsourced testing services, driven by manufacturers seeking cost‑effective compliance pathways, and a rise in sustainability‑focused fire‑testing protocols for green building materials.

How did COVID‑19 impact the Europe Fire Testing Market and what is the recovery trajectory?

The pandemic caused temporary laboratory shutdowns, delayed construction projects, and postponed certification schedules, leading to a short‑term dip in testing volume. However, the market rebounded quickly as stimulus funds revived construction and infrastructure programs. Recovery is reinforced by heightened safety awareness and the acceleration of digital testing platforms, positioning the market for a robust post‑COVID growth path.

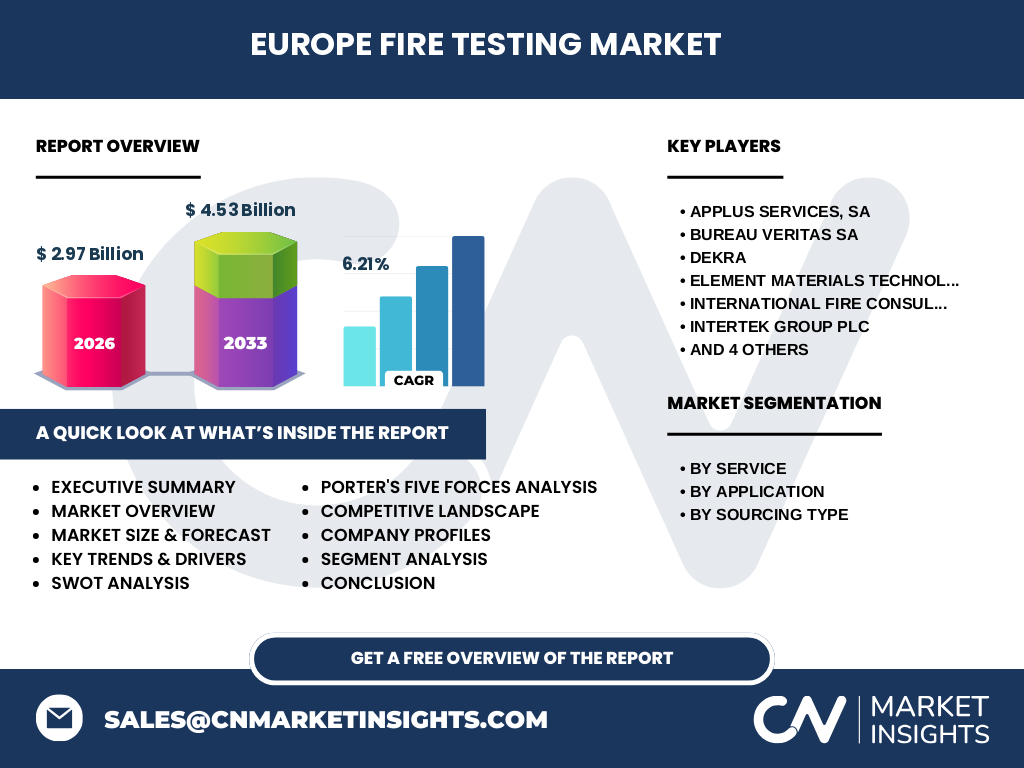

Who are the major competitors in the Europe Fire Testing Market and how is the competitive landscape evolving?

The competitive arena is led by global testing and certification firms such as Applus Services, Bureau Veritas, Dekra, Element Materials Technology, International Fire Consultants Group, Intertek, SGS, TUV SUD, UL, and United Technologies Corporation. Consolidation continues through strategic acquisitions and partnerships, enabling companies to broaden service portfolios, expand geographic reach, and integrate advanced analytics into testing processes.

What are the high‑level findings in the Executive Summary for the Europe Fire Testing Market?

The market is valued at €2.97 billion in 2026 and is projected to reach €4.53 billion by 2033, reflecting a CAGR of 6.21 %. Growth is underpinned by tighter EU regulations, expanding construction and automotive sectors, and increasing reliance on outsourced testing. Digital transformation and sustainability requirements present new avenues for differentiation, while cost pressures and regulatory complexity remain focal challenges.

What is the forecast for the Europe Fire Testing Market from 2025 to 2032?

Based on the provided CAGR of 6.21 %, the market is expected to continue expanding steadily, moving from the 2026 baseline of €2.97 billion toward the 2033 forecast of €4.53 billion. This trajectory indicates consistent demand across all service lines—testing, inspection, and certification—and across all application segments, with particular acceleration anticipated in building & construction and automotive testing.

How is the Europe Fire Testing Market sized and shared by service, application, and sourcing type?

The market is segmented by service into testing, inspection, and certification, each contributing to the total €2.97 billion base. Application-wise, the largest portions come from building & construction and automotive, followed by industrial & manufacturing, consumer goods & retail, and aerospace & defense. Regarding sourcing, both in‑house and outsourced models coexist, with a noticeable shift toward outsourced testing as companies seek expertise and cost efficiency.

What is the geographic distribution of the Europe Fire Testing Market by region?

The market’s geographic footprint spans the major European economies, including Western Europe (Germany, France, UK), Northern Europe (Scandinavia), Southern Europe (Italy, Spain), and Central/Eastern Europe. While exact regional revenue figures are not disclosed, the overall market size of €2.97 billion reflects the collective contribution of these regions, with Western Europe traditionally accounting for the highest concentration of testing activities due to its mature industrial base.

What does the regional analysis reveal about performance within the Europe Fire Testing Market?

Western European nations exhibit strong demand driven by large‑scale construction projects and advanced automotive manufacturing. Northern Europe shows growth linked to renewable‑energy installations that require specialized fire assessments. Southern Europe’s recovery from economic slowdowns is boosting testing volumes, particularly in tourism‑related construction. Central and Eastern Europe are emerging markets where regulatory alignment with EU standards is spurring increased testing and certification engagements.

Which leading companies operate in the Europe Fire Testing Market and what are their strategic approaches?

Key players such as Applus Services, Bureau Veritas, Dekra, and Intertek focus on expanding digital testing platforms and acquiring niche specialists to enhance service depth. SGS and TUV SUD emphasize global network integration to offer consistent cross‑border certification. UL leverages its strong brand in safety standards, while United Technologies Corporation utilizes its engineering expertise to provide integrated fire‑testing solutions for aerospace and high‑tech sectors.

How does Porter’s Five Forces model apply to the Europe Fire Testing Market?

Threat of new entrants is moderate due to high capital requirements and regulatory expertise. Bargaining power of buyers is growing as manufacturers consolidate and demand faster turnaround, pressuring pricing. Supplier power is low because testing labs source standard equipment. Rivalry among existing firms is intense, driven by service differentiation and geographic coverage. The threat of substitutes is limited, as fire testing remains essential for compliance.

What are the SWOT insights for the Europe Fire Testing Market?

Strengths include robust regulatory frameworks and high safety standards. Weaknesses involve fragmented national regulations and high operational costs. Opportunities arise from digital simulation, sustainability‑focused testing, and expansion into emerging economies. Threats encompass potential regulatory changes that could alter testing requirements and increasing competition from low‑cost service providers outside Europe.

How is the value chain structured in the Europe Fire Testing Market?

The value chain starts with standards development (European Committee for Standardization), followed by sample preparation, laboratory testing, data analysis, and final certification or inspection reporting. Supporting activities encompass R&D for new test methods, digital platform development, and after‑sales technical support. Outsourced testing providers sit between manufacturers and certification bodies, adding value through expertise and accelerated timelines.

What investment insights can be drawn for stakeholders interested in the Europe Fire Testing Market?

Investors should consider funding digital transformation initiatives, such as AI‑driven test data analytics, to capture differentiation. Acquiring niche testing labs or forming joint ventures can accelerate market entry in high‑growth regions like Central/Eastern Europe. Sustainable fire‑testing services aligned with green‑building certifications present a compelling growth niche, while maintaining focus on regulatory compliance to mitigate risk.

What are the concluding takeaways for the Europe Fire Testing Market?

The market is on a solid growth path, supported by regulatory rigor and expanding demand across multiple industries. Digitalization and sustainability are key catalysts, while cost management and regulatory harmonization remain critical challenges. Companies that invest in technology, geographic expansion, and strategic partnerships are best positioned to capture market share as the sector moves toward €4.53 billion by 2033.

How was the research methodology designed for this market study?

The study employed a mixed‑method approach, combining primary interviews with industry experts, surveys of key users, and secondary data analysis from regulatory publications, company reports, and reputable market databases. Trend extrapolation used the disclosed CAGR of 6.21 % to project future values, while segmentation was aligned with standard industry classifications for service, application, and sourcing.

What is the defined scope of this research and its limitations?

The scope covers the Europe fire testing ecosystem, focusing on testing, inspection, and certification services across five application sectors and two sourcing models. It includes market size, forecast, competitive landscape, and strategic analyses. Limitations stem from the reliance on publicly available data and the absence of granular regional revenue breakdowns; however, the study provides a comprehensive qualitative and quantitative overview within these parameters.

Which key companies have recent developments, product launches, or partnerships in the Europe Fire Testing Market?

Recent activities include Applus Services expanding its digital testing platform across Germany, Bureau Veritas launching a new fire‑resistance certification for modular construction, Dekra acquiring a niche fire‑testing lab in Poland, Element Materials Technology introducing AI‑enhanced test data interpretation, Intertek partnering with automotive OEMs for rapid certification cycles, SGS opening a state‑of‑the‑art fire laboratory in Scandinavia, and UL releasing a portable fire‑inspection device for field use. These developments highlight a market focused on innovation and collaboration.