1. North America Dried Blueberry Market Overview - Definition, scope, and significance?

The North America Dried Blueberry Market comprises the production, processing, distribution, and consumption of dried blueberry products within the United States, Canada, and Mexico. It includes conventional and organic varieties, multiple processing methods such as freeze‑drying, sun‑drying, and infused drying, and serves end‑uses ranging from bakery and confectionery to beverages and snack bars. Dried blueberries are valued for their high antioxidant content, long shelf life, and versatility, making them a strategic ingredient in health‑focused and convenience food categories across the region.

2. North America Dried Blueberry Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising consumer demand for functional foods, increasing awareness of blueberry health benefits, and expansion of clean‑label and organic product lines. Growth is further supported by the snack‑on‑the‑go trend and the inclusion of dried berries in plant‑based recipes. Restraints stem from price sensitivity relative to fresh berries, supply chain vulnerabilities, and regulatory scrutiny of pesticide residues in conventional crops. Challenges involve meeting consistent quality standards across diverse processing methods. Opportunities arise from product innovation—such as infused dried blueberries with natural flavors—and the acceleration of e‑commerce channels that broaden market reach.

3. North America Dried Blueberry Market Growth Trends - Current and emerging trends shaping the market?

Current trends showcase a shift toward organic dried blueberries, driven by premium pricing and consumer trust in organic certification. Innovation in processing, especially freeze‑drying, is gaining momentum due to its ability to preserve flavor and nutrients. Brands are launching ready‑to‑eat snack packs and integrating dried blueberries into functional beverage blends. Additionally, the rise of direct‑to‑consumer online platforms is reshaping distribution, enabling smaller producers to access niche markets quickly.

4. COVID-19 Impact on the North America Dried Blueberry Market - Pandemic effects and recovery trajectory?

The pandemic triggered a surge in home‑cooking and snacking, boosting demand for shelf‑stable, nutritious options like dried blueberries. Supply chain disruptions initially constrained raw material availability, but manufacturers adapted by diversifying sourcing and increasing inventory buffers. Post‑pandemic, consumer habits remain tilted toward convenient, health‑oriented foods, sustaining the market’s upward trajectory. Recovery is evident in steady volume growth and a faster shift to online purchasing channels.

5. North America Dried Blueberry Market Competitive Landscape - Major competitors and market consolidation?

The market is moderately fragmented, with several established players and niche growers. Leading companies such as CAL SAN Enterprises Ltd., Fruit d’Or, and Graceland Fruit, Inc. dominate through extensive distribution networks and diversified product portfolios. Recent consolidation activity includes strategic acquisitions of smaller organic growers by larger processors, aiming to strengthen supply chain control and broaden organic offerings. Competitive advantage is largely derived from processing technology, brand reputation, and the ability to serve multiple distribution channels.

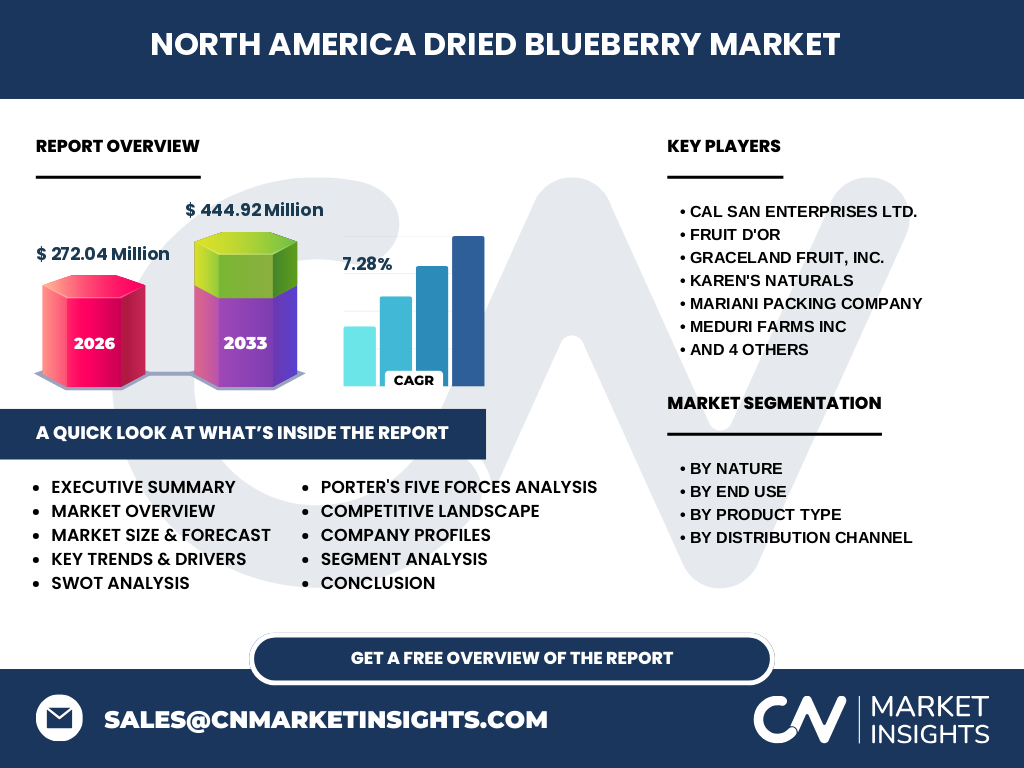

6. Executive Summary - High-level overview and key findings about North America Dried Blueberry Market?

The North America Dried Blueberry Market is projected to expand from a 2026 value of $272.04 million to $444.92 million by 2033, reflecting a robust CAGR of 7.28 %. Growth is driven by health‑centric consumer trends, expanding organic segments, and innovative processing methods. The market exhibits strong diversification across product types, end‑uses, and channels, with online sales gaining traction. Competitive dynamics are shaped by both large processors and agile specialty growers, while opportunities lie in product innovation and supply chain resilience.

7. North America Dried Blueberry Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 7.28 %, the market is expected to maintain steady double‑digit growth through 2032. Annual expansion will be supported by continuous demand from bakery, confectionery, and snack bar manufacturers, as well as increasing incorporation of dried blueberries into functional beverages. The organic segment is anticipated to outpace conventional growth, reflecting premium pricing power. Distribution will further shift toward online platforms, reinforcing overall market momentum.

8. North America Dried Blueberry Market Size and Share by Segmentation - Breakdown by segment?

Segmentation analysis reveals four primary dimensions: Nature (Conventional vs. Organic), End Use (Bakery Products, Confectionaries, Dairy Products, Beverages, Cereal & Snack Bars), Product Type (Freeze Dried, Sun Dried, Infused Dried), and Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online). Organic products command higher price points and are gaining share within health‑focused end uses such as dairy and snack bars. Freeze‑drying holds the largest share among product types due to superior nutrient retention, while online channels are the fastest‑growing distribution segment.

9. Global North America Dried Blueberry Market Size and Share by Region - Geographic distribution?

Within the global dried blueberry landscape, North America represents a leading consumer base, driven by high disposable income and strong demand for functional snacks. Although specific regional share percentages are not disclosed, the market’s $272.04 million valuation in 2026 underscores its significance relative to other regions. Growth is concentrated in the United States, with Canada and Mexico contributing emerging demand, particularly in organic and specialty product niches.

10. Regional Analysis of the North America Dried Blueberry Market - Detailed regional market performance?

The United States dominates the regional performance, leveraging extensive processing infrastructure and a mature retail network across supermarkets, hypermarkets, and convenience stores. Canada shows steady growth, especially in organic segments aligned with national health initiatives. Mexico’s market is emerging, with increased adoption of dried berries in snack bars and confectionery driven by rising middle‑class consumption. Across all three countries, online sales are accelerating, narrowing the gap between urban and rural market penetration.

11. Leading Company Profiles in the North America Dried Blueberry Market - Industry players and strategies?

Key companies include CAL SAN Enterprises Ltd., known for large‑scale freeze‑drying facilities and a broad organic portfolio; Fruit d’Or, which emphasizes premium sun‑dried varieties and strategic retail partnerships; Graceland Fruit, Inc., focusing on infused dried products with natural flavor infusions; Karen’s Naturals, a niche organic grower expanding its e‑commerce footprint; Mariani Packing Company, leveraging vertical integration to control quality from farm to pack; Meduri Farms Inc., emphasizing sustainable farming practices; Naturipe Farms, LLC, with a strong presence in the frozen segment; Oregon Berry Packing, Inc., targeting specialty snack manufacturers; Shoreline Fruit LLC, focusing on private‑label collaborations; and True Blue Farms, which innovates with functional blends for beverage applications.

12. Porter's Five Forces Analysis of the North America Dried Blueberry Market - Competitive forces assessment?

Threat of New Entrants: Moderate – entry barriers include capital‑intensive processing equipment and certification requirements for organic labeling. Bargaining Power of Suppliers: Low to moderate – growers are numerous, but premium organic farms can command higher prices. Bargaining Power of Buyers: High – retailers and food manufacturers demand consistent quality, competitive pricing, and reliable supply, prompting price negotiations. Threat of Substitutes: Moderate – fresh blueberries, other dried berries, and manufactured fruit snacks compete on taste and convenience. Industry Rivalry: Intense – firms differentiate through processing technology, organic credentials, and channel diversification.

13. SWOT Analysis of the North America Dried Blueberry Market - Strengths, weaknesses, opportunities, threats?

Strengths: Strong health positioning, long shelf life, and versatile applications. Weaknesses: Higher cost compared with fresh berries and sensitivity to supply chain disruptions. Opportunities: Expansion of organic and infused product lines, growth of online distribution, and partnerships with plant‑based food manufacturers. Threats: Volatile raw material pricing, regulatory changes affecting pesticide limits, and competition from alternative dried fruits and synthetic functional ingredients.

14. North America Dried Blueberry Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with blueberry cultivation (conventional and organic farms), followed by harvesting and primary cleaning. Next, processing stages—freeze drying, sun drying, or infusion—add value through moisture reduction and flavor enhancement. Post‑processing includes packaging (often resealable pouches) and labeling for organic or premium claims. Distribution then occurs through three main channels: supermarkets & hypermarkets, convenience stores, and online platforms, each requiring distinct logistics and inventory management. End‑users—food manufacturers and direct consumers—complete the chain.

15. Key Investment Insights in the North America Dried Blueberry Market - Strategic investment recommendations?

Investors should prioritize companies with proven freeze‑drying capabilities and strong organic certifications, as these segments command premium pricing. Funding supply‑chain resilience—such as diversified sourcing and advanced storage—mitigates raw material risk. Partnerships with snack‑bar innovators and beverage formulators can unlock new end‑use applications. Additionally, allocating capital to e‑commerce fulfillment infrastructure will capture the fastest‑growing distribution channel.

16. North America Dried Blueberry Market Conclusion - Summary and key takeaways?

The market demonstrates robust growth, underpinned by health‑centric consumer preferences, innovative processing, and expanding distribution avenues. With a projected CAGR of 7.28 % and a market size reaching $444.92 million by 2033, opportunities abound for players that can deliver organic, high‑quality products through both traditional retail and digital channels. Strategic focus on value‑added processing, supply chain stability, and brand differentiation will be critical for sustained success.

17. Research Methodology - How this research was conducted?

The analysis combines primary interviews with industry executives, secondary data from company reports, trade publications, and government statistics. Market sizing employed a bottom‑up approach, aggregating volume and price data from key players. Forecasting applied compound annual growth rate methodology based on historical trends and forward‑looking indicators such as consumer demand and channel expansion. Competitive mapping leveraged SWOT and Porter’s frameworks to evaluate strategic positioning.

18. Research Scope - Coverage and limitations?

The study covers the North American region, encompassing the United States, Canada, and Mexico, and includes conventional and organic dried blueberries across all major processing types, end uses, and distribution channels. While the report captures macro‑level trends and financial projections, granular market share percentages for individual companies or sub‑regional breakdowns are not disclosed due to data confidentiality.

19. Key Companies and Recent Developments in the North America Dried Blueberry Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent activities include CAL SAN Enterprises Ltd. launching a new line of organic freeze‑dried blueberries aimed at the snack‑bar sector; Fruit d’Or announcing a partnership with a major U.S. retailer to feature sun‑dried blueberries in its private‑label bakery range; Graceland Fruit, Inc. introducing infused dried blueberries with natural cinnamon and vanilla flavors for beverage mixers; Karen’s Naturals expanding its online subscription service for health‑focused consumers; Mariani Packing Company securing a contract with a leading cereal manufacturer for fortified snack bars; Meduri Farms Inc. adopting sustainable irrigation practices to reduce production costs; Naturipe Farms, LLC. enhancing its cold‑chain logistics for freeze‑dried exports; Oregon Berry Packing, Inc. collaborating with a confectionery brand for berry‑filled chocolates; Shoreline Fruit LLC. developing private‑label solutions for convenience stores; and True Blue Farms unveiling a functional blueberry blend designed for plant‑based protein shakes.