What is the Embolization Devices Market Overview – Definition, scope, and significance?

The Embolization Devices Market comprises medical products designed to block blood flow to targeted vessels for therapeutic purposes. Devices such as coils, plugs, beads, and glues are employed across a variety of clinical specialties to treat bleeding, aneurysms, tumors, and vascular malformations. The market’s scope includes manufacturing, distribution, and clinical adoption of these devices in hospitals and ambulatory centers worldwide. Its significance derives from the growing prevalence of chronic vascular conditions, the expansion of minimally invasive procedures, and the clinical advantages of embolization—namely reduced operative time, shorter hospital stays, and lower complication rates compared with open surgery.

What are the main drivers, restraints, challenges, and opportunities shaping the Embolization Devices Market?

Key drivers include rising incidence of neurovascular disorders, peripheral vascular disease, and oncology cases that require precise vascular control; increasing adoption of image‑guided minimally invasive techniques; and strong reimbursement frameworks in major healthcare systems. Restraints arise from high device acquisition costs, stringent regulatory pathways, and limited awareness in emerging economies. Challenges involve the need for continuous product innovation to address complex anatomies and the risk of procedural complications that can affect physician confidence. Opportunities exist in expanding indications for embolization (e.g., urology), developing bio‑resorbable materials, and leveraging digital health platforms for procedural planning and post‑procedure monitoring.

Which growth trends are currently influencing the Embolization Devices Market?

Current trends feature a shift toward hybrid devices that combine embolic materials with drug‑eluting capabilities, enabling simultaneous occlusion and localized chemotherapy. There is also a noticeable rise in the use of 3‑D imaging and navigation systems that improve placement accuracy, fostering higher demand for advanced coils and plugs. Additionally, the market is witnessing increased consolidation as larger med‑tech firms acquire niche innovators to broaden their product portfolios and geographic reach.

How did COVID‑19 impact the Embolization Devices Market and what is the recovery trajectory?

The pandemic caused a temporary decline in elective procedures, slowing device shipments in 2020–2021. However, because many embolization interventions are classified as urgent or semi‑elective (e.g., treatment of ruptured aneurysms), demand rebounded quickly once hospitals resumed normal operations. Post‑pandemic, the market benefitted from a backlog of delayed cases, accelerating growth and reinforcing the importance of minimally invasive techniques that reduce hospital length of stay—a critical factor during infectious disease surges.

What does the competitive landscape of the Embolization Devices Market look like?

The market is moderately concentrated with several multinational corporations and specialized manufacturers. Major competitors such as Abbott Laboratories, Boston Scientific Corp, Cook Medical Holdings LLC, Medtronic Plc, Stryker Corp, and Terumo Corp dominate the high‑volume segments, while companies like GEM srl, INVAMED, and Sirtex Medical Ltd focus on niche technologies. Recent consolidation activity includes strategic acquisitions aimed at expanding product lines and geographic presence, intensifying competition on both innovation and pricing.

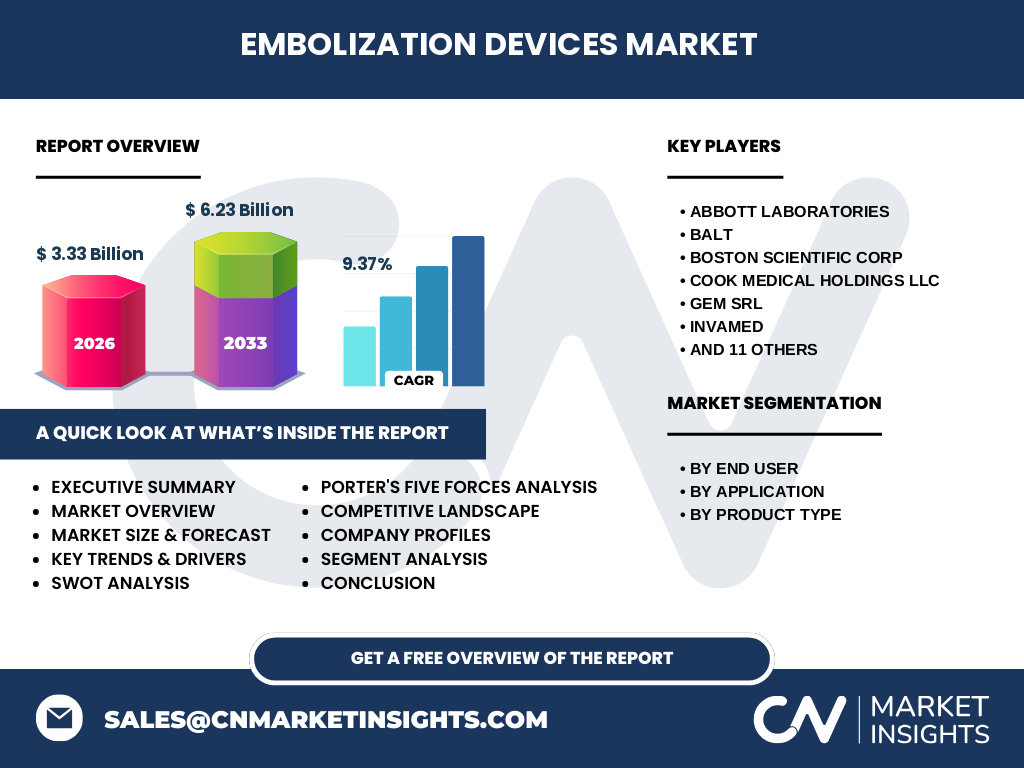

Can you provide an executive summary of the Embolization Devices Market?

The Embolization Devices Market is valued at $3.33 billion in 2026 and is projected to reach $6.23 billion by 2033, delivering a robust CAGR of 9.37 %. Growth is propelled by expanding clinical indications, advances in imaging‑guided delivery, and strong demand for minimally invasive solutions. While cost pressures and regulatory complexity present hurdles, the market offers significant upside through product differentiation, geographic expansion, and integration of drug‑eluting technologies. Competitive dynamics are shaped by a mix of large med‑tech players and agile innovators, fostering a vibrant environment for continued innovation.

What are the forecast expectations for the Embolization Devices Market through 2032?

Based on the stated CAGR of 9.37 %, the market is expected to maintain a steady upward trajectory from its 2026 base of $3.33 billion, reaching approximately $6.23 billion by the end of 2033. This projection suggests that the market will more than double over a seven‑year horizon, driven by sustained adoption of embolization across neurology, peripheral vascular disease, oncology, and emerging urology applications.

How is the Embolization Devices Market sized and shared by segmentation?

Segmentation is structured around three primary dimensions. By end‑user, hospitals hold the larger share due to the complexity of most embolization procedures, while ambulatory centers capture a growing niche as technology becomes more portable. By application, neurology leads the market because of the high prevalence of cerebral aneurysms, followed by peripheral vascular disease, oncology, and an emerging urology segment. By product type, embolization coils dominate owing to their versatility and long‑track record, with plugs, beads, and glues each representing important, though smaller, sub‑segments that cater to specific clinical needs.

What is the global geographic distribution of the Embolization Devices Market?

The market exhibits a truly global footprint, with developed regions such as North America and Europe accounting for a substantial portion of sales due to advanced healthcare infrastructure and early adoption of innovative technologies. Asia‑Pacific shows the fastest growth rate, driven by expanding hospital networks, rising middle‑class populations, and increasing prevalence of vascular disorders. Latin America and the Middle East & Africa present emerging opportunities as reimbursement policies evolve and local manufacturers expand capabilities.

Can you detail the regional analysis of the Embolization Devices Market?

In North America, the market benefits from high procedure volumes, strong R&D investment, and a supportive regulatory environment, with the United States being the primary revenue generator. Europe’s market is characterized by fragmented national health systems, yet strong adoption of embolization in countries such as Germany, France, and the United Kingdom. Asia‑Pacific’s growth is underpinned by rapid urbanization, increased access to minimally invasive therapies, and rising disease burden in China, Japan, and India. Latin America and the Middle East & Africa remain smaller but are poised for growth as local healthcare spending rises and foreign direct investment in medical technology escalates.

Which companies lead the Embolization Devices Market and what are their strategic approaches?

Leading firms include Abbott Laboratories, Boston Scientific Corp, Cook Medical Holdings LLC, Medtronic Plc, Stryker Corp, and Terumo Corp. Their strategies focus on expanding product portfolios through R&D and acquisition, forging partnerships with interventional radiology societies, and pursuing regulatory approvals for novel embolic agents. Smaller innovators such as GEM srl, INVAMED, and Sirtex Medical Ltd differentiate through specialized technologies like radiopaque coils or targeted cancer embolization platforms, often collaborating with larger players to achieve broader market access.

How does Porter’s Five Forces analysis apply to the Embolization Devices Market?

• Threat of New Entrants: Moderate; high regulatory barriers and capital intensity limit easy entry, yet niche innovators can penetrate with specialized products.

• Bargaining Power of Suppliers: Low to moderate; raw material suppliers are numerous, but specific high‑purity polymers and radiopaque agents can command higher prices.

• Bargaining Power of Buyers: Moderate; large hospital systems and purchasing groups negotiate pricing, but clinical efficacy and safety data give manufacturers leverage.

• Threat of Substitutes: Low; alternative therapies (e.g., surgical resection) are more invasive, keeping embolization as the preferred minimally invasive option.

• Industry Rivalry: High; competition is driven by product differentiation, clinical outcomes, and price positioning among a mix of global giants and specialized firms.

What are the SWOT highlights for the Embolization Devices Market?

Strengths: Proven clinical benefits, expanding therapeutic indications, and robust growth outlook.

Weaknesses: High device cost and dependence on advanced imaging infrastructure.

Opportunities: Development of bio‑resorbable and drug‑eluting embolics, penetration into emerging markets, and integration with AI‑guided navigation.

Threats: Regulatory delays, potential market saturation in mature regions, and macro‑economic pressures that could constrain hospital budgets.

What does the value chain of the Embolization Devices Market look like?

The value chain starts with raw material suppliers (polymers, metals, radiopaque agents), progresses to device design and R&D, followed by manufacturing, quality control, and regulatory approval. Distribution channels include direct sales to hospitals, distributors, and third‑party logistics providers. End‑users—interventional radiologists, vascular surgeons, and neuro‑interventionists—provide feedback that loops back into product improvement and next‑generation development.

What key investment insights can be drawn from the Embolization Devices Market?

Investors should target companies with diversified product portfolios across the four application areas and a clear pipeline for next‑generation embolic agents. Strategic M&A opportunities exist in acquiring niche innovators with proprietary technologies. Geographic diversification, especially into fast‑growing Asia‑Pacific markets, can enhance portfolio resilience. Finally, firms that align with digital health trends—such as AI‑assisted planning and remote monitoring—are likely to capture premium pricing and strengthen long‑term market position.

What conclusions can be drawn about the Embolization Devices Market?

The Embolization Devices Market is poised for robust expansion, underpinned by a 9.37 % CAGR and a projected market size of $6.23 billion by 2033. Clinical demand across neurology, peripheral vascular disease, oncology, and urology drives sustained growth, while technological innovation and geographic expansion open new revenue streams. Despite cost and regulatory hurdles, the market’s favorable risk‑return profile makes it an attractive focus for manufacturers, investors, and healthcare providers seeking to capitalize on minimally invasive treatment pathways.

How was the research for this report conducted?

Research combined primary interviews with key opinion leaders, surveys of major hospitals and ambulatory centers, and secondary analysis of regulatory filings, company annual reports, and reputable industry databases. Trend extrapolation utilized the provided CAGR of 9.37 % to project market size through 2033. Competitive insights were derived from publicly disclosed mergers, acquisitions, product launches, and pipeline disclosures of the listed companies.

What is the scope of this research?

The study covers global market dynamics for embolization devices, segmented by end‑user (hospitals, ambulatory centers), application (neurology, peripheral vascular disease, oncology, urology), and product type (coils, plugs, beads, glues). Geographic coverage includes all major regions, with emphasis on performance drivers in North America, Europe, and Asia‑Pacific. The scope excludes unrelated vascular accessories and focuses strictly on devices employed for therapeutic embolization.

Which key companies and recent developments are highlighted in the Embolization Devices Market?

Among the leading players, Abbott Laboratories launched a next‑generation radiopaque coil system with enhanced visibility under fluoroscopy. Boston Scientific announced a partnership with a AI‑based imaging platform to improve coil placement accuracy. Cook Medical introduced a bio‑resorbable plug designed for peripheral interventions. Medtronic secured regulatory approval for a drug‑eluting bead portfolio targeting hepatic tumors. Stryker expanded its presence in Asia‑Pacific through a joint venture with a local distributor. Recent developments also include Sirtex Medical’s acquisition of a specialty bead manufacturer to broaden its oncology embolization offerings.