Operating Tables Market Overview - Definition, scope, and significance?

The Operating Tables market comprises medical devices designed to support patients during surgical procedures across diverse healthcare settings. These tables range from basic non‑powered models to advanced powered and radiolucent systems, catering to general, specialty, pediatric, and ambulatory surgeries. The scope of the market includes manufacturing, distribution, and aftermarket services for tables used in hospitals, ambulatory surgical centers, and specialty clinics worldwide. The significance lies in its direct impact on surgical precision, patient safety, and operational efficiency, making operating tables a critical component of modern operating rooms and a prerequisite for high‑quality clinical outcomes.

Operating Tables Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising global surgical volumes driven by aging populations, increased prevalence of chronic diseases, and expanding healthcare infrastructure in emerging economies. Technological advancements such as ergonomic designs, integrated imaging compatibility, and smart sensor integration further stimulate demand. Restraints stem from high capital costs, especially for powered and specialty tables, and stringent regulatory requirements that lengthen product launch timelines. Challenges involve maintaining equipment uptime in resource‑constrained facilities and addressing compatibility with diverse surgical tools. Opportunities arise from the growing adoption of minimally invasive and robotic surgeries, which require specialized tables, and from service‑based revenue models such as leasing, maintenance contracts, and table upgrades.

Operating Tables Market Growth Trends - Current and emerging trends shaping the market?

Current trends highlight a shift toward powered and radiolucent tables that facilitate imaging procedures and improve ergonomics for surgeons. The integration of IoT sensors for real‑time table positioning data and maintenance alerts is emerging, enhancing preventive service strategies. Additionally, manufacturers are expanding product portfolios to include pediatric and specialty surgery tables, responding to niche clinical needs. Sustainability trends are prompting the use of recyclable materials and energy‑efficient mechanisms, while digital twin technologies are being piloted to simulate table performance and optimize design.

COVID-19 Impact on the Operating Tables Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially disrupted the Operating Tables market as elective surgeries were postponed, leading to a temporary dip in demand. However, the crisis accelerated hospital investments in flexible operating room solutions capable of handling infectious cases, boosting demand for easily sterilizable, non‑powered tables. Post‑pandemic, the market has entered a robust recovery phase, driven by the resurgence of elective procedures and heightened focus on infection control, positioning the market for steady growth through 2032.

Operating Tables Market Competitive Landscape - Major competitors and market consolidation?

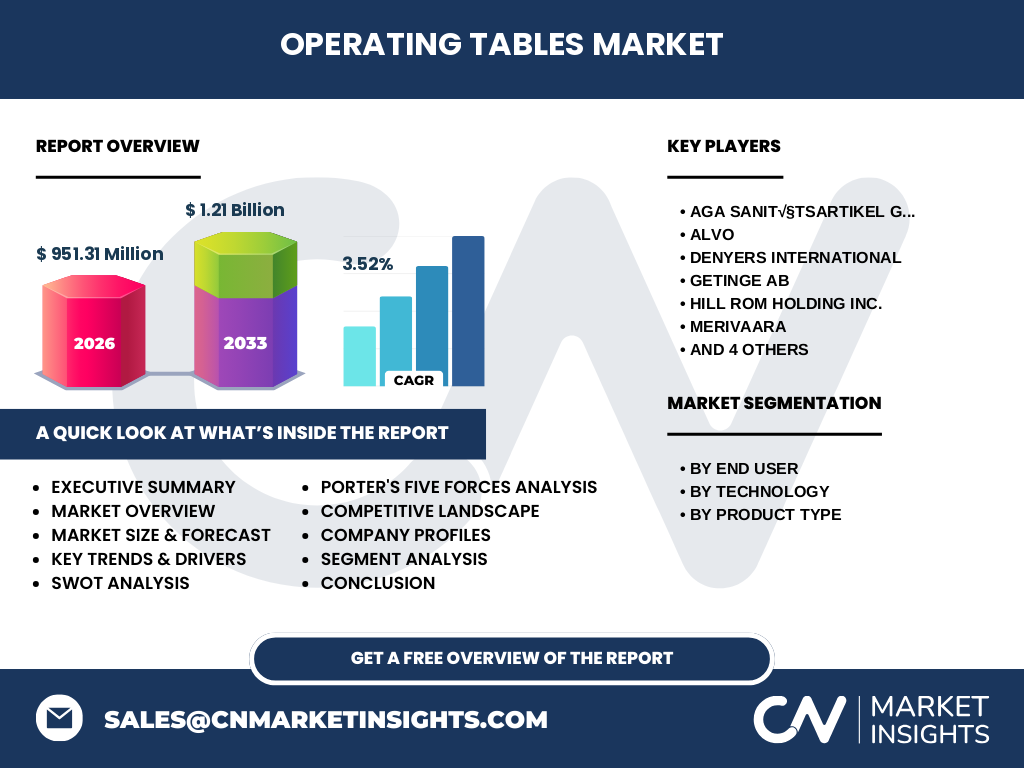

The competitive landscape is characterized by a mix of established multinational manufacturers and specialized regional players. Key competitors include AGA Sanitätsartikel GmbH, Alvo, Denyers International, Getinge AB, Hill Rom Holding Inc., Merivaara, Mizuho Medical, Skytron, LLC., Steris PLC, and Stryker Corporation. Over the past few years, the market has seen moderate consolidation through strategic acquisitions and joint ventures aimed at expanding product portfolios and geographic reach, reinforcing the dominance of these leading firms.

Executive Summary - High-level overview and key findings about Operating Tables Market?

The Operating Tables market was valued at USD 951.31 million in 2026 and is projected to reach USD 1.21 billion by 2033, reflecting a CAGR of 3.52 % over the forecast horizon. Growth is propelled by expanding surgical volumes, technological innovations, and rising adoption of specialized tables in hospitals, ambulatory surgical centers, and specialty clinics. The market is fragmented yet led by ten major manufacturers who are actively pursuing product differentiation and service‑based offerings. Regional demand is strongest in North America and Europe, with emerging opportunities in Asia‑Pacific driven by healthcare infrastructure investments.

Operating Tables Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 3.52 %, the market is expected to continue expanding steadily from 2025 through 2032. By 2027, the market will approach the USD 1 billion mark, and by 2032 it will be close to the projected USD 1.21 billion figure for 2033. The forecast reflects sustained demand for both powered and specialty tables, with incremental growth supported by ongoing healthcare reforms, increased procedural volumes, and continuous product innovation.

Operating Tables Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by end‑user shows hospitals as the largest consumer, followed by ambulatory surgical centers and specialty clinics. By technology, powered tables are gaining market share due to their ergonomic benefits, while non‑powered tables retain relevance in cost‑sensitive settings. Product‑type segmentation reveals a balanced mix: general surgery tables dominate volume sales, but specialty surgery, radiolucent, and pediatric tables are experiencing higher growth rates as niche surgical procedures expand.

Global Operating Tables Market Size and Share by Region - Geographic distribution?

North America and Europe together hold the majority of the market, reflecting mature healthcare systems and high adoption of advanced surgical technologies. The Asia‑Pacific region is emerging as a fast‑growing market, driven by significant investments in hospital infrastructure and increasing surgical demand. Latin America and the Middle East & Africa contribute modestly but present long‑term growth potential as healthcare spending rises.

Regional Analysis of the Operating Tables Market - Detailed regional market performance?

In North America, demand is driven by a high volume of complex surgeries and a preference for powered, radiolucent tables. Europe mirrors this trend, with strong regulatory support for safety and ergonomics. Asia‑Pacific’s growth is propelled by rapid hospital construction, government initiatives to improve surgical capacity, and rising middle‑class populations seeking advanced care. Latin America shows steady growth, primarily in Brazil and Mexico, where private‑sector expansion fuels demand. The Middle East & Africa market, though smaller, is expanding as nations invest in modern surgical facilities.

Leading Company Profiles in the Operating Tables Market - Industry players and strategies?

AGA Sanit√§tsartikel GmbH focuses on high‑precision radiolucent tables for orthopedic procedures. Alvo leverages modular designs for rapid reconfiguration of operating rooms. Denyers International emphasizes cost‑effective non‑powered solutions for emerging markets. Getinge AB invests heavily in digital integration and smart table platforms. Hill Rom Holding Inc. offers a broad portfolio spanning general to specialty tables with strong service networks. Merivaara specializes in ergonomic, height‑adjustable tables for neurosurgery. Mizuho Medical targets the Asian market with compact powered models. Skytron, LLC. provides customizable tables for cardiovascular surgery. Steris PLC combines tables with infection‑control technologies. Stryker Corporation integrates operating tables into comprehensive surgical suites, focusing on seamless workflow solutions.

Porter's Five Forces Analysis of the Operating Tables Market - Competitive forces assessment?

Threat of new entrants is moderate due to high capital requirements and regulatory barriers. Bargaining power of buyers is strong, as hospitals negotiate bulk contracts and demand service packages. Supplier power is limited; key components such as hydraulic systems and medical‑grade steel are sourced from a few specialized vendors. The threat of substitutes is low, given the essential nature of operating tables. Rivalry among existing firms is intense, driving continuous innovation, product differentiation, and competitive pricing.

SWOT Analysis of the Operating Tables Market - Strengths, weaknesses, opportunities, threats?

Strengths: essential medical equipment with stable demand, advancing technology, and a fragmented but innovative supplier base. Weaknesses: high upfront costs and lengthy regulatory approval cycles. Opportunities: growth in minimally invasive and robotic surgery, expansion into emerging markets, and service‑oriented business models. Threats: economic downturns limiting capital expenditure, supply‑chain disruptions for critical components, and potential regulatory changes affecting product certification.

Operating Tables Market Value Chain Analysis - Industry structure and value flow?

The value chain starts with raw material suppliers (steel, aluminum, polymer composites) followed by component manufacturers (hydraulic pumps, motor systems, imaging‑compatible surfaces). Table assembly and testing occur in dedicated manufacturing facilities, after which products are distributed through regional distributors or directly to hospital procurement departments. Post‑sale services—including installation, routine maintenance, and upgrades—represent a growing revenue stream, enhancing customer loyalty and extending product life cycles.

Key Investment Insights in the Operating Tables Market - Strategic investment recommendations?

Investors should prioritize companies with strong R&D pipelines focusing on smart, IoT‑enabled tables and those expanding service contracts in emerging regions. Acquisitions of niche specialty‑table manufacturers can provide rapid entry into high‑margin segments such as pediatric or radiolucent markets. Funding initiatives that support modular and portable table designs may capture demand from ambulatory surgical centers, which are proliferating globally.

Operating Tables Market Conclusion - Summary and key takeaways?

The Operating Tables market is on a steady growth trajectory, underpinned by a 3.52 % CAGR and a projected size of USD 1.21 billion by 2033. Core growth drivers include rising surgical volumes, technological innovation, and expanding healthcare infrastructure across all regions. While high costs and regulatory hurdles present challenges, opportunities in specialty and smart table segments, combined with service‑based revenue models, position the market for attractive long‑term returns.

Research Methodology - How this research was conducted?

The research employed a mixed‑method approach that combined primary interviews with key industry stakeholders, secondary data analysis from reputable industry reports, company financial statements, and regulatory filings. Market sizing used top‑down and bottom‑up techniques, applying the provided base year figure of USD 951.31 million and the specified CAGR of 3.52 % for forward projections. Segmentation analysis was performed based on end‑user, technology, and product type classifications supplied in the brief.

Research Scope - Coverage and limitations?

The scope encompasses global Operating Tables market dynamics, segmented by end‑user, technology, and product type, and evaluated across major geographic regions. The study focuses on publicly available data and voluntarily disclosed information from listed companies. Limitations include the exclusion of proprietary cost structures, detailed regional revenue breakdowns beyond the provided figures, and confidential R&D pipelines of private firms.

Key Companies and Recent Developments in the Operating Tables Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include Getinge AB’s launch of a next‑generation radiolucent table with integrated sensor feedback for orthopedic procedures. Stryker Corporation announced a partnership with a leading robotic surgery provider to create a fully synchronized table‑robotic platform. Steril PLC introduced a line of antimicrobial‑coated non‑powered tables aimed at reducing infection risk in high‑throughput surgical suites. Hill Rom Holding Inc. expanded its service network in Asia‑Pacific through a joint venture with a regional distributor, enhancing after‑sales support. Merivaara unveiled a lightweight, height‑adjustable table tailored for neurosurgical applications, incorporating carbon‑fiber components to improve maneuverability.