What is the Asia Pacific Floor Coating Market Overview – definition, scope, and significance?

The Asia Pacific Floor Coating Market comprises manufacturers, distributors, and end‑users of protective and decorative coatings applied to various flooring substrates such as wood, concrete, mortar and terrazzo. The market scope covers all product types—including epoxy, polyurethane, acrylics and polymethyl methacrylate—formulated as solvent‑based or water‑based, and delivered in 1K, 2K or 3K systems. Its significance stems from rapid urbanisation, growing infrastructure projects, and heightened demand for durable, hygienic surfaces across residential, commercial and industrial sectors in the region.

What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Floor Coating Market?

Drivers include strong construction activity, government incentives for green buildings, and increasing awareness of safety‑critical flooring in hospitals and warehouses. Restraints arise from fluctuating raw‑material costs and stringent environmental regulations on solvent‑based products. Challenges involve skilled‑labor shortages for proper surface preparation and intense price competition. Opportunities are presented by the shift toward water‑based, low‑VOC formulations, digital coating application technologies, and expansion into secondary cities where new retail and logistics hubs are emerging.

What are the current growth trends in the Asia Pacific Floor Coating Market?

Current trends feature a surge in epoxy and polyurethane usage for industrial floors due to their chemical resistance, while acrylics gain traction in residential projects for rapid curing and aesthetic flexibility. Sustainable formulations—especially water‑based systems—are becoming mainstream, driven by green certification requirements. Additionally, the adoption of 2K and 3K multi‑component systems is increasing to meet higher performance specifications for heavy‑traffic environments.

How has COVID‑19 impacted the Asia Pacific Floor Coating Market and what is the recovery trajectory?

The pandemic caused a temporary slowdown in construction activity and disrupted supply chains, leading to a short‑term dip in demand. However, post‑2022 recovery has been robust, propelled by pent‑up demand for residential renovations and accelerated logistics‑centre development. The market is on a clear upward trajectory, with manufacturers expanding capacity to meet renewed growth, and the shift toward health‑focused flooring solutions gaining momentum.

What does the competitive landscape of the Asia Pacific Floor Coating Market look like?

The market is moderately consolidated, with a mix of global giants and strong regional players. Key competitors such as 3M, PPG Industries, Sherwin‑Williams, Nippon Paint and Sika dominate by leveraging extensive distribution networks, broad product portfolios, and advanced R&D capabilities. Recent consolidation activity includes strategic acquisitions and joint ventures aimed at expanding product lines and strengthening presence in fast‑growing economies like India, Vietnam and the Philippines.

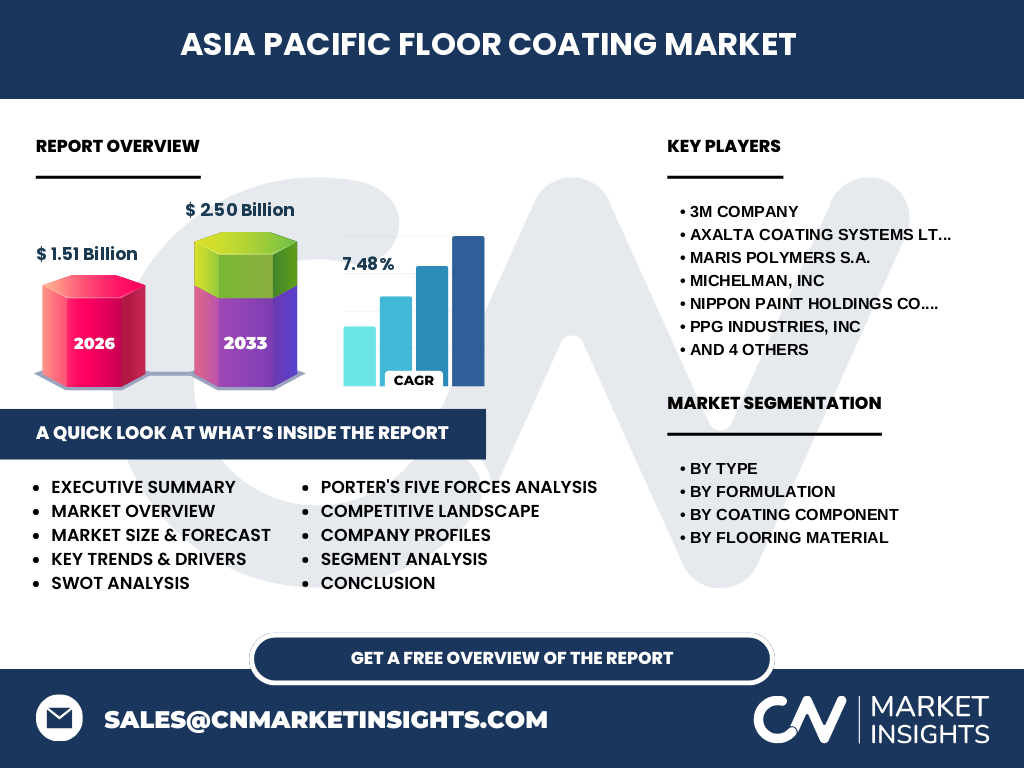

What are the high‑level insights presented in the executive summary?

The Asia Pacific Floor Coating Market is valued at USD 1.51 billion in 2026 and is projected to reach USD 2.50 billion by 2033, reflecting a CAGR of 7.48 % over the forecast horizon. Growth is driven by infrastructure expansion, demand for sustainable coatings, and technological advances in multi‑component systems. Competitive pressure is intensifying, prompting players to focus on innovation, geographic diversification and strategic partnerships to capture emerging opportunities.

What are the market forecasts for 2025‑2032?

Based on the provided CAGR of 7.48 %, the market is expected to continue expanding steadily. By 2027 the market size will approach USD 1.70 billion, progressing to USD 2.00 billion by 2030, and reaching the forecasted USD 2.50 billion by 2033. This trajectory signals strong demand across all segments, with premium high‑performance coatings and eco‑friendly formulations anticipated to outpace the overall growth rate.

How is the market sized and shared by segmentation?

Segmentation by type places epoxy as the largest contributor, followed by polyurethane, acrylics and polymethyl methacrylate. By formulation, water‑based products are gaining share due to regulatory pressure, while solvent‑based remains significant for high‑performance industrial applications. The coating component split shows 2K systems capturing the majority of industrial orders, with 1K favored in fast‑track residential projects and 3K emerging for specialty flooring. Finally, flooring material segmentation indicates concrete as the dominant substrate, with wood, mortar and terrazzo serving niche markets.

What is the geographic distribution of the market size and share?

The Asia Pacific region exhibits pronounced variation. China and India together account for a substantial portion of the market, driven by mega‑infrastructure programs and urban housing growth. Southeast Asian economies such as Vietnam, Indonesia and the Philippines contribute rapidly expanding demand, while developed markets like Japan and Australia maintain steady consumption of high‑performance coatings. Each sub‑region presents unique growth dynamics aligned with local construction cycles and regulatory environments.

What does the regional analysis reveal about market performance?

In East Asia, premium epoxy and polyurethane systems dominate industrial flooring, supported by advanced manufacturing hubs. South Asia shows accelerated adoption of water‑based acrylics in residential projects, reflecting cost sensitivity and sustainability targets. Southeast Asia records the fastest growth rate, propelled by logistics‑centre construction and retail expansion. Australasia remains a mature market with a focus on high‑durability, low‑VOC solutions for commercial spaces.

Which leading companies are operating in the Asia Pacific Floor Coating Market and what are their strategies?

Major players include 3M, Axalta, Maris Polymers, Michelman, Nippon Paint, PPG Industries, Rust‑Oleum, Sika, Lubrizol and Sherwin‑Williams. Strategies revolve around expanding product portfolios with low‑VOC water‑based lines, investing in digital coating application technologies, forming local partnerships to enhance distribution, and pursuing R&D collaborations to develop high‑performance 2K/3K systems. Several firms are also targeting niche segments such as anti‑microbial flooring for healthcare facilities.

How does Porter’s Five Forces affect the Asia Pacific Floor Coating Market?

Threat of new entrants is moderate due to high capital requirements and regulatory barriers. Bargaining power of suppliers is moderate; raw‑material price volatility impacts margins but diversified sourcing mitigates risk. Bargaining power of buyers is high, as large contractors and OEMs demand competitive pricing and consistent quality. Threat of substitutes is low because alternative flooring solutions lack the protective characteristics of specialized coatings. Industry rivalry is intense, driving continuous innovation and price competition.

What are the SWOT insights for the overall market?

Strengths: Strong demand from construction boom, diverse product range, and advancing technology. Weaknesses: Dependence on volatile raw‑material costs and regulatory constraints on solvent‑based products. Opportunities: Growth of green building standards, expansion into secondary urban centers, and development of smart, self‑healing coatings. Threats: Economic slowdowns, increased competition from low‑cost manufacturers, and tightening environmental legislation.

What does the value chain of the Asia Pacific Floor Coating Market look like?

The value chain begins with raw‑material suppliers (resins, solvents, pigments), proceeds to formulation and compounding by manufacturers, followed by packaging and logistics. Distribution channels include direct sales to large contractors, distributors serving smaller builders, and e‑commerce platforms for DIY segments. End‑users apply the coatings, often supported by service providers offering surface preparation, application training and after‑sales technical support, completing the cycle.

What key investment insights can be drawn for the market?

Investors should focus on companies with robust R&D pipelines for water‑based and high‑performance multi‑component systems, as these segments promise higher margins. Strategic acquisitions of regional distributors can accelerate market entry, especially in fast‑growing Southeast Asian economies. Monitoring regulatory developments around VOC limits will highlight firms best positioned to benefit from compliance‑driven demand. Finally, partnerships with construction firms for “turn‑key” flooring solutions can secure long‑term revenue streams.

What conclusions can be drawn from the market analysis?

The Asia Pacific Floor Coating Market is on a strong growth path, underpinned by infrastructural investment and a shift toward sustainable, high‑performance coatings. While challenges such as raw‑material volatility and regulatory pressures persist, the overall outlook remains positive, with ample room for innovation, geographic expansion and strategic consolidation. Companies that adapt quickly to eco‑friendly trends and offer integrated service solutions are likely to lead the market.

How was the research methodology designed?

The study combined primary interviews with industry experts, senior executives and key distributors, alongside secondary data from company reports, trade publications and government statistics. Market sizing employed a top‑down approach using the provided 2026 base value and CAGR to project forward estimates. Segmentation analysis was validated through product‑level sales data and expert insights, while competitive assessment drew on revenue disclosures, patent filings and recent M&A activity.

What is the scope of the research and its limitations?

The scope covers the floor coating industry across the Asia Pacific region, addressing all major product types, formulations, component systems and flooring substrates. It includes quantitative forecasts to 2033 and qualitative assessments of trends, competitive dynamics and strategic opportunities. Limitations stem from reliance on publicly available financials and the absence of granular country‑level sales figures, which may affect precise market‑share calculations for smaller economies.

Which key companies have made recent developments in the Asia Pacific Floor Coating Market?

Recent developments include 3M launching a new low‑VOC water‑based epoxy line for industrial flooring, Axalta expanding its distribution network in India, and Nippon Paint announcing a joint venture with a local ceramic tile manufacturer to offer integrated flooring solutions. PPG Industries introduced a digital coating application platform in Australia, while Sherwin‑Williams acquired a Southeast Asian specialty coating firm to broaden its portfolio of high‑performance polyurethane systems.