What is the Europe Floor Coating Market Overview – Definition, scope, and significance?

The Europe Floor Coating Market encompasses the production, distribution, and application of protective and decorative coating systems for various flooring substrates across European countries. It includes a range of chemistries—epoxy, polyurethane, acrylics, and polymethyl methacrylate—available in solvent‑based or water‑based formulations and in 1‑component (1K), 2‑component (2K), and 3‑component (3K) systems. The market serves sectors such as residential, commercial, industrial, and infrastructure, where durable, chemical‑resistant, and aesthetically appealing flooring is critical. Its significance lies in supporting construction growth, renovation activities, and sustainability goals through low‑VOC and high‑performance solutions.

What are the Europe Floor Coating Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include robust construction and refurbishment pipelines, rising demand for high‑performance industrial floors, and stringent European regulations that favor low‑VOC, water‑based products. Opportunities arise from green building certifications, digitalization of application processes, and the expansion of prefabricated flooring modules. Restraints involve fluctuating raw‑material costs, especially petroleum‑derived solvents, and skilled‑labour shortages for complex 2K/3K systems. Challenges stem from the need to balance performance with environmental compliance and from intense price competition among established global manufacturers.

What are the Europe Floor Coating Market Growth Trends – Current and emerging trends shaping the market?

Current trends show a decisive shift toward water‑based and high‑solids formulations, driven by EU VOC directives. Epoxy systems remain dominant for industrial floors, while polyurethane and acrylics gain traction in residential and retail spaces due to flexibility and rapid cure times. Emerging trends include the adoption of nanotechnology‑enhanced coatings for superior abrasion resistance, the integration of smart sensor‑embedded layers for real‑time condition monitoring, and the rise of modular, click‑fit flooring systems that reduce installation time.

How did COVID‑19 impact the Europe Floor Coating Market – Pandemic effects and recovery trajectory?

The pandemic caused a temporary slowdown in new construction projects and supply‑chain disruptions, leading to modest year‑over‑year volume declines in 2020. However, the rapid rebound in renovation activity, driven by remote‑working trends and government stimulus for infrastructure, accelerated demand for durable floor coatings. By 2022, the market regained momentum, and the subsequent years have shown a strong recovery trajectory, supported by pent‑up demand and an increased focus on indoor environmental quality.

What does the Europe Floor Coating Market Competitive Landscape look like – Major competitors and market consolidation?

The competitive landscape is fragmented, featuring a mix of multinational corporations and regional specialists. Leading players such as 3M Company, Axalta Coating Systems Ltd, PPG Industries, Inc., Sherwin‑Williams, and Sika AG dominate through extensive product portfolios and distribution networks. Recent consolidation activity includes strategic acquisitions targeting niche water‑based technologies and joint ventures aimed at expanding market reach in Central and Eastern Europe. Competitive differentiation is based on innovation speed, sustainability credentials, and service‑oriented solutions.

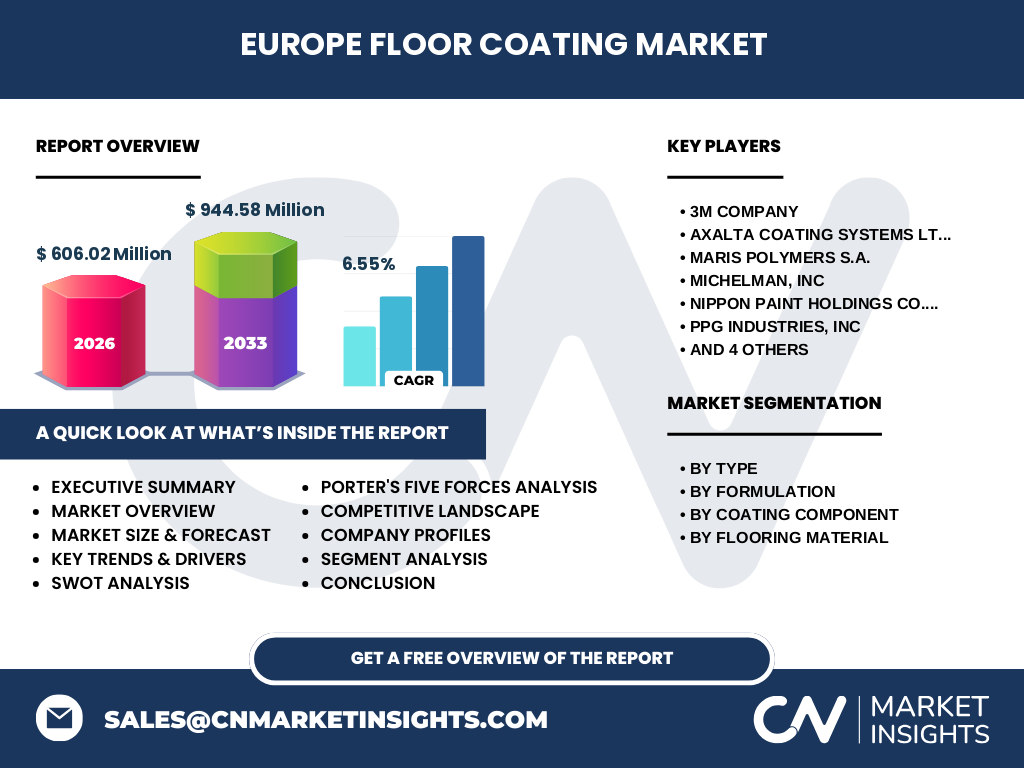

What are the key findings in the Executive Summary – High‑level overview of the Europe Floor Coating Market?

The Europe Floor Coating Market is projected to grow from a 2026 size of €606.02 million to €944.58 million by 2033, reflecting a compound annual growth rate of 6.55 %. Growth is propelled by strong construction pipelines, tightening environmental regulations, and an expanding portfolio of high‑performance, low‑VOC coatings. Epoxy remains the largest type segment, while water‑based formulations capture the fastest growth. Major players are investing in R&D and strategic partnerships to capture emerging opportunities in green and smart floor‑coating solutions.

What is the Europe Floor Coating Market Forecast – Projections for the 2025‑2032 period?

Based on current trends, the market is expected to maintain a steady CAGR of approximately 6.5 % through 2032. Revenue is anticipated to exceed €900 million by the end of the forecast horizon, with water‑based and high‑solids products contributing the majority of incremental growth. Demand from industrial sectors such as logistics, automotive manufacturing, and renewable‑energy facilities will drive the 2K and 3K system segments, while residential and commercial renovations will fuel the 1K water‑based segment.

What is the Europe Floor Coating Market Size and Share by Segmentation?

By type, the market is divided into epoxy, polyurethane, acrylics, and polymethyl methacrylate. Epoxy commands the largest share due to its superior chemical resistance, followed by polyurethane for its flexibility and quick cure. Acrylics are gaining ground in decorative applications, while polymethyl methacrylate serves niche high‑clarity needs. By formulation, solvent‑based and water‑based coatings each hold significant portions, with water‑based accelerating faster. Component segmentation shows 1K systems dominant in low‑maintenance projects, whereas 2K and 3K systems are preferred for heavy‑duty industrial floors. Flooring material segmentation includes wood, concrete, mortar, and terrazzo, with concrete representing the primary substrate across most segments.

What is the Global Europe Floor Coating Market Size and Share by Region – Geographic distribution?

The European region accounts for a substantial portion of the global floor‑coating landscape, anchored by mature markets in Germany, France, the United Kingdom, and the Nordics. While specific regional share percentages are not disclosed, Europe’s contribution is highlighted by its leadership in green‑coating adoption and advanced manufacturing capabilities, positioning it as a key growth engine within the worldwide market.

What does the Regional Analysis of the Europe Floor Coating Market reveal – Detailed regional market performance?

Western Europe leads in market volume, driven by high construction activity, stringent environmental standards, and strong purchasing power. Germany and the United Kingdom exhibit the highest uptake of epoxy and water‑based systems for industrial and commercial projects. Southern Europe, particularly Italy and Spain, shows robust demand for decorative acrylics and terrazzo coatings in renovation works. Central and Eastern European economies are emerging markets, with rapid adoption of cost‑effective 1K water‑based solutions as infrastructure investments increase.

Who are the leading company profiles in the Europe Floor Coating Market – Industry players and strategies?

Key companies include 3M Company, renowned for its advanced epoxy technologies; Axalta Coating Systems Ltd, focusing on high‑performance polyurethane solutions; Maris Polymers S.A., a specialist in water‑based acrylics; Michelman, Inc., offering innovative 2K systems; Nippon Paint Holdings Co., Ltd., strong in decorative finishes; PPG Industries, Inc., a global leader with a broad portfolio; Rust‑Oleum, known for DIY and commercial coatings; Sika AG, a major player in construction chemicals; The Lubrizol Corporation, focusing on high‑solids formulations; and The Sherwin‑Williams Company, leveraging extensive distribution channels. Strategies revolve around product innovation, sustainability certifications, and geographic expansion through acquisitions and partnerships.

What does the Porter’s Five Forces analysis indicate for the Europe Floor Coating Market?

Threat of new entrants is moderate due to high R&D costs and regulatory barriers. Bargaining power of suppliers is limited, as raw‑material sources are diversified, though specialty chemicals can command premium pricing. Bargaining power of buyers is high, especially among large industrial clients that demand customized solutions and competitive pricing. Threat of substitutes remains low; alternative floor protection methods (e.g., tiles) do not replicate the performance of advanced coatings. Competitive rivalry is intense, driven by product innovation, brand reputation, and service differentiation among the leading multinational firms.

What are the SWOT insights for the Europe Floor Coating Market?

Strengths: Mature supply chains, strong technical expertise, and alignment with EU sustainability regulations.

Weaknesses: Dependence on volatile petrochemical feedstocks and fragmented pricing pressure.

Opportunities: Growth of green building certifications, smart‑floor technologies, and expanding demand in emerging European economies.

Threats: Regulatory shifts that could tighten VOC limits further, and potential trade barriers affecting raw‑material imports.

How is the Europe Floor Coating Market value chain structured?

The value chain begins with raw‑material suppliers (resins, solvents, pigments), progresses to formulation manufacturers that produce 1K, 2K, and 3K coating systems. These are followed by distributors and specialty retailers who supply end‑users such as construction firms, contractors, and facility managers. Application services, including surface preparation and coating installation, add value and create post‑sale revenue streams. After‑sales support and recycling programs close the loop, particularly for water‑based and low‑VOC products.

What key investment insights can be drawn for the Europe Floor Coating Market?

Investors should target companies with strong pipelines in water‑based and high‑solids technologies, as these segments are aligned with regulatory trends and command premium pricing. Acquisitions of niche innovators in nanocoatings or smart‑floor integration offer high upside. Geographic expansion into Central and Eastern Europe presents growth at lower entry costs. Additionally, firms that demonstrate robust sustainability metrics are better positioned for long‑term contracts with green‑building projects.

What is the concluding overview of the Europe Floor Coating Market?

The Europe Floor Coating Market is on a clear upward trajectory, underpinned by a 6.55 % CAGR and a projected 2027‑2033 value of €944.58 million. Demand is being reshaped by environmental mandates, digital installation methods, and the need for durable, low‑maintenance flooring across industrial and commercial spaces. Market leaders that invest in sustainable formulations, advanced application technologies, and strategic regional expansion are poised to capture the majority of future growth.

What research methodology was employed for this market study?

The study combines primary interviews with industry executives, distributors, and end‑users, alongside secondary data from company reports, trade publications, and EU regulatory sources. Quantitative analysis used time‑series modelling to project the 2026 base size of €606.02 million to the 2033 forecast of €944.58 million, applying the disclosed CAGR of 6.55 %. Qualitative insights were validated through cross‑checking with multiple expert opinions.

What is the defined research scope – Coverage and limitations?

The scope covers all major European countries, encompassing all floor‑coating types, formulations, component systems, and substrate applications listed. It excludes niche decorative paints not intended for floor protection and omits non‑European regions. Financial figures are limited to the provided market size, forecast, and growth rate; detailed market‑share percentages are not disclosed.

Which key companies and recent developments are notable in the Europe Floor Coating Market?

Key players such as 3M, Axalta, PPG, Sherwin‑Williams, and Sika have announced new water‑based epoxy lines that meet stricter VOC limits. Nippon Paint launched a high‑solids polyurethane range targeting the logistics sector. Rust‑Oleum introduced a DIY‑friendly 1K acrylic system with rapid cure. Michelman unveiled a 3K nano‑reinforced coating aimed at chemical‑resistant industrial floors. These developments highlight a market focus on sustainability, performance, and faster installation cycles.