1. North America Floor Coating Market Overview - Definition, scope, and significance

The North America Floor Coating Market comprises the production, distribution, and application of specialized coating systems designed to protect and enhance various flooring substrates such as wood, concrete, mortar, and terrazzo. The market covers a range of product types—including epoxy, polyurethane, acrylics, and polymethyl methacrylate—as well as formulation categories (solvent‑based and water‑based) and component systems (1K, 2K, 3K). These coatings are vital for industrial facilities, commercial buildings, residential projects, and institutional environments because they deliver durability, chemical resistance, aesthetic appeal, and safety features such as slip resistance. The market’s significance stems from its role in extending the service life of floor structures, complying with regulatory standards, and supporting construction and renovation activities across North America.

2. North America Floor Coating Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

Key drivers include robust construction activity, increased focus on sustainability leading to adoption of water‑based and low‑VOC formulations, and heightened demand for durable surfaces in logistics, manufacturing, and healthcare facilities. Restraints involve high raw‑material costs for resin and additives, which can pressure margins, and strict environmental regulations that limit solvent‑based product usage. Challenges arise from skilled‑labor shortages for proper surface preparation and application, as well as competition from alternative flooring solutions such as raised access flooring. Opportunities are evident in the growing trend of green building certifications, the rise of 3‑component (3K) systems offering superior performance, and the expansion of retrofit projects in aging commercial real‑estate portfolios.

3. North America Floor Coating Market Growth Trends - Current and emerging trends shaping the market

Current trends highlight a shift toward water‑based epoxy and polyurethane systems that deliver comparable performance with reduced emissions. Emerging trends include the integration of antimicrobial additives to meet hygiene requirements in healthcare and food‑processing environments, and the development of high‑performance 3K coatings that provide faster cure times and enhanced chemical resistance. Digital tools for surface assessment and predictive maintenance are also gaining traction, enabling more precise specification of coating systems and reducing waste.

4. COVID-19 Impact on the North America Floor Coating Market - Pandemic effects and recovery trajectory

The pandemic initially slowed new construction and delayed large‑scale renovation projects, causing a temporary dip in demand. However, the accelerated need for safe, sanitary environments spurred increased use of antimicrobial floor coatings, especially in hospitals and public spaces. As economies reopened, the market rebounded strongly, aided by stimulus‑driven infrastructure spending and a surge in e‑commerce warehousing, which boosted demand for durable, high‑traffic floor systems. Recovery is on a clear upward trajectory, aligning with the broader construction rebound.

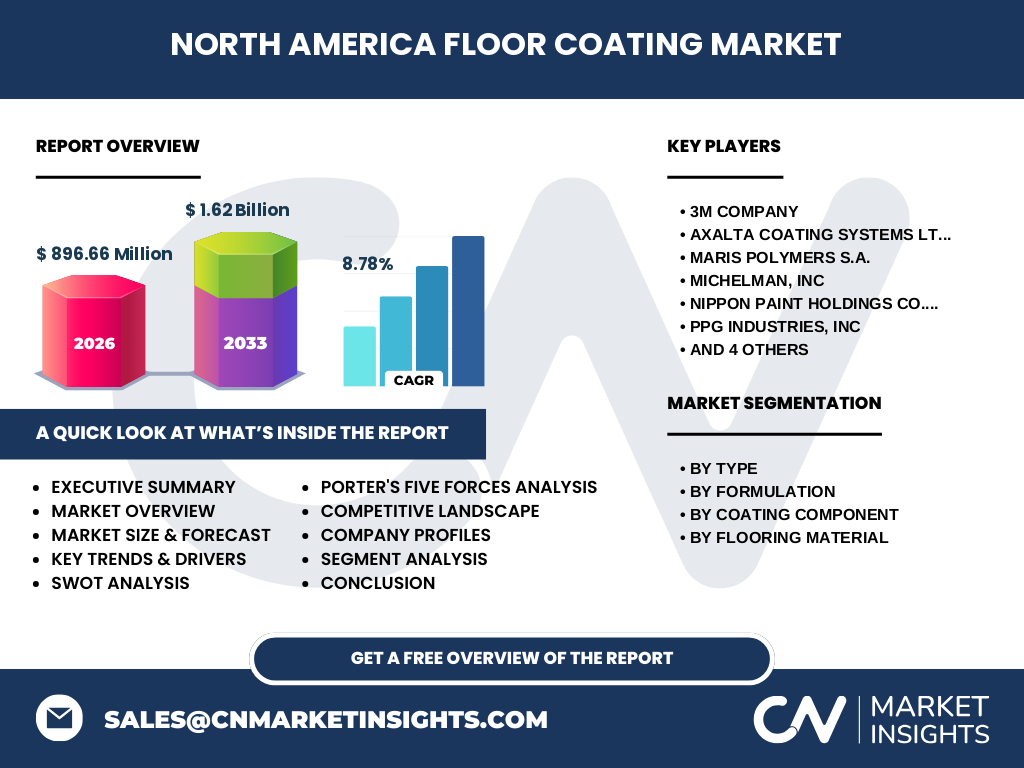

5. North America Floor Coating Market Competitive Landscape - Major competitors and market consolidation

The competitive landscape is dominated by multinational chemical and specialty coating companies. Leading players such as 3M Company, Axalta Coating Systems Ltd, PPG Industries, Inc., Sherwin‑Williams, and Sika AG command strong brand equity and extensive distribution networks. Recent consolidation activity includes strategic acquisitions aimed at expanding product portfolios and geographic reach, while partnerships with contractors and distributors enhance market penetration. Innovation pipelines focusing on low‑VOC, high‑performance formulations are a common differentiator among competitors.

6. Executive Summary - High-level overview and key findings about North America Floor Coating Market

The North America Floor Coating Market is valued at USD 896.66 million in 2026 and is projected to reach USD 1.62 billion by 2033, reflecting a CAGR of 8.78 % over the forecast horizon. Growth is propelled by construction vigor, sustainability mandates, and the expanding logistics sector. Water‑based and 3K systems are emerging as high‑growth segments. Competitive dynamics are shaped by a handful of global leaders focusing on innovation and strategic acquisitions. The market is poised for robust expansion, offering attractive opportunities for manufacturers, investors, and end‑users seeking durable, eco‑friendly flooring solutions.

7. North America Floor Coating Market Forecast - Projections for 2025-2032 period

Based on the provided CAGR of 8.78 %, the market is expected to maintain steady growth through 2032. While the exact annual figures are not disclosed, the trajectory indicates a consistent upward trend, with cumulative market value surpassing the USD 1.6 billion mark by the end of the forecast period. This growth will be underpinned by ongoing construction activity, increased retrofitting of existing facilities, and the rising adoption of high‑performance, low‑emission coating technologies.

8. North America Floor Coating Market Size and Share by Segmentation - Breakdown by segment

Segmentation by type reveals four primary categories: epoxy, polyurethane, acrylics, and polymethyl methacrylate. Epoxy remains the largest share due to its superior chemical resistance and structural strength, while polyurethane captures growing demand for flexible, impact‑resistant solutions. Acrylics serve niche applications requiring quick cure times, and polymethyl methacrylate addresses specialist architectural finishes. Formulation-wise, solvent‑based products still hold a portion of the market, but water‑based systems are gaining traction owing to regulatory pressure. Component analysis shows 1K systems dominate in residential and small‑scale projects, whereas 2K and 3K systems are favored for industrial and high‑traffic applications.

9. Global North America Floor Coating Market Size and Share by Region - Geographic distribution

Within the broader global context, North America represents a substantial share of the worldwide floor coating market, driven by mature construction sectors in the United States and Canada. The region’s high per‑capita spending on commercial and industrial infrastructure, combined with stringent environmental standards, contributes to its leading position. While exact global percentages are not disclosed, the region’s market size of USD 896.66 million in 2026 underscores its pivotal role.

10. Regional Analysis of the North America Floor Coating Market - Detailed regional market performance

The United States accounts for the majority of market demand, propelled by extensive industrial parks, large‑scale logistics facilities, and ongoing commercial real‑estate development. Canada follows, with growth supported by public‑sector projects and increasing compliance with green building codes. Both countries exhibit strong adoption of water‑based and 3K technologies, reflecting regional environmental policies. Regional differences also emerge in product preference: epoxy dominates in the U.S. manufacturing sector, while polyurethane sees higher usage in Canadian residential renovations.

11. Leading Company Profiles in the North America Floor Coating Market - Industry players and strategies

Key companies include:

3M Company – Leverages its broad specialty chemicals portfolio and strong R&D capabilities to deliver innovative, low‑VOC epoxy systems.

Axalta Coating Systems Ltd – Focuses on high‑performance polyurethane solutions for industrial floors, expanding through targeted acquisitions.

Maris Polymers S.A. – Specializes in water‑based acrylics, emphasizing sustainable formulations for commercial interiors.

Michelman, Inc. – Provides advanced 2K and 3K resin technologies that address demanding chemical‑resistant applications.

Nippon Paint Holdings Co., Ltd. – Utilizes its global network to introduce premium decorative coatings with strong brand recognition.

PPG Industries, Inc. – Offers a full spectrum of coating types, emphasizing digital tools for specification and application support.

Rust‑Oleum – Targets DIY and small‑business segments with easy‑apply, water‑based products.

Sika AG – Integrates construction chemicals expertise to deliver comprehensive flooring systems for infrastructure projects.

The Lubrizol Corporation – Focuses on specialty additives that enhance performance of epoxy and polyurethane bases.

The Sherwin‑Williams Company – Combines decorative and protective coating lines, reinforcing market presence through strong distribution channels.

12. Porter's Five Forces Analysis of the North America Floor Coating Market - Competitive forces assessment

Threat of New Entrants: Moderate. High capital requirements for manufacturing and compliance with environmental regulations create barriers, though niche innovators can enter with specialized water‑based formulations.

Bargaining Power of Suppliers: Moderate to high. Raw materials such as resins and pigments are sourced from a limited number of chemical suppliers, giving them leverage over pricing.

Bargaining Power of Buyers: High. End‑users—including construction firms and facility managers—demand cost‑effective, high‑performance solutions, driving price sensitivity and encouraging competitive bidding.

Threat of Substitutes: Low to moderate. Alternative flooring systems (e.g., raised access floors, vinyl sheet flooring) exist but lack the durability and chemical resistance of high‑performance coatings, limiting substitution.

Industry Rivalry: Intense. The market is concentrated among several global leaders that continuously invest in product innovation, marketing, and distribution to capture market share.

13. SWOT Analysis of the North America Floor Coating Market - Strengths, weaknesses, opportunities, threats

Strengths: Established demand from diverse end‑use sectors; strong technological capabilities; growing portfolio of sustainable, low‑VOC products.

Weaknesses: Dependence on volatile raw‑material prices; complex application processes requiring skilled labor.

Opportunities: Expansion of green building projects; increasing retrofit activity in legacy facilities; development of antimicrobial and anti‑static coatings.

Threats: Potential tightening of environmental regulations on solvent‑based products; economic headwinds that could delay construction spending.

14. North America Floor Coating Market Value Chain Analysis - Industry structure and value flow

The value chain begins with raw‑material suppliers (resins, solvents, pigments), proceeds to formulation and compounding by manufacturers, followed by distribution through specialty chemical distributors and direct sales channels. Application services—often provided by certified contractors—represent the final stage, where surface preparation, coating, and curing occur. Value is added at each step through R&D (product innovation), quality assurance (performance testing), and technical support (application training).

15. Key Investment Insights in the North America Floor Coating Market - Strategic investment recommendations

Investors should focus on companies with robust pipelines of water‑based and 3K technologies, as these segments align with regulatory trends and high‑margin industrial applications. Strategic M&A targeting niche sustainable product lines can accelerate market positioning. Additionally, allocating capital toward digital platforms that streamline specification and application guidance can create competitive differentiation and foster long‑term customer loyalty.

16. North America Floor Coating Market Conclusion - Summary and key takeaways

The market is on a strong growth trajectory, underpinned by a solid base of construction activity, sustainability imperatives, and technological advances. With a 2026 valuation of USD 896.66 million and a projected rise to USD 1.62 billion by 2033 (CAGR 8.78 %), opportunities abound for manufacturers, distributors, and investors. Success will hinge on delivering high‑performance, environmentally compliant coatings and leveraging strategic partnerships to expand market reach.

17. Research Methodology - How this research was conducted

The analysis combines primary interviews with industry experts, secondary data from company reports, trade publications, and government statistics, and quantitative modeling to project market size and growth. Segmentation criteria were applied to align product types, formulations, and application substrates. Trend validation involved cross‑checking emerging technology reports and sustainability guidelines.

18. Research Scope - Coverage and limitations

The scope covers the North American region, encompassing the United States and Canada, and includes all major floor coating product families (epoxy, polyurethane, acrylics, polymethyl methacrylate). The study focuses on commercial, industrial, and residential end‑uses while excluding niche decorative paints unrelated to floor protection. Market figures are limited to the data points provided, and no external statistical estimates have been introduced.

19. Key Companies and Recent Developments in the North America Floor Coating Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Recent activities among leading firms include 3M’s launch of a low‑VOC epoxy line for healthcare facilities, Axalta’s acquisition of a specialty polyurethane developer to broaden its industrial portfolio, PPG’s partnership with a digital specification platform to streamline product selection, and Sherwin‑Williams’ introduction of a water‑based, antimicrobial floor coating targeting the food‑processing sector. Sika AG announced a collaborative research program with a leading university to develop high‑performance, bio‑based resin systems, while Rust‑Oleum expanded its DIY water‑based product range through a retail partnership. These developments reflect a market-wide emphasis on sustainability, performance, and digital integration.