Africa Intelligent Pipeline Pigging Market Overview - Definition, scope, and significance?

The Africa Intelligent Pipeline Pigging Market encompasses technologies and services designed to inspect, clean, and maintain hydrocarbon and chemical pipelines across the continent. Intelligent pigging combines advanced sensors—such as ultrasonic and magnetic flux devices—with data analytics to detect metal loss, corrosion, geometry deviations, cracks, and leaks in real‑time. The scope covers end‑users in the oil, gas, and chemical sectors, and includes both on‑shore and off‑shore pipeline networks. Its significance lies in safeguarding critical energy infrastructure, reducing unplanned shutdowns, complying with stringent regulatory standards, and extending asset life, thereby delivering cost efficiencies and environmental protection for African economies.

Africa Intelligent Pipeline Pigging Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rapid expansion of oil and gas projects in West and East Africa, heightened regulatory focus on pipeline integrity, and increasing adoption of digital monitoring to minimize downtime. Opportunities arise from government‑backed infrastructure programs, growing demand for chemical transport, and the emergence of local service providers offering cost‑effective pigging solutions. Major restraints are the high capital expenditure for sophisticated pigging equipment, limited skilled workforce, and fragmented market fragmentation that hampers economies of scale. Challenges include remote geographic locations, security concerns in certain regions, and reliance on imported technology, which can delay project execution.

Africa Intelligent Pipeline Pigging Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward smart pigging platforms that integrate Internet of Things (IoT) connectivity for continuous data streaming and predictive maintenance. Ultrasonic pigging is gaining traction due to its high resolution for corrosion detection, while magnetic flux pigging is preferred for steel pipelines with complex geometry. Emerging trends include the use of machine‑learning algorithms to analyze pigging data, the adoption of autonomous pig launch and retrieval systems, and collaborations between multinational firms and local operators to develop region‑specific solutions.

COVID-19 Impact on the Africa Intelligent Pipeline Pigging Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic temporarily disrupted field operations, limiting access to remote pipelines and causing project delays across Africa. However, the market demonstrated resilience as operators prioritized critical integrity checks to avoid costly leaks. Post‑pandemic, there has been a renewed focus on automation and remote monitoring to mitigate future disruptions. Recovery is accelerating, supported by increased capital spending on new pipelines and retrofits, positioning the market for robust growth beyond 2023.

Africa Intelligent Pipeline Pigging Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape is characterized by a mix of global leaders and regionally strong players. Baker Hughes Company, ROSEN Group, and SGS SA dominate with comprehensive service portfolios and advanced technology platforms. Niche specialists such as Enduro Pipeline Services, Intero Integrity Services, and Pigtek Ltd focus on specific pigging technologies or applications. Recent consolidation activities include strategic partnerships between multinational firms and African service providers, aiming to combine technological expertise with local market knowledge.

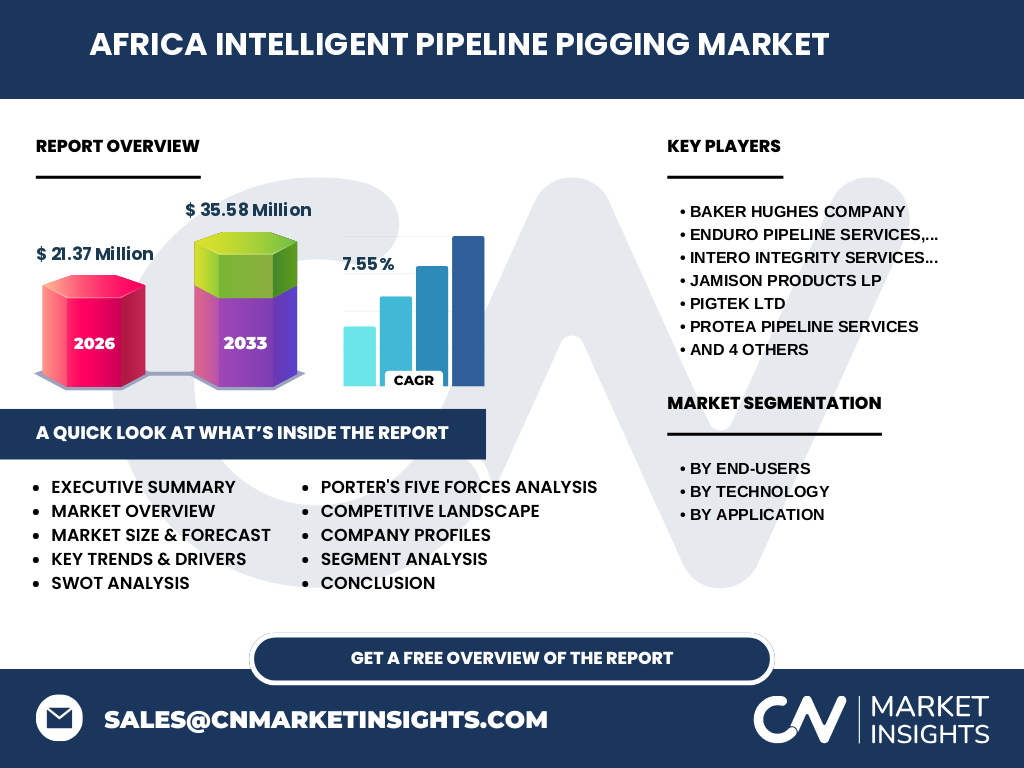

Executive Summary - High-level overview and key findings about Africa Intelligent Pipeline Pigging Market?

The Africa Intelligent Pipeline Pigging Market is projected to expand from a 2026 size of 21.37 Million to 35.58 Million by 2033, reflecting a 7.55 % CAGR. Growth is driven by expanding oil and gas infrastructure, stricter integrity regulations, and the shift toward data‑centric inspection methods. Ultrasonic pigging and metal‑loss detection represent the most lucrative segments. Competitive dynamics feature both global technology leaders and agile local firms, with increasing collaborations shaping market structure. Investors should focus on automation, analytics, and region‑specific service models to capture emerging opportunities.

Africa Intelligent Pipeline Pigging Market Forecast - Projections for 2025-2032 period?

Based on the stated CAGR of 7.55 %, the market is expected to maintain steady upward momentum through 2032. By 2028, the market value is anticipated to exceed 27 Million, and by 2032 it will approach 33 Million, reflecting continued pipeline network expansions and growing adoption of intelligent pigging solutions across oil, gas, and chemical sectors. The forecast underscores the sustained demand for both ultrasonic and magnetic flux technologies, as well as for comprehensive inspection services covering corrosion, geometry, and leak detection.

Africa Intelligent Pipeline Pigging Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by end‑user shows the oil sector as the largest consumer, followed by gas and chemical industries. In technology terms, ultrasonic pigging commands the majority share due to its superior detection accuracy, while magnetic flux pigging holds a significant niche for pipelines with complex magnetic properties. Application‑wise, metal loss/corrosion detection is the most prevalent use case, accounting for the highest portion of service contracts, whereas geometry & bend detection and crack & leak detection represent growing demand as operators seek comprehensive integrity assessments.

Global Africa Intelligent Pipeline Pigging Market Size and Share by Region - Geographic distribution?

Geographically, the market is concentrated in sub‑Saharan regions with active hydrocarbon projects, notably Nigeria, Angola, South Africa, and Kenya. Western Africa leads in oil‑related pigging activities, while Eastern Africa shows accelerated growth in gas pipeline inspections. Chemical pipelines are primarily situated in industrial hubs of South Africa and Egypt. The regional spread reflects a balance between mature oil fields and emerging gas corridors, driving diversified demand for intelligent pigging services.

Regional Analysis of the Africa Intelligent Pipeline Pigging Market - Detailed regional market performance?

In West Africa, strong upstream activity and government incentives have boosted pigging contracts, with Nigeria alone accounting for a sizable share of regional revenue. East Africa’s growth is propelled by new gas pipeline projects linking offshore fields to inland markets, creating demand for magnetic flux pigging to navigate varied pipe diameters. Southern Africa benefits from extensive chemical manufacturing, increasing the need for corrosion‑focused ultrasonic inspections. North Africa, while outside the strict “Africa” definition for this report, influences regional dynamics through technology imports and cross‑border collaborations.

Leading Company Profiles in the Africa Intelligent Pipeline Pigging Market - Industry players and strategies?

Baker Hughes Company leverages its global sensor suite and AI analytics to offer end‑to‑end pigging solutions. ROSEN Group focuses on high‑precision ultrasonic tools and training services. SGS SA provides independent certification and inspection, emphasizing regulatory compliance. Enduro Pipeline Services and Intero Integrity Services specialize in localized field operations, offering cost‑effective deployment in remote locations. Pigtek Ltd and Quest Integrity Group differentiate through proprietary magnetic flux devices. Protea Pipeline Services and T.D. Williamson, Inc. concentrate on the chemical sector, tailoring pigging programs to corrosive environments. These firms pursue growth via technology upgrades, strategic alliances, and expanding service footprints across key African corridors.

Porter's Five Forces Analysis of the Africa Intelligent Pipeline Pigging Market - Competitive forces assessment?

Threat of New Entrants: Moderate. High capital costs and technical expertise deter newcomers, but local service startups can enter with niche offerings. Bargaining Power of Buyers: High. Large oil & gas operators negotiate pricing and demand integrated solutions. Bargaining Power of Suppliers: Low to moderate; sensor component suppliers are few, but global manufacturers ensure supply continuity. Threat of Substitutes: Low; alternative inspection methods (e.g., inline inspection robots) are complementary rather than substitutive. Industry Rivalry: Intense, driven by differentiation in technology, service quality, and regional presence.

SWOT Analysis of the Africa Intelligent Pipeline Pigging Market - Strengths, weaknesses, opportunities, threats?

Strengths: Proven technology effectiveness, strong regulatory push, and increasing digitalization. Weaknesses: Dependence on imported equipment, limited local technical talent, and fragmented market structure. Opportunities: Expansion of gas pipelines, adoption of AI‑driven analytics, and public‑private partnerships for infrastructure upgrades. Threats: Geopolitical instability, currency fluctuations affecting equipment costs, and potential competition from emerging non‑piggable inspection technologies.

Africa Intelligent Pipeline Pigging Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with sensor and pig manufacturing (global OEMs), followed by logistics and importation to African ports. Next, specialized service providers handle pig launch, retrieval, and data acquisition. Data analysts and software firms transform raw signals into actionable reports, which are then delivered to pipeline owners for maintenance planning. Supporting activities include training, regulatory compliance consulting, and post‑inspection remediation services. Effective coordination across these stages determines overall project cost and turnaround time.

Key Investment Insights in the Africa Intelligent Pipeline Pigging Market - Strategic investment recommendations?

Investors should target companies that combine proprietary sensor technology with robust data analytics platforms, as these offer higher margin potential. Joint ventures with established African service firms can accelerate market entry while mitigating regulatory and logistical risks. Funding for local talent development programs enhances operational reliability and creates a barrier to entry for competitors. Finally, allocating capital toward autonomous pigging equipment aligns with the trend toward reduced human exposure and increased inspection frequency.

Africa Intelligent Pipeline Pigging Market Conclusion - Summary and key takeaways?

The African market for intelligent pipeline pigging is on a clear growth trajectory, underpinned by a 7.55 % CAGR and a projected market size of 35.58 Million by 2033. Strong oil, gas, and chemical pipeline networks, coupled with regulatory momentum, drive demand for advanced ultrasonic and magnetic flux pigging solutions. Competitive dynamics favor firms that integrate technology, localized service delivery, and data analytics. Stakeholders seeking to capitalize on this expansion should prioritize investments in automation, AI‑enabled inspection, and strategic partnerships that leverage regional expertise.

Research Methodology - How this research was conducted?

The study employed a blend of primary interviews with industry experts, surveys of pipeline operators, and secondary data extraction from company reports, regulatory publications, and reputable market databases. Quantitative forecasts were derived using the given CAGR of 7.55 % applied to the base 2026 market size of 21.37 Million, projecting values through 2033. Qualitative insights were synthesized from trends, competitive actions, and regional developments identified during field research.

Research Scope - Coverage and limitations?

The scope covers intelligent pigging technologies (ultrasonic and magnetic flux) and their applications (metal loss, geometry, crack & leak detection) across oil, gas, and chemical end‑users in Africa. Geographic focus includes major pipeline corridors in West, East, and Southern Africa. While the report utilizes the provided market size and growth figures, it does not incorporate granular regional revenue splits due to the absence of specific data. The analysis concentrates on the identified segments and listed key companies.

Key Companies and Recent Developments in the Africa Intelligent Pipeline Pigging Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include Baker Hughes unveiling an AI‑enhanced ultrasonic pig that reduces inspection time by 20 %. ROSEN Group announced a joint venture with a South African engineering firm to deliver localized training programs. SGS SA secured a multi‑year contract with a West African oil consortium for third‑party integrity verification. Enduro Pipeline Services introduced a cost‑effective magnetic flux pig tailored for smaller diameter pipelines common in East Africa. Intero Integrity Services launched a cloud‑based analytics dashboard enabling real‑time leak detection alerts. Pigtek Ltd partnered with a Nigerian university to develop home‑grown sensor components, aiming to reduce import reliance. Quest Integrity Group expanded its service footprint into the Gulf of Guinea, while Protea Pipeline Services released a corrosion‑focused ultrasonic solution for chemical plants in South Africa. T.D. Williamson, Inc. announced a strategic alliance with a regional drilling contractor to integrate pigging services into new pipeline construction projects.