What is the Dental Burs Market Overview – definition, scope, and significance?

The Dental Burs Market encompasses the production, distribution, and consumption of cutting instruments used in dental procedures. These rotary tools, made from diamond or carbide steel, enable precise tooth preparation, shaping, and removal across various dental specialties. The market’s scope spans hospital dentistry units, private dental clinics, and a wide array of applications such as restorative dentistry, orthodontics, endodontics, periodontics, and oral surgery. Its significance lies in supporting clinical efficiency, patient outcomes, and the overall growth of modern dental care services.

What are the key drivers, restraints, challenges, and opportunities shaping the Dental Burs Market?

Primary drivers include rising dental disease prevalence, increasing demand for aesthetic and restorative procedures, and growing investment in dental infrastructure worldwide. Technological advances in bur materials—especially diamond-coated and high‑precision carbide designs—fuel demand for superior performance. Restraints involve high product costs, stringent regulatory approvals, and price sensitivity in emerging markets. Challenges stem from supply chain disruptions and the need for skilled clinicians to utilize advanced burs effectively. Opportunities arise from expanding minimally invasive techniques, digital dentistry integration, and emerging markets adopting modern oral health practices.

What growth trends are currently influencing the Dental Burs Market?

Current trends feature a shift toward single‑use, pre‑sterilized burs to enhance infection control, driven by heightened hygiene standards. Manufacturers are investing in nano‑technology and hybrid coatings to improve cutting efficiency and durability. The rise of CAD/CAM workflows promotes burs compatible with computer‑guided preparations. Additionally, there is a growing preference for diamond burs in high‑precision restorative work, while carbide steel burs retain strong demand in surgical and heavy‑cut applications.

How has COVID‑19 impacted the Dental Burs Market and what is the recovery trajectory?

The pandemic caused temporary clinic closures, reduced patient footfall, and postponed elective procedures, leading to a short‑term dip in bur sales. However, heightened awareness of infection control accelerated adoption of disposable and sterilizable burs. Post‑2020, the market rebounded as dental practices reopened, supported by pent‑up demand for aesthetic and restorative services. The recovery is steady, with growth projected to outpace pre‑pandemic levels due to renewed focus on safety and efficiency.

Who are the major competitors in the Dental Burs Market and how is the competitive landscape evolving?

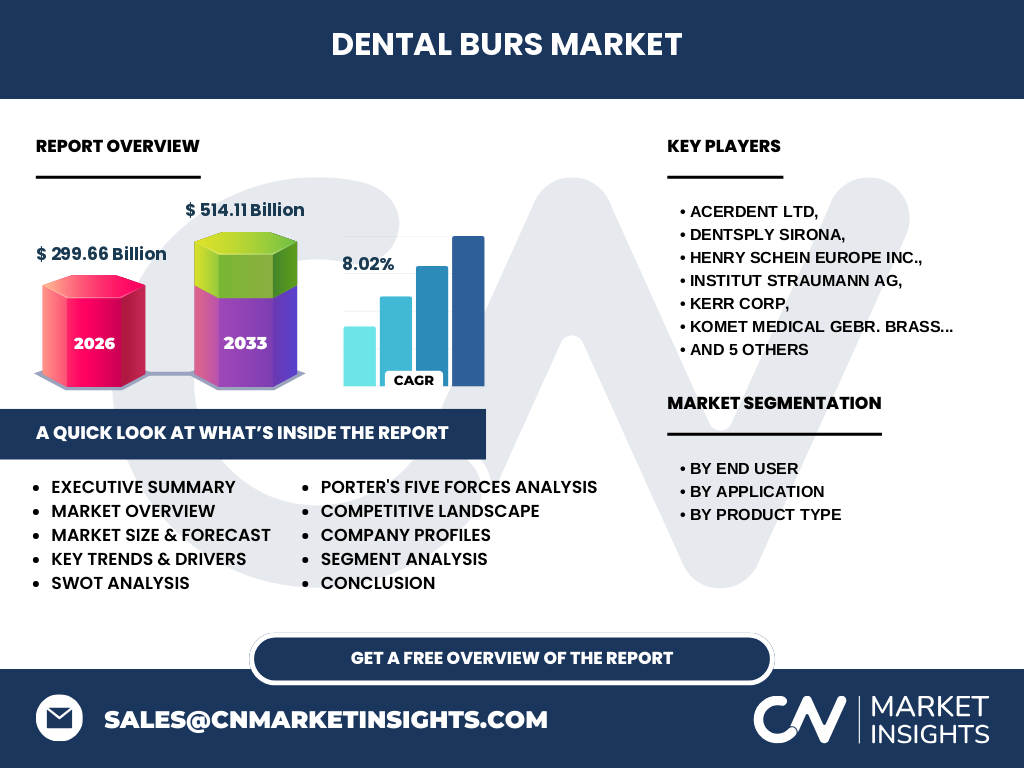

The market is fragmented, featuring both multinational corporations and specialized manufacturers. Key players include Acerdent Ltd, Dentsply Sirona, Henry Schein Europe Inc., Institut Straumann AG, Kerr Corp, Komet Medical Gebr. Brasseler GmbH & Co. KG, MEDIN a.s., NTI KAHLA GmbH, Prima Dental, SYNDENT Tools, and Shofu Global. Companies compete on product innovation, material quality, and distribution reach. Recent consolidation trends involve strategic acquisitions and partnerships aimed at expanding product portfolios and geographic coverage.

What are the high‑level insights from the Executive Summary of the Dental Burs Market?

The Dental Burs Market is valued at 299.66 billion in 2026 and is forecast to reach 514.11 billion by 2033, reflecting an 8.02% CAGR. Growth is propelled by expanding dental services, technological enhancements in bur materials, and increasing demand for minimally invasive procedures. Hospitals and dental clinics are the primary end users, with diamond burs leading in restorative dentistry and carbide steel burs dominating surgical applications. Competitive dynamics are shaped by innovation, regulatory compliance, and strategic collaborations.

What are the forecast projections for the Dental Burs Market from 2025 to 2032?

Based on the provided CAGR of 8.02%, the market is expected to expand steadily, surpassing the 514.11 billion mark by 2033. Annual growth will be driven by continued adoption of advanced bur technologies, rising dental procedure volumes, and geographic expansion into emerging economies. The forecast underscores a robust upward trajectory, indicating strong investment potential and sustained demand across all product types and applications.

How is the Dental Burs Market sized and shared by segmentation?

Segmentation by end user divides the market between hospitals and dental clinics, with clinics representing the larger share due to the high volume of routine restorative work. Application‑wise, restorative dentistry commands the greatest demand, followed by orthodontics, endodontics, periodontics, and oral surgery. By product type, diamond dental burs lead in precision‑critical procedures, while carbide steel burs retain a strong position in high‑stress surgical and heavy‑cut tasks.

What is the global Dental Burs Market size and share by region?

The market’s global footprint includes North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. While specific regional monetary figures are not disclosed, growth is strongest in regions investing heavily in dental infrastructure and advanced treatment modalities—particularly North America and Europe. Emerging markets in Asia‑Pacific are experiencing accelerated adoption due to rising oral health awareness and expanding private dental networks.

What does the regional analysis reveal about Dental Burs Market performance?

North America leads in terms of advanced product adoption, driven by high per‑capita dental expenditure and stringent clinical standards. Europe follows closely, with strong demand for both diamond and carbide burs across public and private sectors. Asia‑Pacific shows the highest growth potential, fueled by rapid urbanization, increasing middle‑class populations, and governmental initiatives promoting oral health. Latin America and MEA regions present moderate growth, constrained by economic variability but benefiting from expanding dental tourism.

Which companies are leading in the Dental Burs Market and what are their strategic approaches?

Leading firms such as Dentsply Sirona and Kerr Corp focus on R&D to launch premium diamond bur lines, leveraging digital dentistry platforms. Henry Schein Europe emphasizes distribution excellence and comprehensive product portfolios. Acerdent Ltd and SYNDENT Tools pursue niche markets with specialized carbide steel burs. Strategic moves include product innovation, acquisitions of boutique manufacturers, and collaborations with dental education institutions to drive brand loyalty.

How does Porter’s Five Forces analysis apply to the Dental Burs Market?

Threat of new entrants is moderate due to high R&D costs and regulatory barriers. Bargaining power of suppliers is low to moderate, as raw material sources (diamond, carbide) are specialized but limited in number. Bargaining power of buyers is moderate; dental clinics negotiate volume discounts, while hospitals demand high‑quality, certified products. Threat of substitutes is low, given the essential role of burs in dental procedures. Industry rivalry is intense, with many firms competing on innovation, price, and service.

What are the SWOT insights for the Dental Burs Market?

Strengths: Essential clinical tool, strong demand across multiple dental specialties, continuous material innovation.

Weaknesses: High unit cost, dependence on regulatory approvals, limited differentiation for basic carbide burs.

Opportunities: Expansion into emerging markets, development of eco‑friendly disposable burs, integration with digital workflow systems.

Threats: Economic downturns affecting elective dental procedures, potential supply constraints of raw materials, evolving infection‑control standards requiring rapid product adaptation.

What does the value chain of the Dental Burs Market look like?

The value chain starts with raw material extraction (diamond, carbide steel) followed by material processing and bur shaping. Next are precision grinding, coating, and quality testing stages. Finished burs are then packaged, distributed through medical supply distributors, and finally sold to hospitals and dental clinics. After‑sales services, including training and sterilization guidelines, add value and support brand differentiation.

What key investment insights can be drawn for the Dental Burs Market?

Investors should target companies with strong R&D pipelines focused on diamond and hybrid bur technologies, as these segments promise higher margins. Strategic acquisitions of niche carbide bur manufacturers can broaden product portfolios and geographic reach. Funding digital‑dental integration projects opens cross‑selling opportunities. Additionally, entering high‑growth regions like Asia‑Pacific through joint ventures can capitalize on expanding oral health infrastructure.

What are the main conclusions of the Dental Burs Market report?

The Dental Burs Market is on a robust growth path, underpinned by an 8.02% CAGR and a projected market size exceeding 514 billion by 2033. Demand is driven by expanding dental services, material innovations, and increasing emphasis on infection control. While competition is fierce, opportunities abound in emerging geographies, digital dentistry linkages, and sustainable product lines. Stakeholders should prioritize innovation, regulatory compliance, and strategic market entry to capture value.

How was the research methodology designed for this Dental Burs Market study?

The study combined primary interviews with key industry executives, dental practitioners, and supply‑chain experts, alongside secondary data collection from reputable databases, company reports, and trade publications. Market sizing employed a top‑down approach anchored on the provided 2026 baseline, while forecasting applied compound annual growth rate calculations. Validation rounds ensured alignment with market participants and cross‑checked data integrity.

What is the scope of this Dental Burs Market research?

The scope covers global market dynamics, segmentation by end user, application, and product type, as well as regional performance across major continents. It includes analysis of competitive landscape, value chain, and strategic recommendations. The study excludes unrelated dental consumables and focuses exclusively on rotary cutting instruments—diamond and carbide steel dental burs—used in clinical dentistry.

Which key companies and recent developments are highlighted in the Dental Burs Market?

Prominent players such as Dentsply Sirona, Kerr Corp, and Henry Schein Europe have launched new diamond‑coated bur series targeting minimally invasive restorative procedures. Acerdent Ltd announced a partnership with a digital dentistry platform to integrate bur selection into treatment planning software. SYNDENT Tools introduced a line of eco‑friendly, biodegradable disposable burs. Shofu Global expanded its distribution network in Asia‑Pacific, reinforcing market presence in high‑growth territories.