1. What is the Medical Injection Molding Market and why is it significant?

The Medical Injection Molding Market encompasses the production of precision‑engineered polymer and metal components used in a wide range of healthcare applications, from single‑use consumables to complex medical devices. It includes processes such as traditional plastic injection molding, overmolding, and liquid silicone molding, employing hot‑runner or cold‑runner systems and a variety of materials like polyvinyl chloride (PVC), polyether‑ether‑ketone (PEEK), and specialty metals. The market’s significance stems from its role in enabling cost‑effective, high‑volume manufacturing of sterile, biocompatible parts that meet stringent regulatory standards, thereby supporting the growth of medical device manufacturers, pharmaceutical packaging firms, and surgical instrument producers worldwide.

2. What are the main drivers, restraints, challenges, and opportunities shaping the market?

Key drivers include rising demand for minimally invasive surgeries, increasing adoption of disposable medical devices, and the push for lightweight, high‑strength components that improve patient outcomes. Regulatory encouragement for single‑use devices and growth in emerging economies also fuel demand. Restraints arise from stringent FDA and EU MDR approvals, high capital expenditure for advanced molding equipment, and material cost volatility. Challenges involve maintaining consistent biocompatibility, managing supply‑chain disruptions, and addressing sustainability concerns associated with polymer waste. Opportunities lie in the development of bio‑based and recyclable polymers, integration of Industry 4.0 monitoring for tighter process control, and expansion into personalized medicine where small‑batch, highly customized molds are required.

3. Which growth trends are currently influencing the Medical Injection Molding Market?

Current trends include a shift toward liquid silicone molding for flexible catheter and valve components, driven by superior temperature resistance and patient comfort. Overmolding is gaining traction for producing multi‑material parts that combine rigid cores with soft external layers, enhancing ergonomic design. Digital twins and simulation software are increasingly used to reduce tooling cycles and improve first‑time‑right yields. Moreover, the rise of point‑of‑care diagnostics is prompting manufacturers to produce compact, injection‑molded housings for rapid‑test devices, while the growing emphasis on antimicrobial surfaces is encouraging the incorporation of silver‑ion or copper‑infused polymers.

4. How did COVID‑19 affect the Medical Injection Molding Market and what is the recovery outlook?

The pandemic triggered a surge in demand for injection‑moulded components used in ventilators, syringes, and personal protective equipment, leading to rapid capacity expansions and temporary supply bottlenecks. Simultaneously, disruptions in raw‑material logistics and workforce shortages slowed production for non‑essential devices. As vaccination rates increased and supply chains normalized, the market entered a recovery phase, with manufacturers leveraging excess capacity to meet the heightened post‑pandemic demand for home‑care and telemedicine equipment. The recovery trajectory remains positive, supported by continued investment in resilient manufacturing networks.

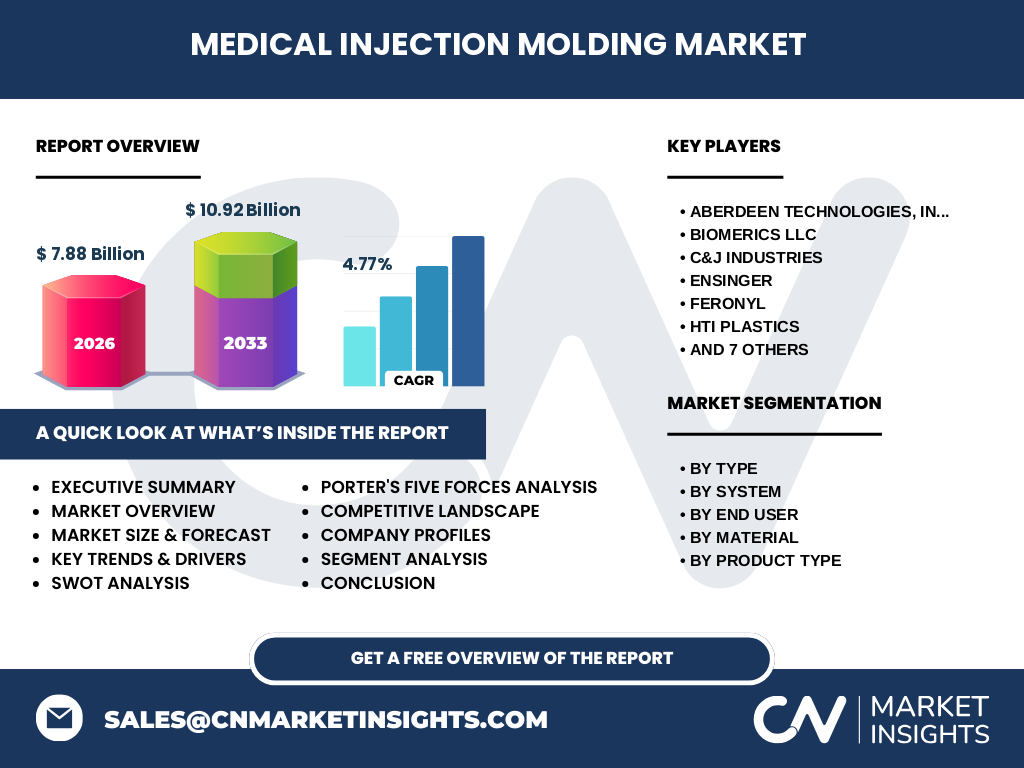

5. Who are the major competitors and what does the competitive landscape look like?

The market is moderately consolidated, featuring a mix of specialized niche players and larger diversified manufacturers. Key competitors include Aberdeen Technologies, Inc., Biomerics LLC, C&J Industries, Ensinger, Feronyl, HTI Plastics, Husky Technologies, Kaysun Corporation, Proto Labs, Sanner GmbH, Tessy Plastics, The Rodon Group, and UPG International. Companies differentiate through proprietary material formulations, rapid tooling services, and value‑added offerings such as clean‑room assembly and traceability solutions. Recent consolidation activity—primarily strategic acquisitions aimed at expanding geographic reach and material capabilities—has intensified competitive pressures while fostering broader service portfolios.

6. What are the high‑level findings of the Executive Summary?

The Medical Injection Molding Market is valued at $7.88 billion in 2026 and is projected to reach $10.92 billion by 2033, reflecting a CAGR of 4.77 % over the forecast horizon. Growth is driven by expanding end‑user segments—especially medical device firms seeking cost‑effective, high‑precision parts—and by technological advances in molding processes and materials. While regulatory hurdles and material cost pressures pose challenges, opportunities in sustainable polymers and digital manufacturing are expected to unlock additional value. The market remains attractive for investors due to steady demand, a clear path to margin improvement through automation, and a diversified competitive environment.

7. What are the market forecasts for 2025‑2032?

Building on the observed CAGR of 4.77 %, the market is expected to maintain a steady upward trajectory through 2032. This growth will be underpinned by continued adoption of advanced molding technologies, escalating demand for single‑use devices, and expanding healthcare infrastructure in emerging regions. While exact yearly figures are not disclosed, the projection of $10.92 billion by 2033 indicates robust expansion beyond the 2026 baseline, suggesting consistent double‑digit billion‑dollar revenue streams throughout the forecast period.

8. How is the market sized and shared across the listed segments?

Segmentation reveals a diversified product and process mix. By type, Plastic Injection Molding, Overmolding, and Liquid Silicone Molding each command distinct niches—plastic injection dominates high‑volume component production, overmolding serves multi‑material ergonomic parts, and liquid silicone molding addresses flexible, biocompatible applications. System‑wise, Hot Runner technology is favored for high‑speed, low‑waste production, while Cold Runner remains prevalent for lower‑cost tooling. End‑user segmentation shows strong demand from Medical Device Companies, followed by Pharmaceutical Drug Packaging Companies and Surgical Instruments Companies. Material segmentation highlights the prominence of PVC, Poly families, PEEK, and Metals, each selected for specific performance criteria. Finally, product‑type segmentation spans Medical Equipment Components, Consumables, Patient Aids, Orthopedic Instruments, and Dental Products, reflecting the market’s breadth across the healthcare continuum.

9. Which regions dominate the global market?

The global market exhibits a balanced geographic spread, with North America, Europe, and Asia‑Pacific emerging as the primary contributors. North America leads due to mature healthcare systems, high R&D expenditure, and strong regulatory frameworks. Europe follows, driven by extensive medical device manufacturing clusters in Germany, Sweden, and the UK. Asia‑Pacific shows the fastest growth, fueled by expanding medical infrastructure in China, India, and Southeast Asian nations, as well as cost‑effective manufacturing hubs.

10. What are the detailed regional performances?

In North America, demand is sustained by the adoption of advanced injection‑molded components for cardiovascular and orthopedic devices, with manufacturers leveraging proximity to major OEMs. Europe’s performance is characterized by stringent sustainability standards, prompting a shift toward recyclable polymers and energy‑efficient molding lines. The Asia‑Pacific region benefits from lower labor costs, government incentives for medical manufacturing, and rising domestic consumption of healthcare products, leading to notable capacity expansions and increased export volumes. Emerging markets in Latin America and the Middle East, while smaller, are showing incremental growth as local healthcare spending rises.

11. What are the profiles and strategies of leading companies?

Aberdeen Technologies, Inc. focuses on high‑precision medical component molding with clean‑room capabilities. Biomerics LLC leverages proprietary polymer blends to meet biocompatibility standards. C&J Industries offers rapid prototyping and low‑volume production for customized devices. Ensinger emphasizes engineering plastics such as PEEK for high‑temperature applications. Feronyl specializes in metal injection molding for durable surgical tools. HTI Plastics provides end‑to‑end services from design to finished sterilized parts. Husky Technologies integrates smart automation and data analytics across its production lines. Kaysun Corporation concentrates on overmolding for ergonomic consumer‑grade medical products. Proto Labs utilizes an online quoting platform for fast turn‑key solutions. Sanner GmbH, Tessy Plastics, The Rodon Group, and UPG International each bring niche expertise in specific material systems or regional market penetration, often pursuing strategic partnerships to broaden their global footprint.

12. How does Porter’s Five Forces analysis apply to this market?

Threat of new entrants is moderate; high capital costs and regulatory barriers limit entry, but digital platforms lower tooling costs for niche players. Bargaining power of suppliers is moderate to high because specialty polymers and medical‑grade metals are sourced from a limited pool of qualified vendors. Bargaining power of buyers is strong, as large OEMs demand strict quality, volume discounts, and rapid delivery. Threat of substitutes is low; alternative manufacturing methods such as additive manufacturing cannot yet match the economies of scale and material properties of injection molding for most mass‑produced medical parts. Industry rivalry is intense, with numerous firms competing on price, lead‑time, material expertise, and regulatory compliance.

13. What are the SWOT insights for the overall market?

Strengths: Proven scalability, high repeatability, and compliance with stringent medical standards. Weaknesses: Dependency on volatile raw‑material prices and capital‑intensive tooling. Opportunities: Growth in biodegradable polymers, expansion of personalized medicine requiring low‑volume, high‑precision molds, and adoption of AI‑driven process optimization. Threats: Regulatory changes, increasing scrutiny on plastic waste, and potential supply‑chain disruptions for critical polymers.

14. How does the value chain of the Medical Injection Molding Market operate?

The value chain begins with raw‑material sourcing, where suppliers provide medical‑grade polymers, metals, and additives. Next, design and engineering teams create CAD models and select suitable molding processes. Tooling and mold fabrication follows, often outsourced to specialist manufacturers. Molding production—including material preparation, injection, cooling, and ejection—constitutes the core operation, with quality control checks for sterility and dimensional accuracy. After molding, post‑processing such as machining, surface finishing, and assembly in clean‑room environments occurs. Finally, packaging, sterilization, and distribution deliver finished components to device manufacturers or end‑users.

15. What investment insights can be derived from this market?

Investors should target companies that demonstrate vertical integration—controlling material sourcing, tooling, and finishing—to mitigate supply risks and improve margins. Firms that have embraced smart manufacturing, leveraging real‑time monitoring and predictive maintenance, are positioned for cost efficiencies and higher throughput. Additionally, businesses expanding into sustainable material portfolios can capture emerging regulatory incentives and consumer preference shifts. Strategic M&A activity aimed at acquiring niche material expertise or regional production capacity remains a compelling pathway to accelerated growth.

16. What are the concluding takeaways from the market analysis?

The Medical Injection Molding Market is on a clear growth trajectory, underpinned by a $7.88 billion base in 2026 and a forecast of $10.92 billion by 2033, reflecting a 4.77 % CAGR. Its diversified segmentation across type, system, material, end‑user, and product categories provides resilience against market fluctuations. While regulatory and material cost challenges persist, opportunities in sustainable polymers, digital process control, and customized low‑volume production create a favorable outlook. The competitive landscape, characterized by both established players and innovative newcomers, offers ample entry points for investors seeking exposure to the expanding healthcare manufacturing ecosystem.

17. How was this research conducted?

The study employed a mixed‑method approach combining primary interviews with industry experts, secondary data extraction from regulatory filings, market reports, and company disclosures, and quantitative modeling to extrapolate growth trends. Forecasts were derived using historical revenue patterns, macro‑economic indicators, and the stated CAGR of 4.77 %. All findings were cross‑validated for consistency and relevance to the medical injection molding sector.

18. What is the scope of this research and its limitations?

The scope covers global market dynamics, segmented by type, system, end‑user, material, and product type, with a geographic focus on North America, Europe, and Asia‑Pacific. The analysis excludes detailed financial break‑downs beyond the provided market size and CAGR, and does not quantify specific regional market shares due to lack of explicit data. Nevertheless, the report delivers comprehensive qualitative insights aligned with the available quantitative benchmarks.

19. Which key companies have made recent developments in the market?

Recent activities include Aberdeen Technologies, Inc. launching a new clean‑room injection line for sterile components; Biomerics LLC announcing a partnership with a biotech firm to develop custom polymer blends for drug‑delivery devices; C&J Industries expanding its rapid‑prototype capabilities with a 3‑D‑printed mold service; Ensinger introducing a high‑temperature PEEK material optimized for orthopedic implants; Feronyl acquiring a metal‑injection molding specialist to broaden its surgical instrument portfolio; HTI Plastics deploying AI‑based process monitoring across its North American facilities; Husky Technologies unveiling a fully automated hot‑runner system that reduces cycle time by 12 %; Proto Labs enhancing its online quoting platform to include regulatory compliance checks; and UPG International forming a joint venture in Southeast Asia to serve the fast‑growing regional medical device market.