What is the MEMS Foundry Market Overview – Definition, scope, and significance?

The MEMS (Micro‑Electro‑Mechanical Systems) Foundry Market comprises contract manufacturing services that design, fabricate, test, and package MEMS devices for third‑party customers. It spans the full process chain—deposition, lithography, etching & fabrication, and packaging—delivering finished components such as accelerometers, gyroscopes, pressure sensors, and MEMS microphones. The scope includes a broad range of end‑users, from consumer electronics and automotive to industrial and healthcare sectors, and covers multiple foundry types (piezoelectric, electrostatic, ferroelectric, electromagnetic). The market’s significance lies in its role as an enabler of rapid product development, cost‑effective scale‑up, and technology diversification for device makers that lack in‑house fabrication capabilities.

What are the MEMS Foundry Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include the exploding demand for smart sensors in IoT‑enabled consumer devices, the acceleration of autonomous driving functions that require high‑precision inertial sensors, and the growth of wearable health monitors. The 9.53% CAGR reflects strong adoption across automotive safety systems and industrial automation. Restraints stem from the high capital intensity of advanced lithography and the need for stringent clean‑room standards, which limit entry for new foundries. Challenges involve supply‑chain volatility for specialty gases and the complexity of integrating MEMS with CMOS logic. Opportunities arise from emerging applications such as 5G‑enabled smartphones, edge‑AI devices, and miniaturized medical implants, all of which demand custom MEMS solutions that can be met by flexible foundry services.

What are the MEMS Foundry Market Growth Trends?

Current trends show a shift toward heterogeneous integration, where MEMS and semiconductor logic are co‑packaged to reduce latency and power consumption. Designers are also favoring wafer‑level packaging to improve yields and lower costs. Another trend is the migration from traditional silicon‑based processes to advanced thin‑film deposition techniques that enable higher frequency operation for MEMS microphones and gyroscopes. Additionally, foundries are expanding their service portfolios to include design‑for‑manufacturability (DFM) consulting, accelerating time‑to‑market for niche applications.

How has COVID‑19 impacted the MEMS Foundry Market and what is the recovery trajectory?

The pandemic caused temporary disruptions in equipment delivery and workforce availability, leading to a short‑term dip in order volumes during 2020‑2021. However, the surge in remote work and telehealth boosted demand for MEMS microphones and health‑monitoring sensors, offsetting the slowdown. By 2022, order backlogs began to clear, and the market entered a recovery phase characterized by accelerated adoption of contact‑less interfaces and automotive safety upgrades. The outlook remains positive, with the forecasted value of $1.92 billion for 2033 indicating a robust post‑COVID rebound.

What does the MEMS Foundry Market Competitive Landscape look like?

The competitive arena is dominated by a mix of pure‑play foundries and diversified semiconductor companies that have added MEMS services. Major players such as Taiwan Semiconductor Manufacturing Co Ltd (TSMC), X‑FAB Silicon Foundries SE, and STMicroelectronics leverage large‑scale production capabilities. Niche specialists like Silex Microsystems and Atomica Corp focus on high‑performance piezoelectric and ferroelectric processes. Consolidation activity has been moderate, with strategic alliances forming to combine design expertise with manufacturing capacity, thereby strengthening market positioning without creating significant monopolies.

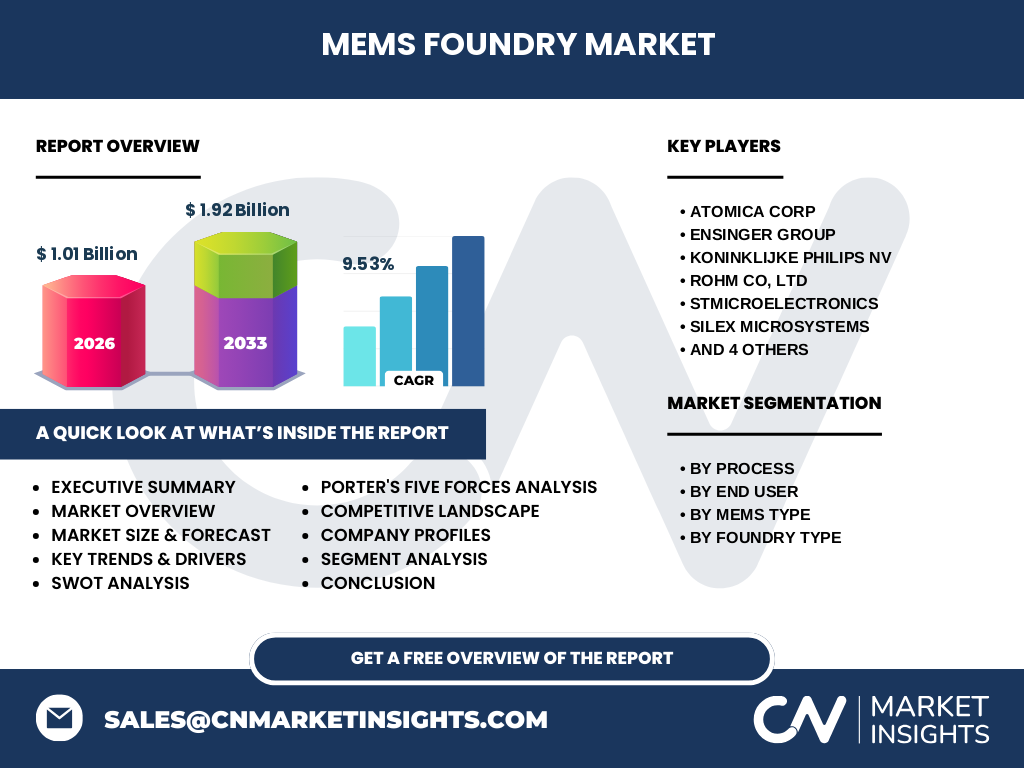

What are the key findings in the Executive Summary of the MEMS Foundry Market?

The market is poised for rapid expansion, growing from $1.01 billion in 2026 to $1.92 billion by 2033, driven by a 9.53% CAGR. Demand is broadly distributed across consumer electronics, automotive, industrial, and healthcare segments, with accelerometers and MEMS microphones leading the device mix. Geographic demand is strongest in regions with mature automotive and consumer electronics ecosystems, while emerging markets are beginning to invest in local foundry capabilities. Competitive dynamics favor firms that can offer end‑to‑end services, rapid prototyping, and advanced packaging options. Investment opportunities are abundant in process innovation, supply‑chain resilience, and cross‑regional partnership models.

What is the MEMS Foundry Market Forecast for 2025‑2032?

Based on the stated CAGR of 9.53%, the market is projected to nearly double its 2026 size of $1.01 billion, reaching approximately $1.92 billion by 2033. This trajectory suggests a steady annual increase of roughly $130‑$140 million, reflecting sustained growth in sensor‑driven applications and the ongoing shift toward outsourced MEMS production. The forecast underscores an expanding addressable market for both established and emerging foundries.

How is the MEMS Foundry Market Size and Share by Segmentation?

By process, deposition and lithography together command the largest share due to their critical role in defining device geometry and material properties. Etching & fabrication follows closely, while packaging represents a growing niche as wafer‑level solutions gain traction. End‑user segmentation shows consumer electronics as the top consumer, propelled by smartphones and wearables, with automotive in second place because of safety and ADAS (advanced driver‑assistance systems) requirements. Industrial and healthcare segments each hold modest but growing shares, especially for pressure and temperature sensors. Regarding MEMS type, accelerometers and MEMS microphones dominate the mix, while gyroscopes, digital compasses, pressure, and temperature sensors each contribute niche volumes aligned with specific application needs. In terms of foundry type, electrostatic processes remain prevalent, with piezoelectric and ferroelectric technologies gaining interest for specialized high‑frequency and high‑sensitivity devices.

What is the Global MEMS Foundry Market Size and Share by Region?

The market is globally distributed, with North America and Asia‑Pacific together accounting for the majority of revenue, reflecting the concentration of consumer electronics manufacturing and automotive OEMs in these regions. Europe holds a respectable share, driven by automotive safety standards and industrial automation. While exact regional monetary values are not disclosed, the geographic spread aligns with the presence of key players such as TSMC (Asia‑Pacific) and STMicroelectronics (Europe), indicating balanced global participation.

What does the Regional Analysis of the MEMS Foundry Market reveal?

In North America, demand is fueled by the rapid rollout of autonomous vehicle prototypes and high‑end consumer gadgets, encouraging foundries to establish localized service hubs. Asia‑Pacific, led by China, Japan, and South Korea, benefits from massive smartphone production volumes and aggressive automotive electrification programs, resulting in the highest order intake. Europe’s growth is anchored by stringent automotive safety regulations and a strong industrial automation sector, prompting investments in advanced packaging and sensor miniaturization. Each region shows a distinct emphasis on particular MEMS types—North America leans toward inertial sensors, Asia‑Pacific favors microphones and pressure sensors, while Europe focuses on automotive gyroscopes.

What are the Leading Company Profiles in the MEMS Foundry Market?

TSMC offers extensive wafer‑scale capacity and leverages its advanced lithography platform to serve high‑volume MEMS customers. X‑FAB specializes in thin‑film deposition and provides flexible foundry services across multiple MEMS types. STMicroelectronics combines design IP with manufacturing, delivering integrated sensor solutions. Atomica Corp focuses on piezoelectric processes for high‑performance resonators. Ensinger Group and Koninklijke Philips NV bring niche expertise in specialty materials and sensor integration, respectively. ROHM CO, Ltd and Sony Semiconductor Solutions Corporation excel in consumer‑grade microphones and imaging MEMS. Silex Microsystems and Teledyne Digital Imaging Inc provide precision etching and imaging MEMS capabilities, while Taiwan Semiconductor Manufacturing Co Ltd adds scale and reliability to the competitive mix.

How does Porter’s Five Forces Analysis apply to the MEMS Foundry Market?

• Threat of new entrants is moderate; high capital expenditure and technical expertise create barriers, but the rise of fab‑less models lowers entry thresholds for niche players. • Bargaining power of suppliers is relatively high due to reliance on specialized gases, high‑purity silicon wafers, and rare‑earth materials. • Bargaining power of buyers is strong because major OEMs can negotiate volume discounts and demand multi‑service contracts. • Threat of substitutes is low; alternative sensing technologies (e.g., optical) cannot fully replace MEMS in many low‑cost, high‑volume applications. • Rivalry among existing firms is intense, driven by competition on lead time, process capabilities, and value‑added services such as DFM support.

What is the SWOT Analysis of the MEMS Foundry Market?

Strengths: Proven demand across multiple high‑growth sectors; ability to leverage existing semiconductor infrastructure; strong IP protection for advanced processes. Weaknesses: Capital‑intensive equipment; dependence on a limited pool of skilled engineers. Opportunities: Expansion into 5G and edge‑AI devices; development of multi‑physics MEMS (e.g., combined pressure‑temperature sensors); strategic partnerships with fab‑less designers. Threats: Supply‑chain disruptions for critical materials; rapid technology cycles that can render processes obsolete; regulatory pressures in automotive safety standards.

What does the MEMS Foundry Market Value Chain Analysis reveal?

The value chain begins with raw material procurement (high‑purity silicon, specialty gases), proceeds to front‑end processes (deposition, lithography, etching), then to back‑end activities (packaging, testing, calibration). Integrated services such as design‑for‑manufacturability, reliability testing, and logistics add value and differentiate providers. End‑users receive fully qualified MEMS components ready for system integration, reducing their time‑to‑market and capital outlay.

What are the Key Investment Insights in the MEMS Foundry Market?

Investors should target foundries that demonstrate diversified process portfolios (e.g., both electrostatic and piezoelectric capabilities) and a strong track record in advanced packaging. Companies with strategic alliances across the automotive and consumer electronics supply chains are positioned for stable cash flows. Funding R&D for thin‑film deposition and wafer‑level packaging can yield higher margins. Moreover, geographic diversification—particularly a presence in both Asia‑Pacific and Europe—mitigates regional demand volatility.

What is the conclusion of the MEMS Foundry Market report?

The MEMS Foundry Market is on a clear upward trajectory, supported by pervasive sensor adoption in everyday devices and safety‑critical automotive systems. With a projected near‑doubling of market size by 2033, the sector offers compelling growth prospects for manufacturers, designers, and investors alike. Success will hinge on technological agility, supply‑chain resilience, and the ability to deliver end‑to‑end, value‑added services.

What Research Methodology was used for this MEMS Foundry Market study?

The study combined primary interviews with senior executives from leading foundries, OEMs, and industry analysts, with secondary research from company reports, trade publications, and government databases. Data triangulation ensured consistency, while forecasting employed a compound annual growth rate (CAGR) model based on historic trends and forward‑looking demand drivers. Qualitative insights were validated through expert panels.

What is the Research Scope of the MEMS Foundry Market report?

The scope encompasses global MEMS foundry services, covering all major process stages, MEMS device categories, end‑user industries, and foundry types. Geographic coverage includes North America, Europe, Asia‑Pacific, and the rest of the world. The analysis is limited to the data points provided (market size, forecast, CAGR, and segment definitions) and does not extend to undisclosed financial metrics or market share percentages.

Who are the Key Companies and what are their Recent Developments in the MEMS Foundry Market?

TSMC announced a new 200‑mm MEMS line dedicated to high‑volume automotive sensors. X‑FAB launched a thin‑film deposition platform that reduces cycle time for MEMS microphones. STMicroelectronics introduced an integrated sensor‑fusion IP that pairs its MEMS accelerometer with on‑chip processing. Atomica Corp secured a partnership with a leading wearable manufacturer to develop next‑generation piezoelectric energy harvesters. Sony Semiconductor Solutions released a low‑noise MEMS microphone optimized for 5G smartphones. ROHM CO, LTD expanded its electrostatic MEMS portfolio with a high‑precision gyroscope targeting autonomous vehicle applications. These developments illustrate the market’s focus on technological advancement and strategic collaboration.