Data Center Liquid Cooling Market Overview - Definition, scope, and significance

Data center liquid cooling represents an advanced thermal management solution that uses liquid-based systems to dissipate heat from IT equipment in data centers. Unlike traditional air cooling methods, liquid cooling employs water, dielectric fluids, or other cooling liquids to transfer heat more efficiently from servers, storage systems, and networking equipment. The scope of this market encompasses various cooling architectures including room-based, row-based, and rack-based solutions, serving diverse data center types from hyperscale facilities to enterprise installations. The significance of liquid cooling has grown exponentially as data centers face increasing power densities due to AI workloads, high-performance computing, and edge computing deployments. With global data center power consumption projected to reach 800 TWh by 2025, efficient cooling solutions have become critical for operational sustainability and cost management.

Data Center Liquid Cooling Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers propelling market growth include the exponential increase in data center power densities, rising energy costs, and stringent environmental regulations pushing for sustainable cooling solutions. The proliferation of AI, machine learning, and high-performance computing applications creates unprecedented thermal challenges that liquid cooling uniquely addresses. However, the market faces restraints such as high initial implementation costs, complex integration requirements with existing infrastructure, and concerns about potential leaks damaging sensitive equipment. Key challenges include the need for specialized expertise in system design and maintenance, compatibility issues with legacy hardware, and the lack of standardized protocols across the industry. Significant opportunities exist in emerging markets, the development of more efficient cooling fluids, integration with renewable energy systems, and the expansion of edge computing facilities requiring compact cooling solutions.

Data Center Liquid Cooling Market Growth Trends - Current and emerging trends shaping the market

Current growth trends indicate a strong shift toward direct-to-chip cooling solutions, which offer superior heat removal efficiency for high-density server environments. The market is witnessing increased adoption of two-phase immersion cooling technologies, particularly in hyperscale data centers supporting AI and machine learning workloads. Modular and scalable liquid cooling systems are gaining traction as they allow data center operators to incrementally upgrade their cooling infrastructure. Emerging trends include the integration of artificial intelligence for predictive cooling management, development of environmentally friendly cooling fluids with lower global warming potential, and the convergence of liquid cooling with power delivery systems for improved overall efficiency. The rise of edge computing is driving demand for compact, high-efficiency liquid cooling solutions that can operate in space-constrained environments while maintaining optimal thermal performance.

COVID-19 Impact on the Data Center Liquid Cooling Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted supply chains and delayed data center construction projects, creating short-term challenges for the liquid cooling market. However, the crisis paradoxically accelerated long-term demand as organizations rapidly expanded digital infrastructure to support remote work, online services, and cloud computing. The pandemic highlighted the critical importance of data center reliability and efficiency, prompting many operators to invest in advanced cooling solutions to optimize existing facilities rather than building new ones. Recovery trajectory shows strong momentum with increased focus on energy efficiency and sustainability, as organizations seek to reduce operational costs while meeting environmental targets. The shift toward hybrid work models continues to drive data center expansion, creating sustained demand for efficient cooling solutions that can handle increased workloads and power densities.

Data Center Liquid Cooling Market Competitive Landscape - Major competitors and market consolidation

The competitive landscape features a mix of established industrial giants and specialized cooling technology providers competing for market share. Major players like Carrier Global Corp, Daikin Industries Ltd, and Schneider Electric SE leverage their extensive HVAC expertise and global distribution networks to maintain strong market positions. Specialized companies such as Asetek, Inc and Vertiv Group Corp focus on innovative cooling technologies and customized solutions for high-density computing environments. The market shows signs of consolidation as larger companies acquire innovative startups to expand their technology portfolios and market reach. Competition is intensifying around technological innovation, with companies investing heavily in R&D to develop more efficient cooling fluids, smarter control systems, and integrated power-cooling solutions. Geographic expansion, particularly in Asia-Pacific and emerging markets, remains a key competitive strategy as data center construction accelerates globally.

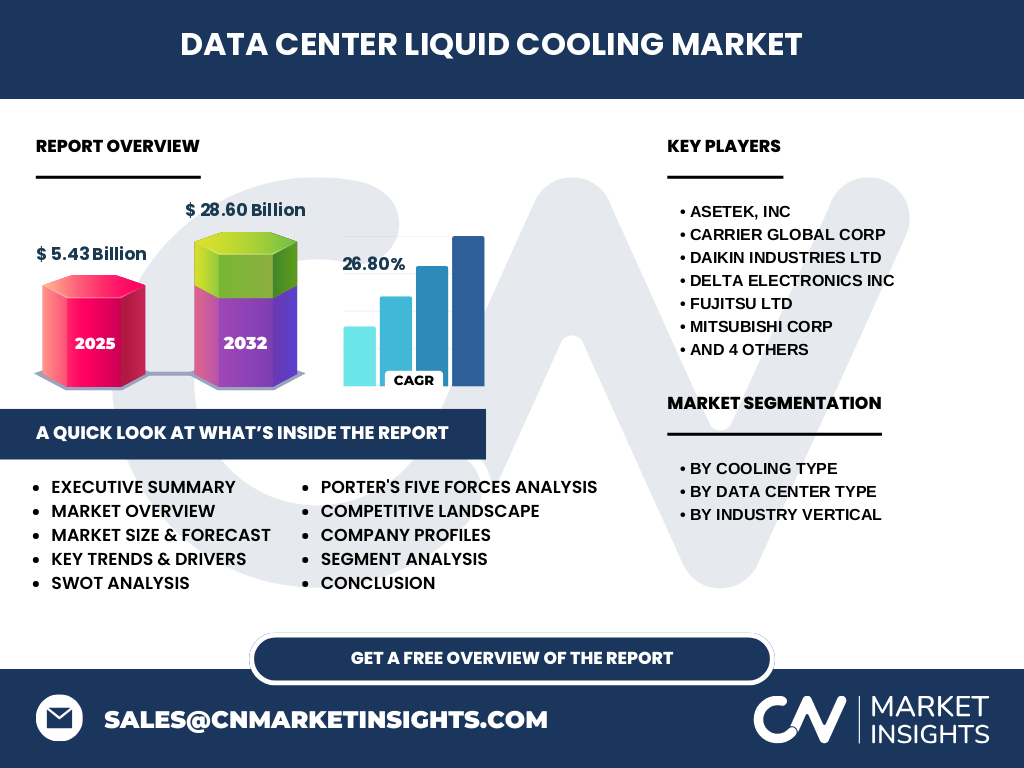

Executive Summary - High-level overview and key findings about Data Center Liquid Cooling Market

The Data Center Liquid Cooling market is experiencing unprecedented growth driven by the exponential increase in data center power densities and the urgent need for energy-efficient cooling solutions. With the market size projected to grow from $5.43 billion in 2025 to $28.60 billion by 2032, representing a remarkable CAGR of 26.80%, the industry is undergoing a fundamental transformation in thermal management approaches. The shift from traditional air cooling to liquid-based solutions is being accelerated by AI workloads, high-performance computing demands, and sustainability requirements. Key findings indicate that rack-based cooling solutions are gaining the most traction due to their scalability and efficiency, while hyperscale data centers represent the largest adoption segment. The IT and telecom sector leads industry vertical adoption, followed closely by BFSI and healthcare sectors. Regional analysis reveals strong growth across all geographic markets, with Asia-Pacific showing the fastest expansion rates due to massive data center construction activity.

Data Center Liquid Cooling Market Forecast - Projections for 2025-2032 period

The forecast period from 2025 to 2032 presents a robust growth trajectory for the Data Center Liquid Cooling market, with projections indicating substantial expansion across all market segments and regions. Starting from a base of $5.43 billion in 2025, the market is expected to reach $28.60 billion by 2032, driven by compound annual growth rate of 26.80%. This exceptional growth rate reflects the accelerating adoption of liquid cooling technologies as data centers worldwide grapple with increasing power densities and energy efficiency requirements. The forecast suggests that room-based cooling solutions will maintain steady growth, while row-based and rack-based solutions will experience the highest growth rates due to their superior efficiency in high-density environments. By 2032, rack-based cooling is projected to capture the largest market share, particularly in hyperscale data centers supporting AI and machine learning workloads. The forecast also indicates that emerging markets in Asia-Pacific and Latin America will contribute significantly to overall growth, driven by rapid digital transformation and increasing data center construction activity.

Data Center Liquid Cooling Market Size and Share by Segmentation - Breakdown by {segmentData}

The market segmentation reveals distinct patterns in adoption and growth across different cooling types, data center categories, and industry verticals. By cooling type, rack-based cooling solutions currently dominate the market due to their superior efficiency in high-density computing environments, followed by row-based and room-based solutions. The rack-based segment is expected to maintain its leadership position throughout the forecast period, driven by increasing adoption in hyperscale data centers and AI-focused facilities. By data center type, hyperscale data centers represent the largest segment, accounting for significant market share due to their massive power requirements and focus on operational efficiency. Colocation data centers show the fastest growth rate as they expand to meet increasing demand for shared infrastructure. Among industry verticals, the IT and telecom sector leads adoption, driven by cloud service providers and telecommunications companies expanding their infrastructure. The BFSI sector shows strong growth potential due to increasing digitalization and data processing requirements, while healthcare and manufacturing sectors are emerging as significant adopters of liquid cooling technologies.

Global Data Center Liquid Cooling Market Size and Share by Region - Geographic distribution

The global distribution of the Data Center Liquid Cooling market reveals varying adoption rates and growth patterns across different geographic regions. North America currently leads the market, driven by the presence of major technology companies, extensive hyperscale data center infrastructure, and early adoption of advanced cooling technologies. The region benefits from strong technological infrastructure, favorable regulatory environment for data center construction, and high concentration of cloud service providers. Europe represents the second-largest market, characterized by stringent energy efficiency regulations and strong focus on sustainable cooling solutions. The Asia-Pacific region shows the fastest growth rate, driven by massive data center construction activity in countries like China, India, and Singapore, along with increasing adoption of cloud services and digital transformation initiatives. Latin America and Middle East & Africa regions, while currently smaller markets, demonstrate significant growth potential due to expanding digital infrastructure and increasing investment in data center facilities. Regional variations in energy costs, climate conditions, and regulatory frameworks influence the specific cooling solutions adopted in each market.

Regional Analysis of the Data Center Liquid Cooling Market - Detailed regional market performance

Regional performance analysis reveals distinct market dynamics and growth drivers across different geographic areas. In North America, the market is characterized by rapid technology adoption, with major cloud providers and technology companies leading the transition to liquid cooling solutions. The region's mature data center infrastructure and focus on energy efficiency create favorable conditions for market growth. Europe shows strong emphasis on sustainable cooling solutions, driven by strict environmental regulations and carbon reduction targets. The region's focus on circular economy principles influences cooling technology development and adoption patterns. Asia-Pacific demonstrates explosive growth potential, with countries like China, Japan, and Singapore investing heavily in data center infrastructure to support digital transformation initiatives. The region's diverse climate conditions and varying energy costs create unique challenges and opportunities for cooling solution providers. Emerging markets in Latin America and Middle East & Africa show increasing adoption of liquid cooling technologies as they build new data center facilities to support growing digital economies. Each region presents unique opportunities and challenges based on local market conditions, regulatory frameworks, and technological maturity levels.

Leading Company Profiles in the Data Center Liquid Cooling Market - Industry players and strategies

The leading companies in the Data Center Liquid Cooling market employ diverse strategies to capture market share and drive innovation. Asetek, Inc has established itself as a pioneer in direct-to-chip cooling solutions, focusing on high-performance computing and AI applications. The company's strategy emphasizes technological innovation and partnerships with major server manufacturers. Carrier Global Corp leverages its extensive HVAC expertise and global distribution network to offer comprehensive cooling solutions, with a strategy focused on integrated systems and energy efficiency. Daikin Industries Ltd combines its air conditioning leadership with liquid cooling innovations, targeting both traditional data centers and emerging edge computing applications. Delta Electronics Inc focuses on energy-efficient solutions and smart cooling management systems, emphasizing integration with renewable energy sources. Fujitsu Ltd brings its extensive experience in high-performance computing to develop specialized cooling solutions for demanding applications. Mitsubishi Corp leverages its global trading network and technical expertise to provide customized cooling solutions across different market segments. Rittal GmbH & Co KG emphasizes modular and scalable solutions, while Schneider Electric SE focuses on integrated power and cooling management systems. Stulz SpA specializes in precision cooling solutions, and Vertiv Group Corp offers comprehensive infrastructure solutions including advanced cooling technologies.

Porter's Five Forces Analysis of the Data Center Liquid Cooling Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the Data Center Liquid Cooling market. The threat of new entrants remains moderate due to high capital requirements, technical expertise needed, and established relationships between existing players and data center operators. However, technological advancements and growing market demand may attract new specialized entrants focusing on niche applications. Bargaining power of suppliers is relatively low as multiple component manufacturers exist, though specialized cooling fluids and components may have limited suppliers. The bargaining power of buyers is increasing as data center operators become more knowledgeable about cooling technologies and demand customized solutions with better price-performance ratios. Threat of substitutes exists from alternative cooling technologies such as advanced air cooling systems and free cooling solutions, though liquid cooling's superior efficiency maintains its competitive advantage. Competitive rivalry is intense among established players, driving innovation, price competition, and strategic partnerships. The analysis indicates that companies focusing on technological differentiation, comprehensive service offerings, and strategic partnerships are best positioned to succeed in this evolving market.

The threat of new entrants remains moderate due to high capital requirements, technical expertise needed, and established relationships between existing players and data center operators. However, technological advancements and growing market demand may attract new specialized entrants focusing on niche applications. Bargaining power of suppliers is relatively low as multiple component manufacturers exist, though specialized cooling fluids and components may have limited suppliers. The bargaining power of buyers is increasing as data center operators become more knowledgeable about cooling technologies and demand customized solutions with better price-performance ratios. Threat of substitutes exists from alternative cooling technologies such as advanced air cooling systems and free cooling solutions, though liquid cooling's superior efficiency maintains its competitive advantage. Competitive rivalry is intense among established players, driving innovation, price competition, and strategic partnerships. The analysis indicates that companies focusing on technological differentiation, comprehensive service offerings, and strategic partnerships are best positioned to succeed in this evolving market.

SWOT Analysis of the Data Center Liquid Cooling Market - Strengths, weaknesses, opportunities, threats

Strengths of the Data Center Liquid Cooling market include superior heat removal efficiency compared to traditional air cooling, growing technological maturity of liquid cooling solutions, and increasing environmental regulations driving adoption of energy-efficient technologies. The market benefits from strong demand drivers including AI workloads, high-performance computing, and edge computing expansion. Weaknesses include high initial implementation costs, complexity of integration with existing infrastructure, and concerns about potential leaks damaging sensitive equipment. The market also faces challenges related to specialized maintenance requirements and limited availability of skilled technicians. Opportunities are abundant in emerging markets, development of more efficient cooling fluids, integration with renewable energy systems, and expansion into new industry verticals such as healthcare and manufacturing. The growing focus on sustainability and energy efficiency creates additional opportunities for innovative cooling solutions. Threats include economic downturns affecting data center construction, potential technological disruptions from alternative cooling methods, and regulatory changes that could impact adoption rates. Supply chain disruptions and raw material price volatility also pose ongoing risks to market growth.

Data Center Liquid Cooling Market Value Chain Analysis - Industry structure and value flow

The value chain analysis of the Data Center Liquid Cooling market reveals a complex ecosystem involving multiple stakeholders and value-adding activities. At the foundation, raw material suppliers provide specialized components including cooling fluids, pumps, heat exchangers, and piping systems. Component manufacturers transform these materials into specialized cooling system elements, while system integrators combine these components into complete cooling solutions. Original equipment manufacturers (OEMs) incorporate cooling systems into their server and data center infrastructure products, working closely with cooling technology providers. Distributors and channel partners facilitate market reach and provide local support services. End-users, primarily data center operators and IT departments, represent the final link in the value chain, benefiting from improved cooling efficiency and reduced operational costs. Value is created through technological innovation, system integration expertise, and comprehensive service offerings. The analysis shows that companies controlling multiple value chain stages, particularly those combining technology development with system integration and service capabilities, are best positioned to capture value and maintain competitive advantage in the market.

Key Investment Insights in the Data Center Liquid Cooling Market - Strategic investment recommendations

Strategic investment insights indicate that the Data Center Liquid Cooling market presents compelling opportunities for investors across multiple segments and technologies. Key investment areas include companies developing advanced cooling fluids with improved thermal properties and environmental characteristics, as well as those focusing on integrated cooling-power delivery systems. Investment in R&D for two-phase immersion cooling technologies shows strong potential, particularly for hyperscale data centers supporting AI and machine learning workloads. The rack-based cooling segment represents an attractive investment opportunity due to its scalability and efficiency advantages in high-density environments. Geographic expansion in Asia-Pacific markets offers significant growth potential, driven by massive data center construction activity and increasing digital transformation initiatives. Strategic investments in companies offering comprehensive service and maintenance solutions are recommended, as the market matures and operators seek long-term partnerships for system optimization and support. Investors should also consider opportunities in companies developing AI-driven cooling management systems and those focusing on sustainable cooling solutions that align with environmental regulations and corporate sustainability goals.

Data Center Liquid Cooling Market Conclusion - Summary and key takeaways

The Data Center Liquid Cooling market stands at a transformative juncture, driven by unprecedented demand for efficient thermal management solutions in increasingly power-dense computing environments. The market's projected growth from $5.43 billion in 2025 to $28.60 billion by 2032, representing a CAGR of 26.80%, underscores the critical importance of liquid cooling technologies in modern data center operations. Key takeaways include the dominance of rack-based cooling solutions, the leading role of hyperscale data centers in driving adoption, and the strong growth potential in emerging markets and new industry verticals. The competitive landscape remains dynamic, with established players and specialized technology providers competing through innovation and strategic partnerships. Success factors include technological differentiation, comprehensive service offerings, and the ability to address sustainability requirements. As data centers continue to evolve to support AI, edge computing, and high-performance applications, liquid cooling technologies will play an increasingly vital role in ensuring operational efficiency, reliability, and environmental sustainability.

Research Methodology - How this research was conducted

The research methodology employed for this market analysis combines extensive primary and secondary research approaches to ensure comprehensive and accurate market insights. Primary research involved interviews with industry experts, data center operators, technology providers, and end-users to gather firsthand information about market trends, challenges, and opportunities. Secondary research encompassed analysis of company annual reports, industry publications, technical journals, and market databases to validate findings and provide historical context. The research methodology included detailed segmentation analysis, competitive landscape assessment, and regional market evaluation using both top-down and bottom-up approaches. Data triangulation techniques were employed to cross-verify information from multiple sources, ensuring reliability and accuracy of market projections. The analysis incorporated consideration of macroeconomic factors, technological trends, regulatory environment, and industry-specific dynamics to provide a holistic view of the market. Special attention was given to emerging technologies and their potential impact on market evolution over the forecast period.

Research Scope - Coverage and limitations

The research scope encompasses a comprehensive analysis of the global Data Center Liquid Cooling market, covering all major segments, regions, and key industry players. The study includes detailed examination of cooling types (room-based, row-based, and rack-based), data center categories (hyperscale, colocation, wholesale, and enterprise), and industry verticals (IT and telecom, BFSI, healthcare, manufacturing, government and defense, media and entertainment, retail, energy, and others). Regional coverage includes North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with detailed analysis of market dynamics in each region. The research timeframe extends from 2025 to 2032, with historical data and future projections providing context for market evolution. Limitations of the research include the rapidly evolving nature of cooling technologies, which may impact adoption rates and market dynamics beyond the forecast period. Additionally, the study focuses on commercially available liquid cooling solutions and may not fully capture emerging experimental technologies still in development phases. Market data and projections are based on available information and industry expert insights, subject to potential variations based on unforeseen technological breakthroughs or economic conditions.

Key Companies and Recent Developments in the Data Center Liquid Cooling Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Key companies in the Data Center Liquid Cooling market have been actively pursuing strategic initiatives to strengthen their market positions and drive technological innovation. Asetek, Inc recently announced advancements in direct-to-chip cooling solutions specifically designed for AI and high-performance computing applications, including new cold plate designs with improved thermal conductivity. Carrier Global Corp unveiled its expanded portfolio of liquid cooling solutions at a major industry conference, emphasizing integration with their existing HVAC systems for comprehensive data center climate control. Daikin Industries Ltd launched a new line of environmentally friendly cooling fluids with reduced global warming potential, targeting the growing demand for sustainable cooling solutions. Delta Electronics Inc announced a strategic partnership with a major cloud service provider to develop customized cooling solutions for next-generation data centers supporting AI workloads. Fujitsu Ltd introduced advanced immersion cooling systems designed for high-density computing environments, featuring improved fluid circulation and heat exchange efficiency. Mitsubishi Corp expanded its presence in the Asia-Pacific market through strategic acquisitions of local cooling technology providers. Rittal GmbH & Co KG launched modular liquid cooling systems offering greater flexibility and scalability for edge computing applications. Schneider Electric SE announced integration of their liquid cooling solutions with their EcoStruxure platform for enhanced monitoring and control capabilities. Stulz SpA introduced new precision cooling units with improved energy efficiency ratings and smart control features. Vertiv Group Corp announced expansion of their manufacturing capabilities to meet increasing demand for liquid cooling solutions in emerging markets. These developments reflect the industry's focus on innovation, sustainability, and market expansion to address evolving data center cooling requirements.