Europe Agricultural Biologicals Market Overview - Definition, scope, and significance?

The Europe Agricultural Biologicals Market encompasses products derived from living organisms or natural processes that are used to protect crops, enhance growth, and improve soil health. It includes bio‑pesticides, bio‑stimulants, and bio‑fertilizers sourced from microbials and bio‑chemicals, applied across cereals, oilseeds, pulses, fruits, and vegetables via foliar sprays, soil treatments, or seed treatments. The market is significant as it supports sustainable agriculture, reduces reliance on synthetic chemicals, and aligns with EU environmental policies.

Europe Agricultural Biologicals Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include stringent EU regulations limiting synthetic pesticide residues, rising consumer demand for organic produce, and government incentives for eco‑friendly farming practices. Opportunities arise from advances in microbial technology, expanding biostimulant research, and increasing adoption of precision agriculture. Restraints involve higher production costs, limited large‑scale field validation, and regulatory complexity across member states. Challenges stem from farmer awareness gaps and variability in product efficacy under diverse climatic conditions.

Europe Agricultural Biologicals Market Growth Trends - Current and emerging trends shaping the market?

Current trends highlight a shift toward integrated pest management (IPM) programs that embed bio‑pesticides with cultural practices. Emerging trends include the rise of seed‑treatment bio‑formulations, leveraging CRISPR‑edited microbial strains for enhanced activity, and growing investment in digital platforms that match biological solutions to specific crop stressors. The market also sees increasing collaboration between biotech firms and agronomic service providers to deliver bundled solutions.

COVID-19 Impact on the Europe Agricultural Biologicals Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially disrupted supply chains for raw biological materials, causing short‑term inventory shortages. However, the crisis accelerated interest in resilient farming inputs, as growers sought alternatives to volatile chemical markets. Post‑2020, demand rebounded strongly, supported by EU stimulus packages that emphasized sustainable agriculture. The market has entered a robust recovery phase, maintaining momentum toward the projected 11.36% CAGR.

Europe Agricultural Biologicals Market Competitive Landscape - Major competitors and market consolidation?

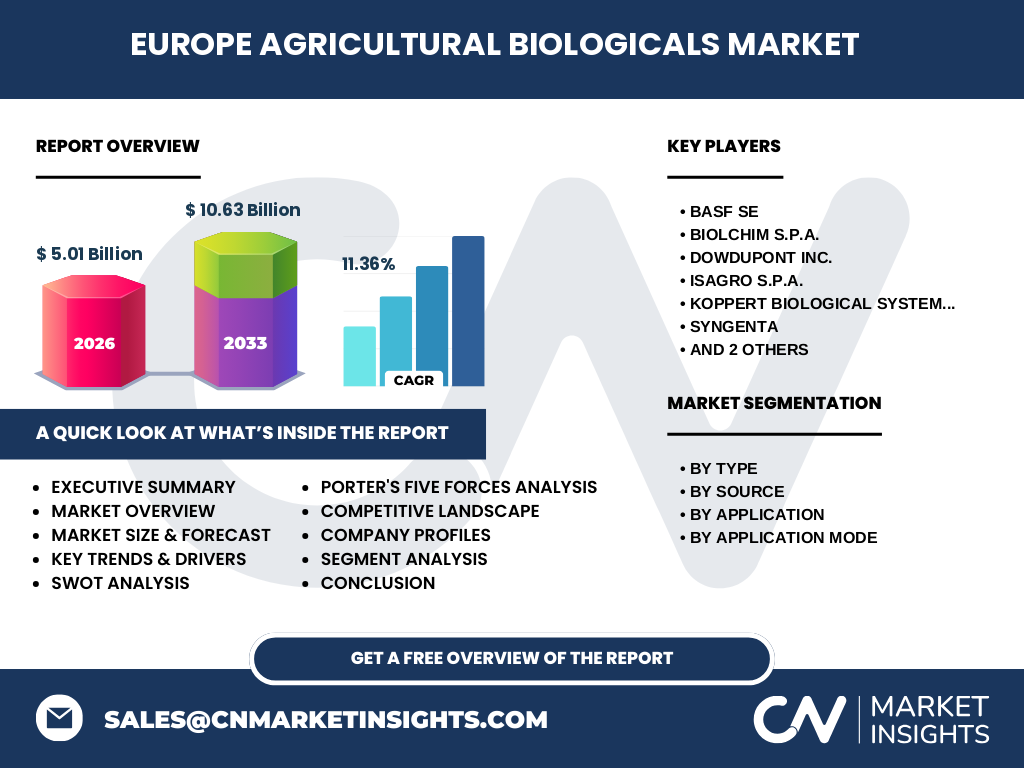

The competitive arena is led by multinational agro‑chemical giants and specialized bio‑technology firms. Key players such as BASF SE, Syngenta, DowDuPont Inc., UPL, and Valent BioSciences LLC dominate through extensive product portfolios and R&D capabilities. Smaller innovators like Biolchim S.p.A., Isagro S.p.A., and Koppert Biological Systems focus on niche microbial strains. Recent years have seen strategic acquisitions and joint ventures aimed at expanding bio‑product pipelines and geographic reach.

Executive Summary - High-level overview and key findings about Europe Agricultural Biologicals Market?

The Europe Agricultural Biologicals Market is valued at €5.01 billion in 2026 and is projected to reach €10.63 billion by 2033, delivering an 11.36% CAGR. Growth is driven by regulatory pressure, sustainability goals, and technological advances in microbial and bio‑chemical solutions. While cost and regulatory heterogeneity pose challenges, strategic partnerships and product innovation create ample opportunities. Leading firms are consolidating to strengthen market position and accelerate commercialization.

Europe Agricultural Biologicals Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 11.36%, the market is expected to more than double its 2026 size of €5.01 billion by 2033, reaching €10.63 billion. This trajectory suggests steady annual growth throughout the 2025‑2032 horizon, underpinned by expanding adoption of bio‑fertilizers and bio‑stimulants across major European cropping systems, and continued policy support for low‑input agriculture.

Europe Agricultural Biologicals Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by type reveals three primary categories: bio‑pesticides, bio‑stimulants, and bio‑fertilizers. By source, the market divides into microbials and bio‑chemicals, each supporting the product types. Application segmentation includes cereals and grains, oilseeds and pulses, and fruits and vegetables, while application mode segments cover foliar sprays, soil treatments, and seed treatments. These segments collectively shape demand patterns and inform product development priorities.

Global Europe Agricultural Biologicals Market Size and Share by Region - Geographic distribution?

Europe represents a leading region within the global agricultural biologicals landscape, driven by progressive environmental policies and robust research infrastructure. While exact global figures are not disclosed, Europe’s market of €5.01 billion (2026) highlights its substantial share relative to other continents, reinforcing the region’s role as a catalyst for worldwide adoption of biological crop solutions.

Regional Analysis of the Europe Agricultural Biologicals Market - Detailed regional market performance?

Within Europe, Northern and Western countries exhibit the highest uptake due to stringent pesticide regulations and strong organic farming sectors. Central and Eastern Europe show rapid growth, propelled by EU-funded sustainability programs and increasing farmer education. Southern markets, while traditionally reliant on chemical inputs, are gradually integrating bio‑products to address drought stress and soil degradation, creating a balanced regional growth pattern.

Leading Company Profiles in the Europe Agricultural Biologicals Market - Industry players and strategies?

Key companies include BASF SE, which leverages its extensive R&D network to launch microbially‑based seed treatments; Syngenta, focusing on integrated digital platforms for bio‑pesticide deployment; DowDuPont Inc., expanding its bio‑chemical portfolio for soil health; UPL, pursuing aggressive acquisitions of niche biotech firms; Valent BioSciences LLC, specializing in specialty bio‑pesticides. Smaller innovators such as Biolchim, Isagro, and Koppert emphasize custom microbial solutions and strong local distribution networks.

Porter's Five Forces Analysis of the Europe Agricultural Biologicals Market - Competitive forces assessment?

Threat of new entrants is moderate due to high R&D costs and regulatory barriers. Supplier power is moderate; raw microbial strains are specialized but sourced from a limited number of labs. Buyer power is growing as farmers gain access to comparative efficacy data and demand cost‑effective solutions. Rivalry among existing firms is intense, driven by product innovation and geographic expansion. Substitute threat remains low, given tightening restrictions on synthetic chemicals.

SWOT Analysis of the Europe Agricultural Biologicals Market - Strengths, weaknesses, opportunities, threats?

Strengths: strong regulatory support, increasing sustainability focus, and advanced biotech capabilities. Weaknesses: higher upfront costs and variability in field performance. Opportunities: development of next‑generation microbial consortia, expansion into seed‑treatment markets, and digital agronomy integration. Threats: regulatory divergence across EU member states, potential market saturation, and competition from emerging synthetic alternatives that claim lower cost.

Europe Agricultural Biologicals Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with R&D and strain discovery, followed by fermentation or synthesis of active ingredients. Next are formulation and packaging stages, where microbials and bio‑chemicals are blended into user‑friendly formats. Distribution channels include specialized agro‑chemical distributors, direct sales to large farms, and online platforms. End‑users—farmers and agronomists—apply the products via foliar sprays, soil treatments, or seed treatments, completing the cycle.

Key Investment Insights in the Europe Agricultural Biologicals Market - Strategic investment recommendations?

Investors should prioritize companies with strong pipelines in microbial seed treatments and digital agronomy services, as these segments forecast the highest growth. Funding R&D collaborations between universities and biotech firms can accelerate time‑to‑market. Acquisitions of niche firms possessing proprietary strains offer rapid portfolio expansion. Additionally, allocating capital to scalable fermentation facilities will address supply‑chain constraints and improve cost competitiveness.

Europe Agricultural Biologicals Market Conclusion - Summary and key takeaways?

The European market is poised for robust expansion, moving from €5.01 billion in 2026 to €10.63 billion by 2033. Drivers such as regulatory pressure, sustainability mandates, and technological innovation outweigh existing restraints. Competitive dynamics favor firms that combine strong R&D with strategic partnerships. Stakeholders should focus on emerging seed‑treatment bio‑products and digital integration to capture the next phase of market growth.

Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, integrating primary interviews with industry experts, secondary data from company reports, EU regulatory publications, and market databases. Quantitative analysis used compound annual growth rate (CAGR) calculations based on the provided market size figures. Qualitative insights were derived from trend mapping, competitive benchmarking, and value‑chain assessments to ensure a comprehensive market view.

Research Scope - Coverage and limitations?

The scope covers the European agricultural biologicals sector, addressing product types, sources, applications, and application modes. Geographic analysis is limited to the European region, with global context referenced only to highlight Europe’s relative size. The study does not provide granular market share percentages beyond the aggregate figures supplied, and it refrains from estimating undisclosed regional or segment-specific financial metrics.

Key Companies and Recent Developments in the Europe Agricultural Biologicals Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent activity includes BASF SE launching a microbially‑enhanced seed coating for wheat, Syngenta forming a partnership with a digital agronomy platform to optimize bio‑pesticide application, DowDuPont Inc. introducing a new bio‑fertilizer line targeting nitrogen fixation in legumes, and UPL acquiring a niche European biotech firm to broaden its microbial portfolio. Valent BioSciences LLC announced a joint venture with a European university to develop next‑generation biostimulants. Biolchim, Isagro, and Koppert continue to expand distribution networks and release region‑specific bio‑product formulations.