What is the Europe Emergency Shutdown Systems Market Overview – definition, scope, and significance?

The Europe Emergency Shutdown Systems (ESS) market comprises hardware and software solutions that automatically halt hazardous processes in industrial facilities to protect personnel, equipment, and the environment. Scope includes components such as switches, sensors, programmable safety systems, safety valves, and actuators, deployed across control methods—pneumatic, electrical, fiber optic, and hydraulic. The market is significant because it underpins safety compliance for high‑risk sectors like oil & gas, refining, power generation, and chemicals, thereby reducing downtime and insurance costs while supporting stringent EU safety regulations.

What are the Europe Emergency Shutdown Systems Market drivers, restraints, challenges, and opportunities?

Key drivers include rising safety legislation, increasing capital expenditure on plant modernization, and growing awareness of occupational risk. Restraints stem from high upfront costs of advanced ESS hardware and integration complexity. Challenges involve maintaining system reliability amid aging infrastructure and addressing skill gaps in operating sophisticated control technologies. Opportunities arise from digital transformation—especially the adoption of fiber‑optic communication for faster response times—and from green‑energy projects that demand robust shutdown capabilities to protect emerging renewable assets.

What are the Europe Emergency Shutdown Systems Market growth trends?

Current trends show a shift toward smart, network‑enabled ESS that leverage IoT sensors for predictive diagnostics. Manufacturers are expanding modular product lines that can be retrofitted into existing plants, facilitating cost‑effective upgrades. The market is also seeing increased demand for fiber‑optic control methods due to their immunity to electromagnetic interference, which is crucial in high‑voltage environments such as power generation. Additionally, sustainability initiatives are prompting integration of ESS with overall plant safety management systems.

How has COVID‑19 impacted the Europe Emergency Shutdown Systems Market?

The pandemic initially slowed new ESS installations because of project delays and restricted site access. However, heightened focus on operational resilience accelerated demand for remote monitoring and automated shutdown capabilities. Recovery has been steady, with many operators prioritizing safety upgrades as part of post‑COVID rejuvenation plans, helping the market regain momentum and aligning with the projected CAGR of 6.45%.

What does the Europe Emergency Shutdown Systems Market competitive landscape look like?

The competitive arena is highly consolidated, featuring global industrial giants such as ABB Ltd., Siemens AG, and Schneider Electric SE, alongside specialist safety providers like Yokogawa Electric Corporation and OMRON Corporation. Companies compete on technology breadth—covering pneumatic to fiber‑optic solutions—and integrated service offerings. Recent consolidation trends include strategic acquisitions aimed at expanding product portfolios and geographic reach, reinforcing the market’s competitive intensity.

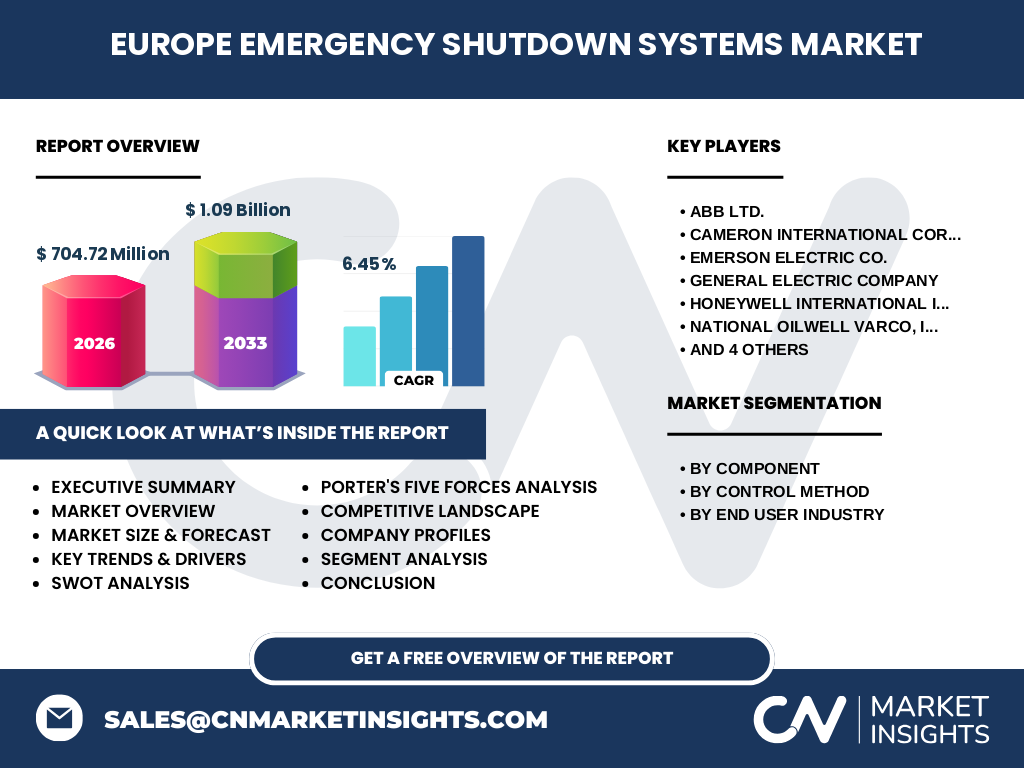

What are the key findings in the Executive Summary of the Europe Emergency Shutdown Systems Market?

The market is valued at €704.72 million in 2026 and is projected to reach €1.09 billion by 2033, reflecting a robust 6.45% CAGR. Growth is propelled by stringent EU safety directives, digitalization, and expanding end‑use sectors, particularly oil & gas and power generation. Competitive dynamics are characterized by a few dominant players offering comprehensive portfolios across components and control methods. Investment opportunities focus on advanced fiber‑optic technologies and modular retrofits.

What is the Europe Emergency Shutdown Systems Market forecast for 2025‑2032?

Building on the base year 2026 valuation of €704.72 million, the market is expected to sustain a compound annual growth rate of 6.45% through 2033, culminating in an estimated €1.09 billion. This trajectory implies steady incremental growth each year, driven by ongoing regulatory enforcement and the progressive adoption of intelligent shutdown solutions across core industries.

How is the Europe Emergency Shutdown Systems Market sized and shared by segmentation?

By component, the market is divided among switches, sensors, programmable safety systems, safety valves, and actuators, each serving distinct safety functions. By control method, the segmentation includes pneumatic, electrical, fiber‑optic, and hydraulic technologies, catering to varied industry preferences for speed, reliability, and environmental resistance. By end‑user industry, the primary segments are oil & gas, refining, power generation, and chemical processing, reflecting the sectors with the highest safety risk profiles.

What is the global Europe Emergency Shutdown Systems Market size and share by region?

Within the global landscape, Europe accounts for a substantial share, anchored by mature industrial bases and rigorous safety standards. While specific regional percentages are not disclosed, the market’s €704.72 million valuation in 2026 underscores Europe’s pivotal role in the worldwide ESS ecosystem, with growth expectations aligning with the overall global expansion trend.

What does the regional analysis of the Europe Emergency Shutdown Systems Market reveal?

Regional performance varies across Western, Northern, and Central Europe, with strong demand in countries hosting major oil & gas complexes and power plants. Nations with robust renewable energy projects are also increasing ESS adoption to safeguard new assets. The analysis highlights that regions with higher capital investment in plant upgrades tend to exhibit faster adoption rates of advanced control methods such as fiber‑optic systems.

Which companies lead the Europe Emergency Shutdown Systems Market and what are their strategies?

Leading firms include ABB Ltd., Cameron International Corporation, Emerson Electric Co., General Electric Company, Honeywell International Inc., National Oilwell Varco, Inc., OMRON Corporation, Schneider Electric SE, Siemens AG, and Yokogawa Electric Corporation. Their strategies focus on expanding digital safety platforms, forging partnerships with EPC contractors, and investing in R&D for fiber‑optic and IoT‑enabled shutdown solutions. Many are also pursuing service‑oriented business models to offer lifecycle support and remote diagnostics.

How does Porter’s Five Forces analysis apply to the Europe Emergency Shutdown Systems Market?

Threat of new entrants is moderate due to high technology barriers and certification requirements. Bargaining power of suppliers is low to moderate, as component manufacturers are numerous, though specialized sensor suppliers hold niche influence. Bargaining power of buyers is moderate, with large industrial operators demanding customized solutions. Threat of substitutes is low, given the critical safety function of ESS. Industry rivalry is high, driven by a handful of large, well‑capitalized competitors offering integrated portfolios.

What are the SWOT insights for the Europe Emergency Shutdown Systems Market?

Strengths: Strong regulatory framework, high safety awareness, and presence of technology leaders. Weaknesses: Capital‑intensive upgrades and fragmented legacy systems. Opportunities: Growth of fiber‑optic control, digital twins for safety simulation, and expansion into renewable energy facilities. Threats: Economic downturns limiting CAPEX and potential cyber‑security risks associated with increased connectivity.

How is the Europe Emergency Shutdown Systems Market value chain structured?

The value chain begins with raw material suppliers for metallic components, progresses to component manufacturers (switches, sensors, valves, actuators), then to system integrators who assemble programmable safety systems and configure control methods. Distributors and system integrators sell to end‑users, while after‑sales service providers deliver maintenance, testing, and compliance certification, completing the loop.

What key investment insights can be drawn for the Europe Emergency Shutdown Systems Market?

Investors should target companies with strong R&D pipelines in fiber‑optic and IoT‑enabled ESS, as these technologies are poised for rapid adoption. Acquisitions of niche sensor firms can accelerate portfolio breadth. Additionally, funding projects that retrofit legacy plants with modular shutdown modules offers a near‑term revenue stream, while participation in green‑energy safety initiatives positions investors for long‑term growth.

What conclusions can be drawn about the Europe Emergency Shutdown Systems Market?

The market demonstrates robust growth, driven by regulatory pressure, digital transformation, and sector‑wide safety imperatives. With a projected rise to €1.09 billion by 2033 and a healthy 6.45% CAGR, the outlook remains positive. Success will hinge on adopting advanced control methods, addressing integration challenges, and capitalizing on the expanding renewable energy landscape.

What research methodology was used for this market analysis?

The study employed a mix of primary interviews with industry experts, secondary data collection from company reports, regulatory publications, and reputable databases. Quantitative data were validated through cross‑checking multiple sources, while qualitative insights were derived from trend analysis and expert opinion to ensure a comprehensive view of the market dynamics.

What is the scope of this research and its limitations?

The scope covers the Europe Emergency Shutdown Systems market by component, control method, and end‑user industry, focusing on the period 2026‑2033. It includes competitive profiling and strategic assessments. Limitations stem from the proprietary nature of some financial figures, which restricts detailed regional market share disclosure beyond the aggregate European valuation.

Which key companies have recent developments in the Europe Emergency Shutdown Systems Market?

Recent activities include ABB Ltd. launching a new fiber‑optic ESS platform, Siemens AG announcing a partnership with major oil refiners for retrofitting legacy plants, and Honeywell International Inc. unveiling an AI‑driven predictive maintenance module for safety valves. Schneider Electric SE has introduced a modular safety system designed for renewable energy sites, while Yokogawa Electric Corporation released updated programmable safety controllers with enhanced cybersecurity features.