Micro Data Center Market Overview - Definition, scope, and significance

A micro data center is a compact, modular system that provides data center capabilities in a smaller footprint, typically ranging from 1 to 10 racks. These systems integrate servers, storage, networking equipment, and power distribution into a single, self-contained unit that can be deployed in remote locations, edge computing environments, or areas with limited space. The significance of micro data centers lies in their ability to bring computing power closer to end-users and data sources, reducing latency and enabling real-time data processing. They serve as critical infrastructure for supporting emerging technologies such as IoT, 5G networks, and edge computing applications, while offering enhanced security, energy efficiency, and simplified deployment compared to traditional data centers.

Micro Data Center Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The micro data center market is primarily driven by the exponential growth of data generation from IoT devices, the need for edge computing solutions, and the increasing adoption of 5G networks. Organizations across various sectors are seeking to reduce latency and improve data processing capabilities at the network edge, which fuels demand for these compact solutions. Additionally, the growing trend of digital transformation and the need for disaster recovery solutions contribute to market growth. However, the market faces restraints such as high initial costs and concerns about security vulnerabilities in distributed computing environments. Challenges include managing heat dissipation in compact spaces and ensuring seamless integration with existing IT infrastructure. Despite these obstacles, significant opportunities exist in emerging markets, particularly in developing regions where traditional data center infrastructure may be limited or cost-prohibitive.

Micro Data Center Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the micro data center market are characterized by increasing adoption of modular and prefabricated solutions, which offer faster deployment times and reduced operational costs. The market is witnessing a shift towards more energy-efficient designs, incorporating advanced cooling technologies and renewable energy sources to address environmental concerns. Another significant trend is the integration of artificial intelligence and machine learning capabilities for predictive maintenance and optimization of data center operations. The rise of hybrid cloud architectures is also driving demand for micro data centers as organizations seek to balance on-premises and cloud-based resources. Additionally, the COVID-19 pandemic has accelerated the need for distributed IT infrastructure, further boosting the market for micro data centers as businesses adapt to remote work models and distributed operations.

COVID-19 Impact on the Micro Data Center Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic has had a profound impact on the micro data center market, initially causing disruptions in supply chains and delaying some projects due to lockdowns and travel restrictions. However, the crisis also highlighted the critical importance of robust and distributed IT infrastructure, leading to an accelerated adoption of micro data centers. The sudden shift to remote work models and increased reliance on digital services created an urgent need for edge computing solutions to support distributed workforces and ensure business continuity. This trend has resulted in a surge in demand for micro data centers, particularly in sectors such as healthcare, education, and e-commerce. As the world recovers from the pandemic, the market is expected to continue its growth trajectory, with organizations prioritizing investments in resilient and flexible IT infrastructure to prepare for future disruptions.

Micro Data Center Market Competitive Landscape - Major competitors and market consolidation

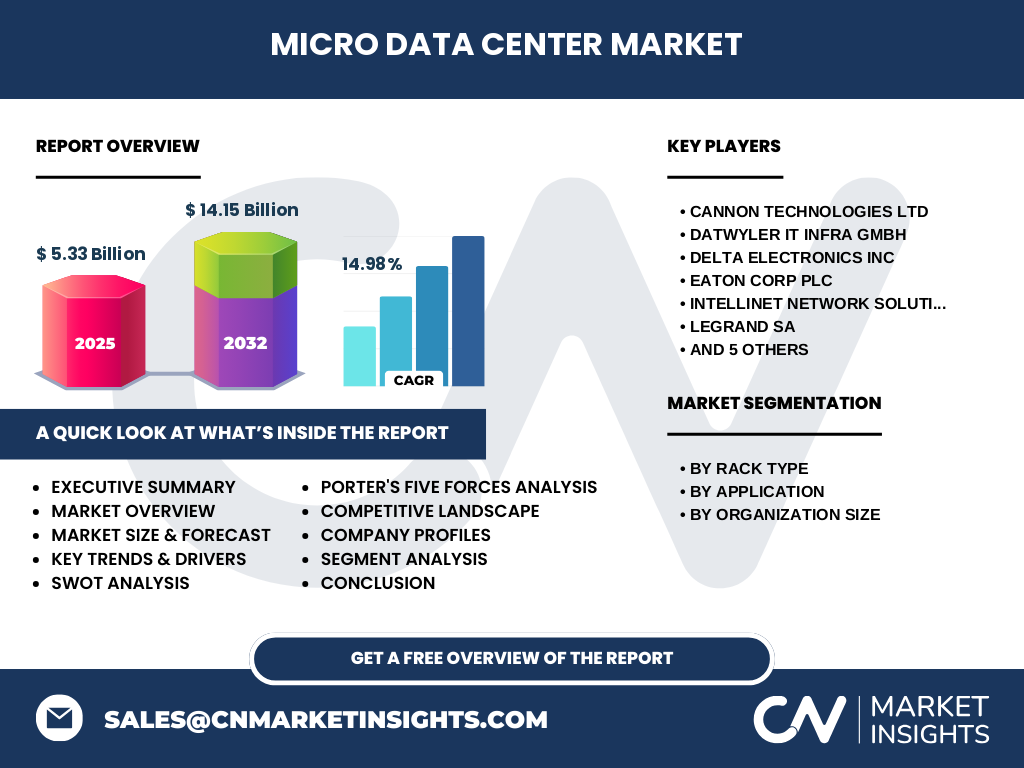

The micro data center market features a diverse competitive landscape with a mix of established IT infrastructure providers and specialized edge computing companies. Key players include Cannon Technologies Ltd, Datwyler IT Infra GmbH, Delta Electronics Inc, Eaton Corp Plc, Intellinet Network Solutions, Legrand SA, Panduit, Rittal GmbH & Co KG, SCHÄFER Ausstattungssysteme GmbH, Schneider Electric SE, and Vertiv Group Corp. These companies are competing on factors such as product innovation, energy efficiency, scalability, and integration capabilities. The market is witnessing increased consolidation as larger players acquire smaller, specialized firms to expand their product portfolios and gain technological advantages. Strategic partnerships and collaborations are also becoming more common, particularly between hardware manufacturers and software providers, to offer comprehensive edge computing solutions. This competitive environment is driving rapid innovation and pushing companies to differentiate themselves through unique value propositions and customer-centric approaches.

Executive Summary - High-level overview and key findings about Micro Data Center Market

The micro data center market is experiencing robust growth, driven by the increasing demand for edge computing solutions and the need for distributed IT infrastructure. With a market size of 5.33 Billion in 2025 and projected to reach 14.15 Billion by 2032, growing at a CAGR of 14.98%, the market presents significant opportunities for stakeholders. Key trends include the adoption of modular and energy-efficient designs, integration of AI and ML capabilities, and the rise of hybrid cloud architectures. The market is segmented by rack type (single rack and multi-rack), application (IT and telecom, BFSI, retail, healthcare, manufacturing), and organization size (large enterprises and SMEs). Despite challenges such as high initial costs and security concerns, the market's growth is supported by the increasing importance of low-latency computing and the expansion of 5G networks. The competitive landscape is characterized by a mix of established players and innovative startups, with consolidation and strategic partnerships shaping the industry's evolution.

Micro Data Center Market Forecast - Projections for 2025-2032 period

The micro data center market is poised for substantial growth over the forecast period from 2025 to 2032, with projections indicating a market size increase from 5.33 Billion to 14.15 Billion. This growth represents a compound annual growth rate (CAGR) of 14.98%, reflecting the increasing demand for edge computing solutions and distributed IT infrastructure. The forecast period is expected to see accelerated adoption across various industry verticals, particularly in sectors such as IT and telecom, BFSI, retail, healthcare, and manufacturing. The growth will be driven by factors such as the proliferation of IoT devices, the rollout of 5G networks, and the need for real-time data processing capabilities. Additionally, advancements in cooling technologies, energy efficiency, and modular designs are likely to further fuel market expansion. The forecast also suggests that emerging markets in developing regions will play a significant role in driving growth, as organizations in these areas seek cost-effective and scalable IT infrastructure solutions.

Micro Data Center Market Size and Share by Segmentation - Breakdown by {segmentData}

The micro data center market is segmented based on rack type, application, and organization size. In terms of rack type, the market is divided into single rack and multi-rack configurations, with the single rack segment currently dominating due to its suitability for small to medium-sized deployments and edge computing applications. By application, the IT and telecom sector holds a significant share, driven by the need for low-latency processing and 5G network support. The BFSI sector is also a major contributor, leveraging micro data centers for enhanced security and real-time transaction processing. In the retail sector, micro data centers are increasingly used to support IoT devices and enable personalized customer experiences. The healthcare industry is adopting these solutions for telemedicine and remote patient monitoring applications. By organization size, large enterprises currently account for a larger share due to their greater IT infrastructure needs, but the SME segment is expected to grow rapidly as costs decrease and awareness increases.

Global Micro Data Center Market Size and Share by Region - Geographic distribution

The global micro data center market exhibits varying levels of adoption and growth across different regions. North America currently holds the largest market share, driven by the presence of major technology companies, early adoption of edge computing technologies, and significant investments in 5G infrastructure. Europe follows closely, with countries like Germany, the UK, and France leading the adoption of micro data centers, particularly in industrial and manufacturing applications. The Asia-Pacific region is expected to witness the highest growth rate during the forecast period, fueled by rapid digitalization, increasing IoT deployments, and government initiatives to promote smart city development. Countries such as China, Japan, and India are at the forefront of this growth, with expanding telecom networks and a large base of SMEs driving demand. Latin America and the Middle East & Africa regions are also showing promising growth, albeit from a smaller base, as organizations in these areas increasingly recognize the benefits of distributed IT infrastructure.

Regional Analysis of the Micro Data Center Market - Detailed regional market performance

The micro data center market demonstrates distinct characteristics and growth patterns across different regions. In North America, the market is characterized by high adoption rates, particularly in the United States, where major tech hubs and early technology adopters drive demand. The region benefits from advanced telecommunications infrastructure and significant investments in edge computing technologies. Europe shows strong growth, with countries like Germany leading in industrial applications and the UK focusing on financial services and smart city initiatives. The Asia-Pacific region presents a diverse landscape, with China rapidly deploying micro data centers to support its massive IoT ecosystem and 5G rollout, while Japan focuses on advanced manufacturing and robotics applications. India's market is driven by its booming IT sector and government initiatives for digital transformation. In Latin America, Brazil and Mexico are key markets, with growth driven by the retail and manufacturing sectors. The Middle East & Africa region, particularly the Gulf Cooperation Council (GCC) countries, are investing heavily in micro data centers to support their smart city projects and diversify their economies beyond oil.

Leading Company Profiles in the Micro Data Center Market - Industry players and strategies

The micro data center market features several key players, each with distinct strategies and strengths. Cannon Technologies Ltd is known for its innovative modular solutions and focus on energy efficiency. Datwyler IT Infra GmbH specializes in comprehensive infrastructure solutions, offering integrated systems for various applications. Delta Electronics Inc leverages its expertise in power management and thermal solutions to provide efficient micro data center designs. Eaton Corp Plc brings its extensive experience in power distribution and backup systems to the market, focusing on reliability and scalability. Intellinet Network Solutions differentiates itself through its networking expertise and tailored solutions for specific industry needs. Legrand SA offers a wide range of enclosure and cable management solutions, emphasizing flexibility and ease of deployment. Panduit is recognized for its high-quality connectivity solutions and comprehensive product portfolio. Rittal GmbH & Co KG is known for its modular enclosure systems and advanced cooling technologies. SCHÄFER Ausstattungssysteme GmbH specializes in customized solutions for industrial applications. Schneider Electric SE leverages its global presence and comprehensive energy management solutions to offer integrated micro data center systems. Vertiv Group Corp focuses on critical infrastructure technologies, providing end-to-end solutions for edge computing environments.

Porter's Five Forces Analysis of the Micro Data Center Market - Competitive forces assessment

Porter's Five Forces analysis provides insights into the competitive dynamics of the micro data center market. The threat of new entrants is moderate, as the market requires significant technical expertise and capital investment, but the growing demand and technological advancements are attracting new players. The bargaining power of buyers is increasing as they become more knowledgeable about micro data center solutions and demand customized offerings. Suppliers have moderate bargaining power due to the specialized nature of components required for micro data centers, but the presence of multiple suppliers helps balance this power. The threat of substitutes is relatively low, as micro data centers offer unique advantages in terms of edge computing and distributed infrastructure that are difficult to replicate with alternative solutions. Competitive rivalry is intense, with numerous players competing on factors such as price, performance, energy efficiency, and integration capabilities. The market is also witnessing increased collaboration between hardware manufacturers and software providers, further intensifying the competitive landscape.

SWOT Analysis of the Micro Data Center Market - Strengths, weaknesses, opportunities, threats

The micro data center market exhibits several strengths, including its ability to provide low-latency computing, support for edge applications, and flexibility in deployment. These solutions offer significant advantages in terms of energy efficiency and reduced operational costs compared to traditional data centers. However, the market also faces weaknesses such as high initial costs and concerns about security in distributed environments. Opportunities for growth are abundant, particularly in emerging markets, the expansion of 5G networks, and the increasing adoption of IoT devices. The market can also capitalize on the growing trend of hybrid cloud architectures and the need for disaster recovery solutions. Threats to the market include rapid technological changes that may render current solutions obsolete, potential regulatory challenges related to data privacy and security, and the risk of market saturation as more players enter the field. Additionally, economic uncertainties and supply chain disruptions could pose challenges to market growth.

Micro Data Center Market Value Chain Analysis - Industry structure and value flow

The micro data center market value chain encompasses several key stages, from component manufacturing to end-user deployment and support. At the beginning of the chain, raw material suppliers provide essential components such as semiconductors, metals, and plastics used in the construction of micro data center systems. Component manufacturers then produce specialized parts, including servers, storage devices, networking equipment, and power distribution units. System integrators combine these components into complete micro data center solutions, often customizing them to meet specific customer requirements. Distributors and resellers play a crucial role in bringing these solutions to market, providing local support and expertise. At the end of the value chain, end-users across various industries deploy and operate micro data centers to support their edge computing and distributed IT infrastructure needs. Throughout the chain, service providers offer consulting, installation, maintenance, and managed services to ensure optimal performance and support for micro data center deployments.

Key Investment Insights in the Micro Data Center Market - Strategic investment recommendations

Investors looking to capitalize on the growing micro data center market should consider several key insights and strategic recommendations. First, focus on companies that are developing innovative cooling technologies and energy-efficient solutions, as these factors are becoming increasingly important in the market. Second, invest in firms that are expanding their presence in emerging markets, particularly in the Asia-Pacific region, where rapid digitalization and 5G rollout are driving demand. Third, look for companies that are forming strategic partnerships and collaborations to offer comprehensive edge computing solutions, as this trend is likely to shape the future of the market. Additionally, consider investments in firms that are integrating artificial intelligence and machine learning capabilities into their micro data center offerings, as these technologies are expected to play a crucial role in optimizing operations and maintenance. Finally, keep an eye on companies that are developing modular and scalable solutions, as the ability to easily expand and adapt to changing needs will be a key differentiator in the market.

Micro Data Center Market Conclusion - Summary and key takeaways

The micro data center market is experiencing significant growth, driven by the increasing demand for edge computing solutions and distributed IT infrastructure. With a projected market size of 14.15 Billion by 2032, growing at a CAGR of 14.98%, the market presents substantial opportunities for stakeholders across the value chain. Key trends shaping the market include the adoption of modular and energy-efficient designs, integration of AI and ML capabilities, and the rise of hybrid cloud architectures. The market is segmented by rack type, application, and organization size, with the IT and telecom sector and large enterprises currently dominating. However, the SME segment is expected to grow rapidly as costs decrease and awareness increases. Despite challenges such as high initial costs and security concerns, the market's growth is supported by the increasing importance of low-latency computing and the expansion of 5G networks. The competitive landscape is characterized by a mix of established players and innovative startups, with consolidation and strategic partnerships shaping the industry's evolution.

Research Methodology - How this research was conducted

This comprehensive market research on the micro data center market was conducted using a combination of primary and secondary research methodologies. Primary research involved interviews with industry experts, including executives from leading micro data center manufacturers, technology providers, and end-users across various sectors. These interviews provided valuable insights into market trends, challenges, and future outlook. Secondary research encompassed a thorough analysis of company annual reports, financial statements, press releases, and industry publications. Additionally, data from reputable market research firms, government publications, and industry associations were reviewed to validate findings and gather statistical information. The research also included a detailed analysis of patent filings, product launches, and strategic partnerships in the micro data center space. Market size and growth projections were derived using a combination of top-down and bottom-up approaches, considering factors such as technological advancements, industry adoption rates, and macroeconomic trends. The research methodology ensured a comprehensive and accurate representation of the micro data center market landscape.

Research Scope - Coverage and limitations

The research scope for this micro data center market analysis covers the period from 2025 to 2032, with a particular focus on the current market size of 5.33 Billion and the projected growth to 14.15 Billion by 2032. The study encompasses a detailed analysis of market segments, including rack type (single rack and multi-rack), application (IT and telecom, BFSI, retail, healthcare, manufacturing), and organization size (large enterprises and SMEs). The research also provides a comprehensive regional analysis, covering key markets in North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The scope includes an in-depth examination of the competitive landscape, featuring profiles of major players such as Cannon Technologies Ltd, Datwyler IT Infra GmbH, Delta Electronics Inc, Eaton Corp Plc, Intellinet Network Solutions, Legrand SA, Panduit, Rittal GmbH & Co KG, SCHÄFER Ausstattungssysteme GmbH, Schneider Electric SE, and Vertiv Group Corp. The research also covers key market dynamics, including drivers, restraints, challenges, and opportunities. Limitations of the study include the exclusion of certain niche applications and emerging technologies that may impact the market in the long term, as well as potential variations in regional data availability and accuracy.

Key Companies and Recent Developments in the Micro Data Center Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The micro data center market is characterized by active innovation and strategic developments among key players. Schneider Electric SE recently announced the launch of its EcoStruxure Micro Data Center, featuring integrated power, cooling, and management capabilities designed for edge computing applications. Vertiv Group Corp has expanded its portfolio with the introduction of the SmartRow DCR, a modular data center solution that combines cooling, power, and IT equipment in a single enclosure. Eaton Corp Plc has formed a strategic partnership with a leading cloud service provider to develop edge computing solutions for industrial IoT applications. Rittal GmbH & Co KG unveiled its new VX25 large enclosure system, offering enhanced flexibility and scalability for micro data center deployments. Legrand SA has acquired a specialized edge computing startup to strengthen its position in the micro data center market. Delta Electronics Inc has launched a new series of high-efficiency power supplies specifically designed for micro data center applications. These developments highlight the industry's focus on innovation, strategic partnerships, and the integration of advanced technologies to meet the growing demand for edge computing solutions.