What is the Asia Pacific Dairy Starter Culture Market Overview – Definition, scope, and significance?

The Asia Pacific Dairy Starter Culture market comprises microbial preparations used to initiate and control fermentation in dairy products such as yogurt, cheese, buttermilk, sour cream, and ripened butter. These cultures are classified by type (mesophilic or thermophilic bacteria), nature (single‑strain or multi‑strain), and function (acid or flavor production). The market’s significance lies in its role in enhancing product safety, texture, flavor, and nutritional value, thereby supporting the rapid growth of the region’s dairy processing industry and meeting rising consumer demand for functional and premium dairy foods.

What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Dairy Starter Culture Market?

Key drivers include increasing dairy consumption, rising disposable incomes, and a growing preference for probiotic‑rich products. Urbanization and the expansion of modern retail channels further stimulate demand for value‑added dairy items that rely on starter cultures. Restraints stem from stringent regulatory requirements and high production costs for patented strains. Challenges involve supply‑chain volatility for raw materials and the need for continuous innovation to address lactose intolerance trends. Opportunities arise from the development of specialty cultures for non‑dairy alternatives, clean‑label formulations, and export potential to emerging markets within the region.

What are the current growth trends in the Asia Pacific Dairy Starter Culture Market?

Current trends feature a shift toward multi‑strain, thermophilic cultures that deliver faster fermentation and improved flavor stability. Manufacturers are increasingly investing in research to create strains with enhanced probiotic benefits and stress tolerance. There is also a notable trend of integrating biotechnology platforms to accelerate strain development. Additionally, the market is witnessing consolidation as large ingredient companies acquire niche culture producers to broaden their product portfolios and geographic reach.

How has COVID‑19 impacted the Asia Pacific Dairy Starter Culture Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and slowed new product launches due to lockdowns and reduced food‑service demand. However, heightened consumer focus on health and immunity boosted demand for functional dairy products, accelerating adoption of probiotic cultures. As economies recover, the market is experiencing a rebound in commercial dairy processing volumes, with a clear trajectory toward robust growth driven by renewed investment in product innovation and capacity expansion.

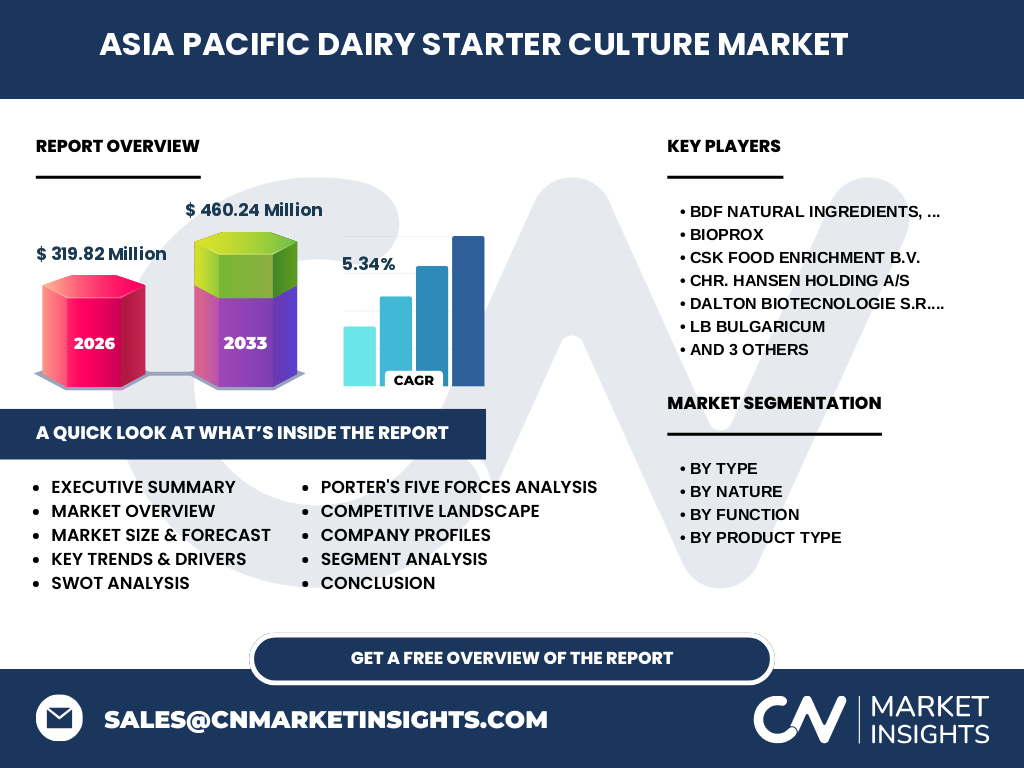

What does the competitive landscape of the Asia Pacific Dairy Starter Culture Market look like?

The market is dominated by a mix of global ingredient giants and specialized regional players. Companies such as Chr. Hansen Holding A/S, Lallemand Inc., and The Dow Chemical Company (Dupont) lead with extensive strain libraries and strong distribution networks. Regional firms like BDF Natural Ingredients, Bioprox, and LB Bulgaricum provide localized solutions and niche products. Competitive dynamics are shaped by mergers, strategic partnerships, and the continuous launch of novel culture blends to meet divergent consumer preferences.

What are the high‑level insights presented in the Executive Summary?

The Asia Pacific Dairy Starter Culture market is valued at US$319.82 million in 2026 and is projected to reach US$460.24 million by 2033, reflecting a CAGR of 5.34 % over the forecast horizon. Growth is propelled by expanding dairy consumption, premiumization, and the rise of probiotic‑focused products. The market’s segmentation across type, nature, function, and product category underscores diverse application opportunities. Competitive pressure is intensifying, with major players leveraging R&D, acquisitions, and strategic alliances to capture market share.

What are the forecast expectations for the Asia Pacific Dairy Starter Culture Market from 2025 to 2032?

Based on the provided CAGR of 5.34 %, the market is expected to sustain steady expansion through 2032, maintaining momentum from the 2026 baseline of US$319.82 million. The forecast indicates that demand will be driven by continued product innovation in yogurt, cheese, and emerging dairy formats, alongside the growing incorporation of starter cultures in functional and fortified dairy offerings across the region.

How is the market sized and shared by segmentation?

Segmentation by type distinguishes mesophilic bacteria, which thrive at moderate temperatures and are suited for traditional cheeses and buttermilk, from thermophilic bacteria, preferred for high‑temperature processes such as yogurt and certain cheeses. By nature, single‑strain cultures offer precise control, while multi‑strain blends provide synergistic benefits for flavor and texture. Functionally, acid‑producing cultures are essential for coagulation and shelf‑life, whereas flavor‑producing strains enhance sensory attributes. Product‑type segmentation captures the breadth of applications, from yogurt and cheese to buttermilk and sour cream, each contributing to the overall market size.

What is the geographic distribution of the Asia Pacific Dairy Starter Culture market?

The market spans key sub‑regions including East Asia, Southeast Asia, South Asia, and Oceania. While specific monetary shares are not disclosed, the distribution reflects strong demand in dairy‑intensive economies such as China, Japan, South Korea, Australia, and India, complemented by emerging opportunities in Vietnam, Thailand, and the Philippines where dairy consumption is on the rise.

What are the detailed regional performance insights for the Asia Pacific Dairy Starter Culture market?

East Asia leads in volume due to mature dairy processing infrastructures and high per‑capita consumption of yogurt and cheese. South Asia shows rapid growth driven by expanding urban populations and increasing consumer awareness of health benefits associated with fermented dairy. Southeast Asia’s market is propelled by the entry of multinational dairy brands and rising middle‑class purchasing power. Oceania, particularly Australia and New Zealand, contributes stable demand, supported by sophisticated supply chains and premium product development.

Which companies are leading in the Asia Pacific Dairy Starter Culture market and what are their strategies?

Chr. Hansen focuses on expanding its probiotic portfolio and leveraging advanced genomics for strain improvement. Lallemand emphasizes sustainable production practices and strategic acquisitions to broaden its culture range. The Dow Chemical (Dupont) integrates starter cultures within its broader food‑ingredient ecosystem, targeting cross‑selling opportunities. Regional leaders like BDF Natural Ingredients and Bioprox concentrate on cost‑effective, locally tailored cultures, while companies such as CSK Food Enrichment and Dalton Biotecnologie prioritize niche specialty strains for high‑value dairy segments.

How does Porter’s Five Forces analysis apply to the Asia Pacific Dairy Starter Culture market?

Threat of new entrants is moderate; high R&D costs and regulatory hurdles limit easy entry. Bargaining power of suppliers is low to moderate, as raw material inputs are relatively commoditized, though specialized fermentation media can command premium pricing. Bargaining power of buyers is growing, with large dairy processors demanding customized cultures and competitive pricing. Threat of substitutes is low, given the unique microbial functionality required for dairy fermentation. Industry rivalry is intense, driven by product differentiation, patent portfolios, and strategic collaborations.

What are the SWOT highlights for the Asia Pacific Dairy Starter Culture market?

Strengths: Robust demand for fermented dairy, strong scientific expertise, and diversified application base. Weaknesses: High development costs and dependence on regulatory approvals. Opportunities: Expansion into plant‑based dairy analogues, development of health‑focused probiotic strains, and increased export potential. Threats: Stringent food safety regulations, volatility in raw material pricing, and competitive pressure from biotech startups.

What does the value chain of the Asia Pacific Dairy Starter Culture market look like?

The value chain starts with strain discovery and R&D, followed by pilot‑scale fermentation and scale‑up production. Next, cultures are formulated into stable preparations (freeze‑dry or liquid) and packaged for distribution. Distributors supply to dairy processors, who integrate the cultures into product manufacturing. Post‑production, quality assurance, traceability, and regulatory compliance ensure market entry. Supporting services include technical consultancy, strain customization, and after‑sales support.

What key investment insights can be drawn for the Asia Pacific Dairy Starter Culture market?

Investors should target companies with strong IP portfolios and proven capabilities in multi‑strain development, as these assets drive differentiation. Given the projected CAGR of 5.34 %, capital allocation toward capacity expansion and bio‑technology platforms presents attractive returns. Partnerships with dairy processors and entry into fast‑growing markets such as Southeast Asia can accelerate revenue growth. Monitoring regulatory changes and sustainability trends will also be critical for risk mitigation.

What are the concluding takeaways for the Asia Pacific Dairy Starter Culture market?

The market is on a clear growth trajectory, underpinned by rising dairy consumption and a shift toward health‑oriented products. With a forecasted market size of US$460.24 million by 2033 and a steady CAGR, opportunities exist across product innovation, regional expansion, and strategic consolidation. Companies that invest in advanced strain technology and align with consumer health trends are positioned to capture the most value.

How was the research methodology designed for this market report?

The study employed a mixed‑method approach, combining primary interviews with industry experts, secondary data extraction from company filings, trade publications, and market databases, and quantitative forecasting using the provided CAGR of 5.34 %. Validation steps included cross‑checking of primary insights with secondary sources and scenario analysis to ensure robustness of the forecast horizon.

What is the scope of this research and its coverage limitations?

The research covers the Asia Pacific region, focusing on starter cultures used in dairy applications and segmented by type, nature, function, and product category. It excludes non‑dairy fermented products and does not provide granular country‑level revenue figures beyond the regional overview. The analysis is confined to the data points supplied, avoiding speculative financial estimations.

Which key companies and recent developments are highlighted in the Asia Pacific Dairy Starter Culture market?

Key players include BDF Natural Ingredients, Bioprox, CSK Food Enrichment B.V., Chr. Hansen Holding A/S, Dalton Biotecnologie S.R.L., LB Bulgaricum, Lallemand Inc., Saccco System, and The Dow Chemical Company (Dupont). Recent developments feature Chr. Hansen’s launch of a new thermophilic multi‑strain blend for high‑temperature yogurt processing, Lallemand’s acquisition of a boutique probiotic culture firm to broaden its functional portfolio, and Dupont’s partnership with a major dairy consortium in Southeast Asia to co‑develop clean‑label starter solutions.