What is the definition, scope, and significance of the E‑Invoicing Market?

E‑Invoicing refers to the electronic generation, transmission, and processing of invoices between businesses, government entities, and consumers without paper. The market encompasses solutions for non‑PO and PO invoices, deployed on‑premise or via cloud, and applied across B2B, B2C, and B2G transactions. Its significance lies in accelerating cash‑flow cycles, reducing manual errors, cutting compliance costs, and supporting digital transformation initiatives that are increasingly mandated by tax authorities worldwide.

What are the main drivers, restraints, challenges, and opportunities shaping the E‑Invoicing Market?

Key drivers include mandatory e‑invoicing regulations, growing demand for automation in retail, BFSI, IT, and telecom sectors, and the cost‑efficiency benefits of cloud‑based platforms. Restraints arise from legacy ERP integrations, data‑security concerns, and varying regional compliance standards. Challenges involve change‑management resistance and the need for skilled talent to implement complex workflows. Opportunities are found in expanding B2C and B2G use cases, AI‑enhanced invoice analytics, and cross‑border invoicing standardisation.

Which current and emerging trends are influencing the growth of the E‑Invoicing Market?

Current trends feature a shift toward cloud‑native invoicing, real‑time invoice validation, and integration with ERP and procurement suites. Emerging trends include the adoption of blockchain for invoice authenticity, machine‑learning driven fraud detection, and the rise of API‑first platforms that enable seamless ecosystem connectivity. Additionally, the convergence of e‑invoicing with broader finance‑as‑a‑service offerings is gaining momentum.

How did COVID‑19 affect the E‑Invoicing Market and what is the recovery trajectory?

The pandemic accelerated digital adoption as businesses sought remote processing capabilities. Companies rapidly migrated from paper‑based billing to electronic solutions to maintain cash flow and comply with tightened fiscal deadlines. Post‑COVID, the market retained its momentum, with organisations continuing to invest in scalable cloud platforms to future‑proof operations, leading to a robust recovery and sustained growth trajectory.

Who are the major competitors in the E‑Invoicing Market and what does the competitive landscape look like?

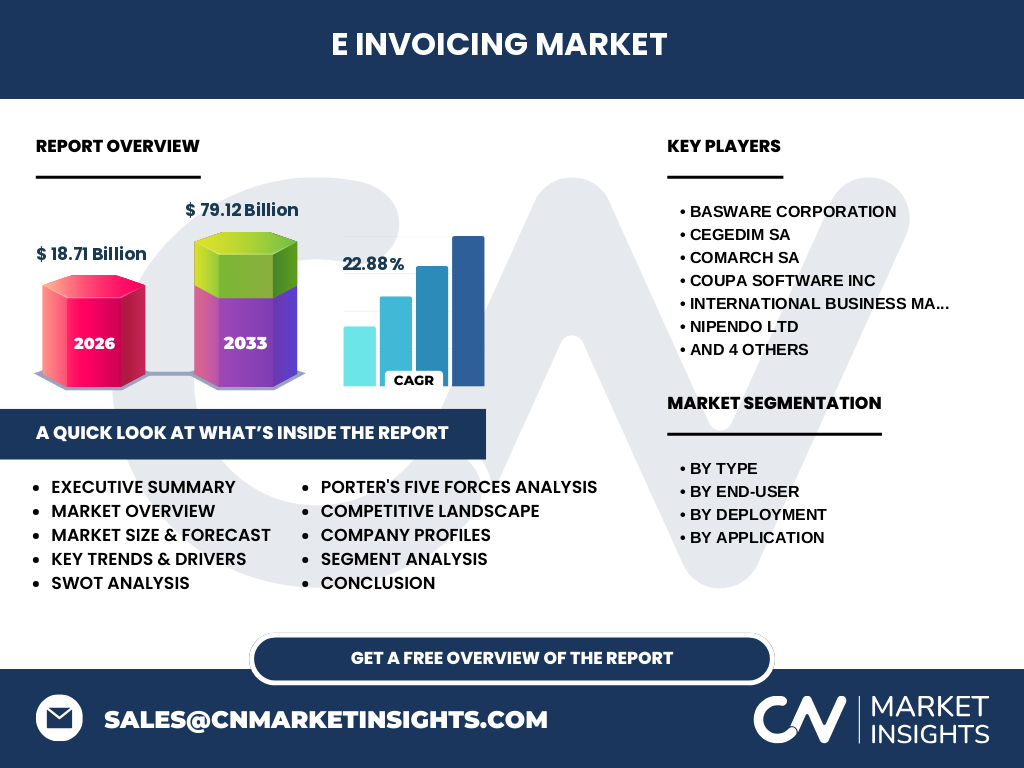

The market is moderately consolidated, featuring global technology leaders and specialised invoicing providers. Prominent players include Basware Corporation, Cegedim SA, Comarch SA, Coupa Software Inc, International Business Machines Corp, Nipendo Ltd, SAP SE, Sage Group Plc, Tradeshift, and Transcepta LLC. Competition centers on platform scalability, regulatory compliance breadth, and value‑added services such as analytics and integration capabilities.

What are the high‑level findings and key takeaways presented in the Executive Summary?

The Executive Summary highlights a market sized at USD 18.71 billion in 2026, projected to reach USD 79.12 billion by 2033, delivering a robust CAGR of 22.88 % over the forecast horizon. Strong regulatory push, cloud migration, and cross‑industry adoption drive growth. The report underscores geographic expansion, consolidation among top vendors, and emerging technology layers that create new revenue streams for forward‑looking players.

What are the forecasted market values for the period 2025‑2032?

Based on the stated CAGR of 22.88 %, the market is expected to expand from its 2026 baseline of USD 18.71 billion to approximately USD 79.12 billion by 2033. This trajectory implies steady double‑digit growth each year through 2032, reflecting continued regulatory roll‑outs and broader enterprise adoption of cloud‑based invoicing solutions.

How is the E‑Invoicing Market sized and shared across the defined segments?

The market is segmented by type (Non‑PO Invoices, PO Invoices), end‑user (Retail & E‑Commerce, Government, IT & Telecom, BFSI), deployment (On‑Premise, Cloud‑Based), and application (B2B, B2C, B2G). While exact monetary splits are not disclosed, each segment benefits from the overall growth trend, with cloud‑based deployments and B2B applications showing the strongest uptake, driven by enterprise‑level digital transformation programs.

What is the global geographic distribution of the E‑Invoicing Market?

The market demonstrates a worldwide footprint, with adoption accelerating in regions that have introduced mandatory e‑invoicing legislation. Major economies in North America, Europe, and the Asia‑Pacific are leading contributors, while emerging markets are beginning to adopt cloud platforms to meet new compliance requirements. Geographic diversification supports the strong CAGR observed.

What are the key performance insights for each major region?

In North America, maturity of ERP ecosystems and high cloud adoption fuel growth. Europe benefits from the EU‑wide directive on electronic invoicing, creating uniform standards that stimulate cross‑border trade. The Asia‑Pacific region shows the fastest growth rate due to rapid digitalisation in China, India, and Southeast Asian economies, coupled with government incentives for paper‑less transactions. These regional dynamics collectively reinforce the market’s upward momentum.

Which companies are leading the E‑Invoicing Market and what strategies are they pursuing?

Leading firms such as SAP SE, IBM, and Basware focus on deep integration with existing ERP suites and expanding cloud service portfolios. Agile players like Tradeshift and Nipendo emphasize API‑centric platforms and strategic partnerships with financial institutions. Companies such as Coupa and Sage target niche verticals through specialised analytics and procurement‑linked invoicing solutions. The prevailing strategy across the board is to broaden ecosystem connectivity while strengthening compliance coverage.

How does Porter’s Five Forces analysis apply to the E‑Invoicing Market?

Threat of new entrants is moderate; high compliance costs and established vendor relationships create barriers. Bargaining power of buyers is growing as enterprises demand flexible, multi‑region solutions. Bargaining power of suppliers (technology platforms) is limited due to commoditisation of cloud infrastructure. Threat of substitutes is low because paper invoicing is rapidly being phased out. Industry rivalry is intense, with players competing on functionality, regulatory coverage, and pricing.

What are the SWOT highlights for the E‑Invoicing Market?

Strengths: Strong regulatory tailwinds, cost‑saving potential, and scalability of cloud models. Weaknesses: Integration complexity with legacy ERP systems and data‑security concerns. Opportunities: Expansion into B2C and B2G segments, AI‑driven analytics, and blockchain verification. Threats: Rapidly changing compliance standards and potential cyber‑risk exposure.

What does the value‑chain analysis reveal about the E‑Invoicing industry?

The value chain begins with software developers creating core invoicing engines, followed by cloud service providers delivering infrastructure. System integrators customize solutions for end‑users, while regulatory bodies define standards that shape product roadmaps. Final users—enterprises and governments—consume the service, generating data that feeds back into analytics providers for continuous improvement. Each link adds incremental value and creates opportunities for partnership.

What key investment insights can be drawn from the E‑Invoicing Market?

Investors should target companies with strong cloud capabilities, robust compliance portfolios, and open API frameworks. Strategic acquisitions of niche analytics or AI firms can accelerate product differentiation. Geographic expansion into high‑growth Asia‑Pacific markets and partnerships with large ERP vendors represent attractive growth levers. The projected market size of USD 79.12 billion by 2033 underscores a lucrative long‑term investment horizon.

What are the concluding remarks and primary takeaways from this market research?

The E‑Invoicing Market is on a decisive growth path, backed by regulatory mandates and the universal shift toward digital finance. With a CAGR of 22.88 % and a forecasted valuation of USD 79.12 billion by 2033, the sector offers compelling opportunities for technology providers, investors, and end‑users seeking efficiency gains. Companies that can combine compliance expertise with cloud scalability will dominate the next phase of market evolution.

How was the research methodology designed for this report?

The study employed a mixed‑method approach, combining primary interviews with industry executives, secondary data collection from reputable databases, and quantitative modeling to project future values. Market sizing leveraged the provided baseline of USD 18.71 billion for 2026 and applied the stated CAGR of 22.88 % to extrapolate forecasts. Segmentation, competitive analysis, and trend identification were validated through triangulation of multiple data sources.

What is the scope of this research and any defined limitations?

The scope covers global E‑Invoicing solutions across type, end‑user, deployment, and application segments, focusing on the period 2025‑2032. While the analysis incorporates all major vendors listed, niche regional players may be under‑represented. Financial figures are limited to the provided market size, forecast, and CAGR; detailed regional revenue breakdowns are excluded due to data constraints.

Which key companies have made recent developments in the E‑Invoicing Market?

Recent activities include Basware’s launch of an AI‑driven invoice validation module, IBM’s partnership with government agencies to standardise B2G invoicing, SAP’s integration of e‑invoicing into its S/4HANA suite, and Tradeshift’s acquisition of a fintech firm to enhance payment automation. Coupa and Sage have introduced cloud‑only invoicing products aimed at mid‑market firms, while Nipendo and Transcepta expanded their API ecosystems to support cross‑border transactions.