1. Microminiature Circular Connectors Market Overview – Definition, scope, and significance

Microminiature circular connectors are compact, high‑density interconnect solutions that provide reliable electrical connections in constrained spaces. They are typically characterized by diameters ranging from 0.5 mm to 3 mm and feature robust locking mechanisms suited for harsh environments. The market encompasses all design, manufacturing, and distribution activities for connectors used across military, aerospace, industrial, and medical sectors. Their significance lies in enabling miniaturized electronics, improving system performance, and supporting the growth of advanced technology platforms such as UAVs and wearable medical devices.

2. Microminiature Circular Connectors Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles

Key drivers include rising demand for lightweight, space‑saving components in defense and aerospace programs, expanding industrial automation, and the proliferation of miniature medical implants. Opportunities arise from emerging UAV applications and the push for IoT‑enabled devices requiring high‑reliability interconnects. Primary restraints are the high manufacturing precision costs and stringent certification requirements, especially for defense and medical use. Challenges involve supply‑chain complexities for specialized materials and the need to balance performance with cost‑effectiveness.

3. Microminiature Circular Connectors Market Growth Trends – Current and emerging trends shaping the market

Current trends feature a shift toward metal‑shell designs for enhanced durability, while plastic‑shell variants gain traction in cost‑sensitive applications. The market is witnessing increased adoption of hermetically sealed connectors for aerospace and defense, driven by higher reliability expectations. Emerging trends include integration of smart‑connector technologies with embedded sensors for health‑monitoring and the development of high‑frequency variants to support 5G and radar systems.

4. COVID‑19 Impact on the Microminiature Circular Connectors Market – Pandemic effects and recovery trajectory

The COVID‑19 pandemic temporarily disrupted supply chains, causing delays in component deliveries and slowing production for aerospace and defense programs. However, the market demonstrated resilience as defense spending remained stable and medical device demand surged. Recovery accelerated in 2022, driven by the reopening of manufacturing facilities and renewed investment in UAV and industrial automation projects, positioning the market on a solid growth path.

5. Microminiature Circular Connectors Market Competitive Landscape – Major competitors and market consolidation

The competitive landscape is fragmented yet dominated by a core group of global players. Leading firms such as Amphenol Corporation, TE Connectivity, HUBER+SUHNER, and Hirose Electric Co., Ltd. command significant brand equity and extensive product portfolios. Recent consolidation activities include strategic acquisitions aimed at expanding technology capabilities and geographic reach, reinforcing the competitive intensity while fostering innovation across metal‑shell and plastic‑shell segments.

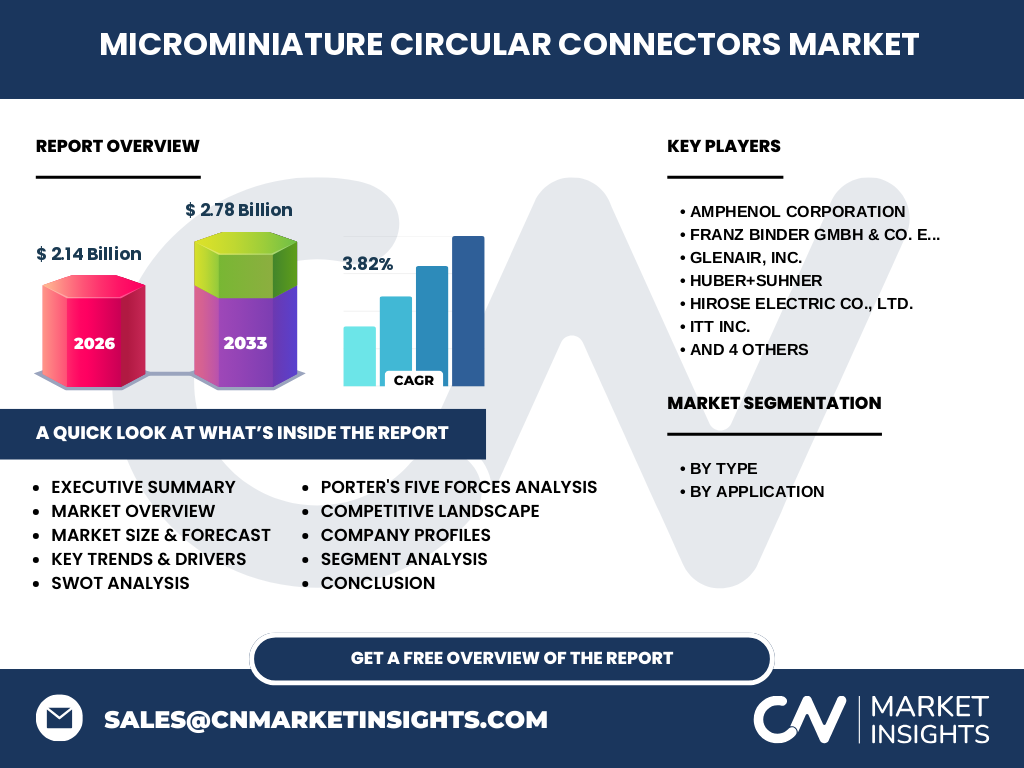

6. Executive Summary – High‑level overview and key findings about Microminiature Circular Connectors Market

The microminiature circular connectors market is valued at USD 2.14 billion in 2026 and is projected to reach USD 2.78 billion by 2033, reflecting a CAGR of 3.82 %. Growth is underpinned by robust demand from military, aerospace, industrial, and medical applications. Metal‑shell connectors lead the type segment, while aerospace/UAV and defense dominate the application segment. Competitive dynamics are shaped by technology‑driven differentiation and strategic partnerships among the top ten manufacturers.

7. Microminiature Circular Connectors Market Forecast – Projections for 2025‑2032 period

Based on current trends, the market will expand steadily, maintaining the 3.82 % CAGR through 2032. The forecast anticipates incremental gains each year, driven by continuous defense expenditure, increasing UAV deployments, and expanding industrial automation initiatives. The metal‑shell sub‑segment is expected to outpace plastic‑shell growth due to higher performance requirements in harsh environments, while medical applications will contribute a steady, niche but growing share.

8. Microminiature Circular Connectors Market Size and Share by Segmentation – Breakdown by segment

Segmentation by type divides the market into metal‑shell and plastic‑shell connectors. Metal‑shell units command a larger share owing to superior durability, thermal resistance, and EMI shielding, making them preferred for defense and aerospace uses. Plastic‑shell connectors retain relevance in cost‑sensitive industrial and consumer‑grade medical devices. By application, the hierarchy is: Military & Defense, Aerospace & UAV, Industrial Application, and Medical, each reflecting distinct performance and regulatory demands.

9. Global Microminiature Circular Connectors Market Size and Share by Region – Geographic distribution

The market exhibits a global footprint with prominent activity in North America, Europe, and the Asia‑Pacific region. North America leads in defense procurement and aerospace innovation, Europe contributes strong industrial automation demand, while Asia‑Pacific shows rapid growth driven by emerging UAV manufacturers and expanding medical device production. Regional shares align with the concentration of key end‑users and the presence of major connector manufacturers.

10. Regional Analysis of the Microminiature Circular Connectors Market – Detailed regional market performance

In North America, sustained defense budgets and a mature aerospace sector propel robust demand for high‑performance metal‑shell connectors. Europe’s focus on industrial automation and stringent medical device standards fuels growth across both connector types. Asia‑Pacific’s accelerating UAV market, coupled with low‑cost manufacturing capabilities, drives volume expansion, particularly for plastic‑shell variants, while also attracting foreign investment from leading global players.

11. Leading Company Profiles in the Microminiature Circular Connectors Market – Industry players and strategies

Key players include Amphenol Corporation, TE Connectivity, HUBER+SUHNER, Hirose Electric, and Omnetics Connector Corporation. These companies leverage extensive R&D resources to develop high‑reliability, miniaturized solutions and pursue strategic alliances with defense contractors and aerospace OEMs. Product diversification, focus on custom engineering services, and expansion of global distribution networks are common strategies to capture market share and address evolving client requirements.

12. Porter’s Five Forces Analysis of the Microminiature Circular Connectors Market – Competitive forces assessment

• Threat of new entrants: Moderate – high technical barriers and certification costs limit newcomers.

• Bargaining power of suppliers: Low to moderate – specialized material suppliers exist, but large manufacturers can negotiate volume discounts.

• Bargaining power of buyers: Moderate – defense and aerospace customers demand high reliability, giving them leverage on specifications and pricing.

• Threat of substitutes: Low – few alternative interconnect technologies can match the performance and miniaturization of circular connectors.

• Industry rivalry: High – intense competition among established firms drives continuous innovation and price competition.

13. SWOT Analysis of the Microminiature Circular Connectors Market – Strengths, weaknesses, opportunities, threats

Strengths: Proven reliability, compact form factor, strong demand in high‑value sectors.

Weaknesses: High production costs, stringent certification timelines.

Opportunities: Growth of UAVs, expansion of medical implant markets, integration of smart‑connector technologies.

Threats: Supply‑chain disruptions for specialty alloys, potential regulatory changes in defense procurement, emergence of alternative high‑frequency interconnects.

14. Microminiature Circular Connectors Market Value Chain Analysis – Industry structure and value flow

The value chain begins with raw‑material sourcing (precision alloys, high‑grade polymers), followed by component design and engineering, precision machining, surface treatment, and assembly. Quality testing and certification (MIL‑STD, ISO, IEC) constitute critical downstream steps before distribution to system integrators. End‑users—defense contractors, aerospace OEMs, industrial equipment manufacturers, and medical device firms—provide feedback that loops back into design improvement, reinforcing a cyclical innovation process.

15. Key Investment Insights in the Microminiature Circular Connectors Market – Strategic investment recommendations

Investors should focus on companies with strong defense contracts and diversified product portfolios across metal‑shell and plastic‑shell lines. Prioritizing firms that demonstrate advanced manufacturing capabilities (e.g., additive manufacturing for custom housings) and active R&D in smart‑connector features can yield superior returns. Geographic investments in Asia‑Pacific manufacturers poised to serve the growing UAV market also present attractive growth potential.

16. Microminiature Circular Connectors Market Conclusion – Summary and key takeaways

The market is on a steady growth trajectory, underpinned by a 3.82 % CAGR and a forecasted increase from USD 2.14 billion in 2026 to USD 2.78 billion by 2033. Metal‑shell connectors dominate due to performance demands, while diverse applications across defense, aerospace, industrial, and medical sectors ensure balanced demand. Competitive pressures drive continual innovation, making the market attractive for strategic investment and partnership opportunities.

17. Research Methodology – How this research was conducted

The study combines primary interviews with industry experts, supplier and buyer surveys, and secondary data from company reports, trade publications, and government defense/ aerospace statistics. Market sizing employed a top‑down approach, aligning known 2026 revenue (USD 2.14 billion) with segmental allocations based on product type and application. Forecasting applied compound annual growth rate (CAGR) calculations (3.82 %) to project the 2027‑2033 market value (USD 2.78 billion).

18. Research Scope – Coverage and limitations

The scope encompasses global microminiature circular connector manufacturers, covering type (metal‑shell, plastic‑shell) and application (military & defense, aerospace & UAV, industrial, medical). Geographic analysis includes major regions—North America, Europe, Asia‑Pacific. Limitations stem from proprietary financial data unavailable for individual companies; therefore, analysis relies on aggregated market figures and publicly disclosed information.

19. Key Companies and Recent Developments in the Microminiature Circular Connectors Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Leading firms such as Amphenol Corporation and TE Connectivity have announced new high‑frequency metal‑shell connector lines targeting UAV radar systems. HUBER+SUHNER unveiled a ruggedized plastic‑shell series designed for medical wearables, while Hirose Electric introduced a miniaturized smart connector with integrated health‑monitoring sensors. Omnetics Connector Corporation secured a multi‑year defense contract for next‑generation spacecraft interconnects, and ITT Inc. expanded its manufacturing footprint in Asia‑Pacific to support growing UAV demand.