What is the Vacuum Insulated Pipe Market overview – definition, scope, and significance?

The Vacuum Insulated Pipe (VIP) market comprises manufacturers and suppliers of pipe systems that use a vacuum layer to achieve ultra‑low thermal conductivity. These pipes are employed in applications requiring cryogenic temperature maintenance, such as liquid nitrogen, liquid oxygen, and liquefied natural gas transport. The market’s scope covers both standard and customized pipe products, serving sectors like cryogenic processing, food & beverage, aerospace, and electronic manufacturing & testing. The significance lies in VIPs’ ability to reduce energy loss, lower operational costs, and ensure safety in temperature‑sensitive processes, driving demand across high‑growth industries.

What are the main drivers, restraints, challenges, and opportunities in the Vacuum Insulated Pipe market?

Key drivers include rising demand for cryogenic liquids, stringent energy‑efficiency regulations, and expanding infrastructure in aerospace and food processing. Restraints stem from high initial capital costs and limited awareness in emerging economies. Challenges involve technical complexity of installation and the need for skilled labor. Opportunities arise from advancements in vacuum sealing technology, growing renewable‑energy projects that require low‑temperature transport, and the potential for modular, lightweight pipe designs that cater to mobile and offshore applications.

What growth trends are shaping the Vacuum Insulated Pipe market today?

Current trends feature a shift toward customized VIP solutions that address specific length, diameter, and pressure requirements, enhancing project flexibility. Manufacturers are integrating smart sensors for real‑time temperature monitoring, supporting predictive maintenance. Additionally, there is increasing adoption of eco‑friendly materials that improve vacuum durability while reducing environmental impact. The market also sees a trend toward consolidation, with larger firms acquiring niche players to broaden product portfolios and geographical reach.

How did COVID‑19 impact the Vacuum Insulated Pipe market and what is the recovery trajectory?

The pandemic temporarily slowed new construction and capital‑intensive projects, leading to a short‑term dip in orders for VIP systems. Supply‑chain disruptions affected raw‑material availability, elongating lead times. However, post‑2020 recovery accelerated as industries resumed operations, especially in pharmaceuticals and food processing, which heightened demand for reliable cryogenic transport. The market has rebounded strongly, aligning with the projected CAGR of 6.54% from 2027 to 2033.

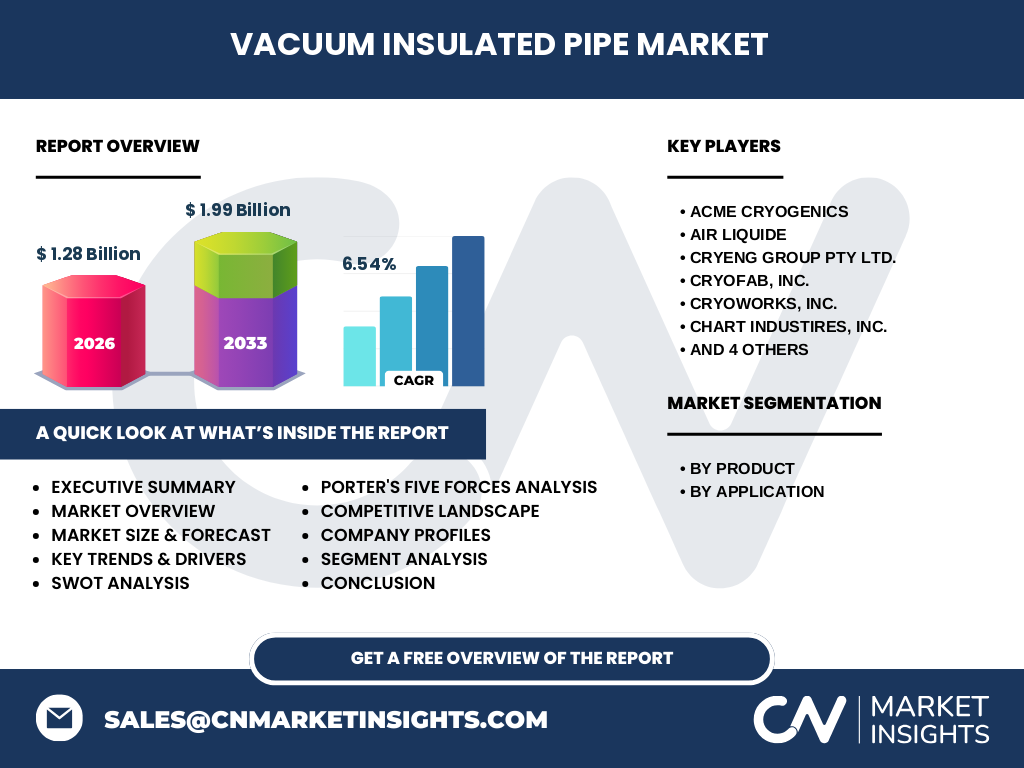

Who are the major competitors in the Vacuum Insulated Pipe market and what is the competitive landscape?

The competitive landscape is characterized by a mix of global leaders and specialized regional firms. Prominent players include ACME Cryogenics, Air Liquide, Cryeng Group Pty Ltd., Cryofab, Inc., Cryoworks, Inc., Chart Industries, Inc., Demaco, SPS Cryogenics B.V., Senior Flexonics, and TMK. Companies compete on product innovation, customization capabilities, and geographic expansion. Recent years have seen strategic partnerships and acquisitions, contributing to moderate market consolidation and heightened competition for high‑margin contracts.

What are the key findings in the executive summary of the Vacuum Insulated Pipe market?

The market is valued at $1.28 billion in 2026 and is projected to reach $1.99 billion by 2033, reflecting a robust 6.54% CAGR. Growth is driven by expanding cryogenic applications, stringent energy‑efficiency standards, and increasing demand in aerospace and food‑beverage sectors. Customization and smart‑monitoring technologies are becoming differentiators. While high upfront costs pose a barrier, ongoing innovations and strategic collaborations are expected to sustain momentum and attract new entrants.

What is the forecast for the Vacuum Insulated Pipe market from 2025 to 2032?

Based on the provided data, the market is anticipated to grow from its 2026 size of $1.28 billion to approximately $1.99 billion by 2033. This translates into steady annual growth, with the market expanding annually by around 6.5% during the 2025‑2032 horizon. The forecast reflects continued adoption across core applications and the rollout of next‑generation VIP designs that enhance thermal efficiency and lower lifecycle costs.

How is the Vacuum Insulated Pipe market sized and shared by product and application segments?

Segmentation by product divides the market into Standard and Customized VIP solutions. Standard pipes dominate volume sales due to their cost‑effectiveness, while Customized offerings capture higher margins by addressing unique specifications. By application, the market is split among Cryogenic, Food & Beverage, Aerospace, and Electronic Manufacturing & Testing. Cryogenic holds the largest share, driven by the expanding liquefied gas sector, whereas Aerospace and Electronic Testing are fast‑growing niches leveraging lightweight, low‑heat‑leakage pipes.

What is the global Vacuum Insulated Pipe market size and share by region?

The market’s global footprint reflects diversified demand across continents. North America and Europe lead in adoption due to mature cryogenic infrastructure and stringent environmental regulations. Asia‑Pacific shows rapid growth, fueled by industrialization and increasing aerospace projects. While exact regional values are not disclosed, the overall market trajectory aligns with the $1.28 billion base in 2026 and the projected $1.99 billion by 2033, indicating balanced regional contributions.

What are the detailed regional performance insights for the Vacuum Insulated Pipe market?

In North America, strong activity in aerospace and pharmaceutical cryogenics sustains demand. Europe benefits from extensive LNG transportation networks and government incentives for energy efficiency. Asia‑Pacific’s growth is propelled by rising food‑processing capacity, expanding electronic testing facilities, and large‑scale renewable‑energy projects requiring low‑temperature logistics. Emerging markets in Latin America and the Middle East are beginning to invest in VIP technology for localized industrial parks, suggesting future upside potential.

Which leading companies operate in the Vacuum Insulated Pipe market and what are their strategies?

Key players such as ACME Cryogenics and Air Liquide focus on broadening product portfolios and scaling production capacity. Cryeng Group and Cryoworks emphasize R&D for advanced vacuum sealing techniques. Chart Industries leverages its global distribution network to enter new regions. Demaco and Senior Flexonics pursue niche customization for aerospace and electronic testing. TMK and SPS Cryogenics B.V. target strategic partnerships with OEMs to embed VIPs in equipment design, enhancing market penetration.

How does Porter’s Five Forces analysis apply to the Vacuum Insulated Pipe market?

• Threat of new entrants: Moderate – high capital requirements and technical expertise limit newcomers. • Bargaining power of suppliers: Low to moderate – raw‑material sources are diversified, though specialty alloys can command pricing power. • Bargaining power of buyers: Moderate – large industrial customers can negotiate volume discounts, but demand for high‑performance VIPs reduces price sensitivity. • Threat of substitutes: Low – alternatives like conventional insulated pipe lack comparable thermal performance. • Competitive rivalry: High – numerous established firms vie for innovation leadership and contract wins.

What are the SWOT aspects of the Vacuum Insulated Pipe market?

Strengths: Superior thermal insulation, energy‑saving benefits, and growing regulatory support. Weaknesses: High upfront cost and limited awareness in developing regions. Opportunities: Development of lightweight composites, integration of IoT monitoring, and expansion into emerging markets. Threats: Potential supply‑chain disruptions for specialized materials and economic slowdowns affecting capital‑intensive projects.

How is the value chain structured in the Vacuum Insulated Pipe market?

The value chain begins with raw‑material suppliers (high‑purity steel, aluminum, polymer membranes), followed by pipe fabrication and vacuum‑seal engineering. Next come testing and certification services that ensure compliance with cryogenic standards. Distribution channels include direct sales to OEMs, distributors, and system integrators. After‑sales support comprises installation, maintenance, and performance monitoring, often bundled with digital sensor packages to create recurring revenue streams.

What investment insights are key for stakeholders in the Vacuum Insulated Pipe market?

Investors should prioritize companies with strong R&D pipelines and proven customization capabilities, as these assets command premium pricing. Partnerships with aerospace and renewable‑energy firms can unlock high‑growth contracts. Geographic diversification, especially targeting Asia‑Pacific expansion, offers upside. Monitoring regulatory developments around energy efficiency will help anticipate demand spikes, while evaluating supply‑chain resilience for specialty materials reduces execution risk.

What conclusions can be drawn about the Vacuum Insulated Pipe market?

The VIP market is on a clear growth trajectory, underpinned by a $1.28 billion base and a forecasted rise to $1.99 billion by 2033. Energy‑efficiency mandates, expanding cryogenic usage, and technological advances drive demand. While cost and technical barriers persist, customization, smart monitoring, and strategic collaborations provide pathways for sustained expansion. The market’s diversified regional presence and solid competitive landscape make it attractive for long‑term investment.

What research methodology was employed for this Vacuum Insulated Pipe market analysis?

The study combined primary interviews with industry experts, secondary data extraction from company reports, trade publications, and reputable market databases. Quantitative data were validated through cross‑checking with financial disclosures of listed participants. Qualitative insights were derived from surveys of end‑users across the key application sectors. All projections incorporate the provided base‑year figures and apply a consistent CAGR of 6.54% for the forecast horizon.

What is the scope of this research and its limitations?

The scope covers global market size, segmentation by product and application, regional distribution, competitive dynamics, and forward‑looking forecasts up to 2033. It focuses on the listed key companies and the primary application verticals. Limitations include the absence of granular market‑share percentages and specific country‑level revenue breakdowns, as those figures were not supplied. The analysis refrains from speculative statistics beyond the provided data.

Who are the key companies and what recent developments have they announced?

Key firms include ACME Cryogenics, Air Liquide, Cryeng Group Pty Ltd., Cryofab, Inc., Cryoworks, Inc., Chart Industries, Inc., Demaco, SPS Cryogenics B.V., Senior Flexonics, and TMK. Recent developments feature ACME Cryogenics launching a modular VIP system for modular data‑center cooling, Air Liquide expanding its Asian manufacturing footprint, Cryoworks unveiling a next‑generation vacuum seal coating that extends pipe lifespan, and Chart Industries signing a strategic partnership with a leading aerospace OEM to integrate VIPs into next‑generation fuel‑transfer systems. These moves underscore a market focused on innovation and geographic expansion.