What is the Clinical Trial Supplies Market Overview – definition, scope, and significance?

The Clinical Trial Supplies (CTS) market encompasses the design, manufacture, packaging, labeling, storage, and logistics of all materials required to conduct clinical investigations, including investigational medicinal products, placebos, and ancillary devices. Its scope covers every stage of a trial—from early‑phase safety studies to large‑scale Phase III and bioequivalence studies—across therapeutic areas such as oncology, cardiovascular, neurological, and respiratory disorders. CTS is critical because the integrity, timing, and compliance of trial materials directly affect patient safety, data quality, regulatory approval, and overall drug development timelines.

What are the main drivers, restraints, challenges, and opportunities in the Clinical Trial Supplies Market?

Key drivers include the rising global demand for new drugs, especially biologics, the expansion of decentralized and hybrid trial models, and increasing regulatory emphasis on supply chain traceability. Restraints stem from complex cold‑chain requirements, high operational costs, and stringent GMP standards. Challenges involve managing multi‑site logistics, mitigating supply disruptions, and ensuring compliance across disparate jurisdictions. Opportunities arise from digitalization of supply chain management, adoption of advanced packaging (e.g., smart blister packs), and growth in emerging markets where clinical research activities are accelerating.

What are the current growth trends shaping the Clinical Trial Supplies Market?

Current trends feature a shift toward on‑demand manufacturing, allowing sponsors to produce small batches quickly for adaptive trial designs. There is also a notable rise in the use of integrated logistics platforms that provide real‑time tracking of temperature‑sensitive shipments. Additionally, the market is seeing increased collaboration between CROs and specialized CTS providers to streamline end‑to‑end services, and a growing preference for sustainable packaging solutions that meet both regulatory and environmental expectations.

How did COVID‑19 impact the Clinical Trial Supplies Market and what is the recovery trajectory?

The pandemic caused temporary disruptions in global logistics, heightened border controls, and shortages of critical cold‑chain resources, leading to delays in trial material deliveries. However, the crisis accelerated the adoption of remote monitoring and decentralized trial approaches, which in turn boosted demand for flexible CTS solutions. Recovery is evident through restored supply chain resilience, expanded pandemic‑preparedness protocols, and a post‑COVID surge in trial activation, positioning the market for robust growth.

Who are the major competitors and what is the current competitive landscape in the Clinical Trial Supplies Market?

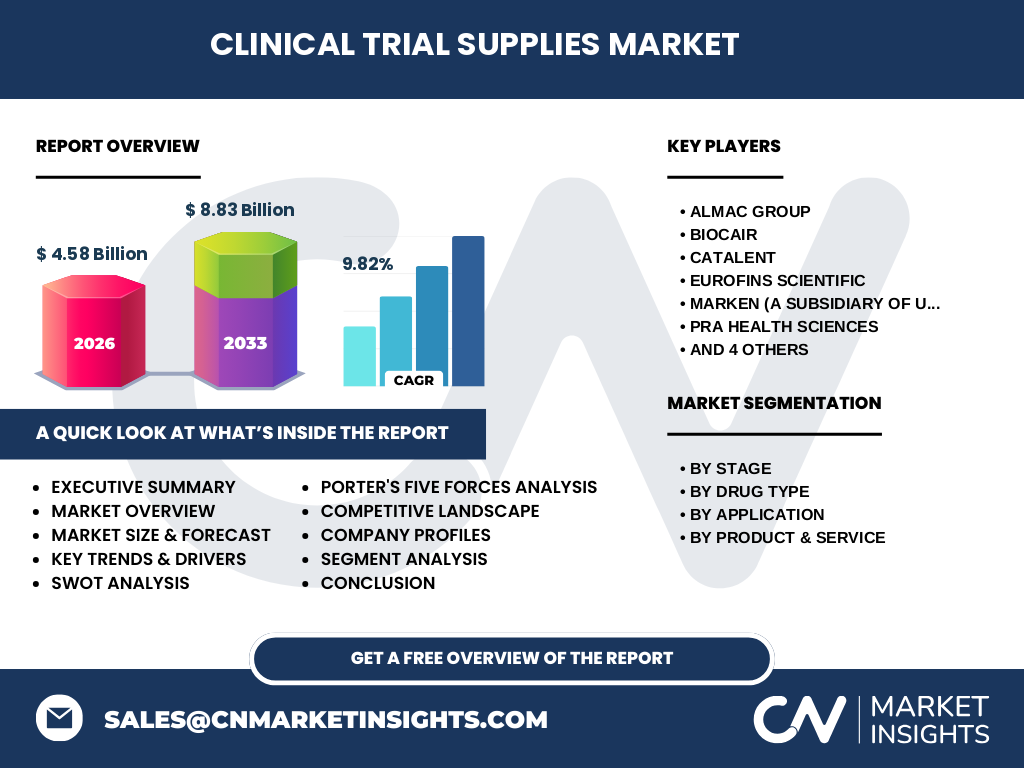

The market is dominated by a mix of specialty logistics firms and integrated CROs. Leading players such as Almac Group, Biocair, Catalent, Eurofins Scientific, Marken (a UPS subsidiary), PRA Health Sciences, Parexel International Corporation, Piramal Pharma Solutions, Sharp Packaging Services, and Thermo Fisher Scientific offer comprehensive CTS portfolios. Recent years have seen strategic acquisitions and partnership agreements that consolidate capabilities, enhance geographic reach, and create differentiated service offerings.

What are the key findings in the Executive Summary of the Clinical Trial Supplies Market?

The CTS market is valued at USD 4.58 billion in 2026 and is projected to reach USD 8.83 billion by 2033, reflecting a CAGR of 9.82 % over the forecast period. Strong growth is underpinned by expanding clinical trial pipelines, rising biologics development, and the emergence of decentralized trial models. Supply‑chain innovation, digital traceability, and sustainable packaging are pivotal enablers. Competitive pressure is intensifying as firms pursue vertical integration and strategic collaborations to capture greater share of the end‑to‑end trial supply value chain.

What are the forecast projections for the Clinical Trial Supplies Market from 2025 to 2032?

Building on the 2026 base of USD 4.58 billion, the market is expected to climb steadily, reaching approximately USD 8.83 billion by 2033. This trajectory indicates sustained double‑digit growth throughout the 2025‑2032 horizon, driven by continuous expansion of trial activity across all phases and therapeutic areas, as well as ongoing investments in supply‑chain technologies and infrastructure.

How is the Clinical Trial Supplies Market sized and shared by segmentation?

Segmentation is performed across four dimensions. By trial stage, the market serves Phase I, Phase II, Phase III, and bioequivalence studies, with later phases typically requiring larger volumes and more complex logistics. By drug type, it distinguishes small‑molecule drugs and biologic drugs, the latter demanding specialized cold‑chain and handling. Application‑wise, the market caters to oncology, cardiovascular diseases, neurological disorders, and respiratory disorders, each with distinct supply‑chain requirements. Finally, by product and service, the market is divided into manufacturing, packaging & labeling, and logistics & distribution, reflecting the end‑to‑end nature of CTS provisioning.

What is the global Clinical Trial Supplies Market size and share by region?

While specific numeric shares are not disclosed, the market exhibits a worldwide footprint, with North America, Europe, Asia‑Pacific, and Rest‑of‑World regions all actively contributing to the overall USD 4.58 billion valuation in 2026. Each region benefits from a robust network of research institutions, pharmaceutical hubs, and logistics infrastructure that support the execution of multinational clinical programs.

What does the regional analysis of the Clinical Trial Supplies Market reveal?

North America leads in trial volume and innovation, leveraging mature regulatory frameworks and a high density of CROs. Europe follows with strong academic research centers and increasing adoption of patient‑centric trial designs. Asia‑Pacific presents the fastest growth potential, driven by expanding biotech ecosystems, cost‑effective manufacturing, and supportive government policies. The Rest‑of‑World markets, including Latin America and the Middle East, are emerging as attractive sites for patient recruitment and supply‑chain diversification.

What are the profiles and strategies of leading companies in the Clinical Trial Supplies Market?

Almac Group focuses on integrated services that combine drug substance manufacturing with packaging and distribution. Biocair specializes in temperature‑controlled logistics for biologics. Catalent offers end‑to‑end solutions from drug product development to global supply. Eurofins Scientific provides comprehensive analytics and testing alongside CTS. Marken leverages UPS’s global network for rapid, compliant distribution. PRA Health Sciences and Parexel integrate CTS within broader CRO offerings. Piramal Pharma Solutions emphasizes flexible manufacturing capacity, while Sharp Packaging Services delivers specialized packaging solutions. Thermo Fisher Scientific supports the market through its extensive laboratory and supply‑chain technologies.

How does Porter’s Five Forces analysis apply to the Clinical Trial Supplies Market?

Threat of new entrants is moderate due to high capital requirements, regulatory barriers, and the need for specialized cold‑chain expertise. Bargaining power of suppliers is relatively low as many raw material providers are commoditized, though specialized packaging suppliers hold marginal leverage. Bargaining power of buyers—pharmaceutical sponsors and CROs—is strong, given their ability to negotiate service levels and price. Threat of substitutes is limited; alternative supply models (e.g., in‑house manufacturing) exist but are less common. Industry rivalry is intense, driven by consolidation, service differentiation, and geographic expansion.

What are the SWOT insights for the Clinical Trial Supplies Market?

Strengths: Critical role in drug development, high entry barriers, and growing demand for complex biologics. Weaknesses: Dependence on tight logistics, high operational costs, and regulatory complexity. Opportunities: Digital supply‑chain platforms, decentralized trial growth, and sustainable packaging innovation. Threats:

The value chain begins with drug substance synthesis, followed by formulation and fill‑finish manufacturing. Next, packaging and labeling add patient‑specific information and protection. Logistics and distribution then ensure temperature‑controlled, timed delivery to trial sites worldwide. Post‑delivery services include return logistics, quarantine management, and traceability reporting, completing a closed‑loop system that safeguards product integrity throughout the trial lifecycle. Investors should consider companies that offer integrated end‑to‑end solutions, as they are positioned to capture higher margins and long‑term contracts. assets in cold‑chain logistics, digital tracking, and sustainable packaging are likely to yield competitive advantage. Additionally, targeting firms expanding in high‑growth regions such as Asia‑Pacific can provide exposure to emerging trial activity. Partnerships with CROs and pharma sponsors also represent strategic pathways for revenue diversification. The CTS market is on a strong upward trajectory, underpinned by a robust CAGR of 9.82 % and an expected market size of USD 8.83 billion by 2033. Growth is fueled by expanding clinical pipelines, especially in biologics, and the shift toward decentralized trial designs that demand flexible, reliable supply solutions. Competitive dynamics favor firms that can deliver integrated, technology‑enabled services across the entire supply chain. The study combined primary interviews with industry experts, secondary analysis of company reports, regulatory filings, and reputable market databases. Trend extrapolation leveraged the provided base-year market size (USD 4.58 billion) and forecast (USD 8.83 billion) using the disclosed CAGR of 9.82 %. Segmentation was derived from standard industry classifications. The research covers global CTS activities across all trial phases, drug types, therapeutic applications, and service categories. It focuses on major players listed in the provided data set and excludes detailed regional revenue breakdowns beyond the qualitative description. Financial estimates are confined to the figures supplied; no additional market share percentages are presented. Recent announcements include Almac Group’s launch of a new biologics packaging line, Biocair’s expansion of its temperature‑controlled fleet in Asia, Catalent’s acquisition of a specialty logistics firm to bolster its distribution network, Eurofins Scientific’s introduction of advanced analytical services for trial material verification, and Marken’s partnership with a leading CRO to streamline global trial supply. Additionally, PRA Health Sciences and Parexel have announced joint initiatives to integrate CTS into their digital trial platforms, while Piramal Pharma Solutions opened a flexible manufacturing site to support rapid trial material turnaround.What does the value chain analysis of the Clinical Trial Supplies Market show?

What key investment insights can be drawn from the Clinical Trial Supplies Market?

What are the main conclusions of the Clinical Trial Supplies Market report?

How was the research for this report conducted?

What is the scope of the research and its limitations?

Which key companies have made recent developments in the Clinical Trial Supplies Market?