What is the Europe Wet Pet Food Market Overview – definition, scope, and significance?

The Europe wet pet food market comprises ready‑to‑serve, moisture‑rich formulations formulated for companion animals, primarily dogs and cats. It includes products packaged in cans and flexible pouches that are sold through supermarkets, specialized pet retailers, and online platforms across the continent. The market’s significance stems from rising pet ownership, increasing consumer willingness to spend on premium nutrition, and a broader trend toward convenience and health‑focused pet diets. In 2026 the market was valued at €8.76 billion, reflecting its role as a major segment of the broader pet food industry and a key driver of growth for manufacturers and retailers alike.

What are the Europe Wet Pet Food Market drivers, restraints, challenges, and opportunities?

Key drivers include the growing humanisation of pets, which fuels demand for higher‑quality, nutritionally complete wet foods, and the expansion of e‑commerce channels that broaden product accessibility. Urbanisation and smaller living spaces also push owners toward convenient, portion‑controlled wet meals. Restraints arise from price sensitivity in certain regions, as wet foods are typically priced higher than dry alternatives. Challenges involve supply‑chain volatility for raw animal proteins and stringent EU food‑safety regulations that increase compliance costs. Opportunities lie in product innovation—such as functional ingredients, limited‑ingredient lines for sensitive pets, and sustainable packaging—and in tapping under‑served markets in Eastern Europe where pet ownership is rising rapidly.

What are the current Europe Wet Pet Food Market growth trends?

Recent trends show a shift toward premiumisation, with brands launching grain‑free, high‑protein, and organ‑rich formulas that cater to health‑conscious owners. Sustainable packaging, especially recyclable pouches, is gaining traction as regulators and consumers demand lower environmental impact. Another emerging trend is the integration of digital tools, such as subscription‑based delivery services and AI‑driven nutrition recommendations, which enhance customer loyalty. Finally, the rise of ‘human‑grade’ ingredients—where pet food uses the same quality standards as human food—continues to reshape product positioning.

How did COVID‑19 impact the Europe Wet Pet Food Market and what is the recovery trajectory?

During the pandemic, pet adoption surged across Europe, creating a sudden increase in demand for wet food, particularly through online channels as lockdowns limited in‑store shopping. Supply‑chain disruptions briefly constrained raw material availability, leading to modest price upticks. Post‑2020, demand has remained robust, with consumers maintaining higher spending on pet nutrition as pets became part of household wellbeing routines. The market is now on a steady recovery path, supported by sustained e‑commerce growth and continued pet‑ownership rates that exceed pre‑COVID levels.

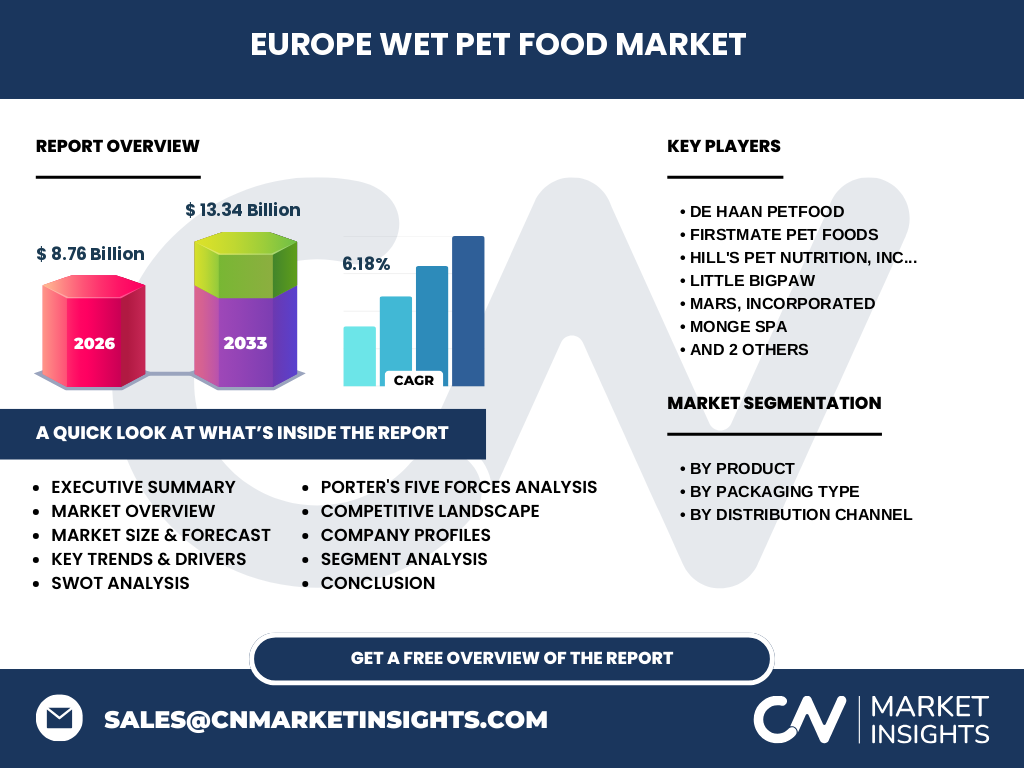

Who are the major competitors in the Europe Wet Pet Food Market and what is the level of market consolidation?

The competitive landscape is characterised by a mix of multinational giants and specialised regional players. Leading companies include De Haan Petfood, FirstMate Pet Foods, Hill’s Pet Nutrition, Inc., Little BigPaw, Mars, Incorporated, Monge SPA, Nestlé, and Petguard Holdings, LLC. Consolidation has accelerated through strategic acquisitions and joint ventures, allowing larger firms to broaden their wet‑food portfolios and gain distribution efficiencies. Nevertheless, niche brands retain relevance by focusing on premium, functional, or sustainable product lines, preserving a diversified competitive environment.

What are the key findings in the Executive Summary of the Europe Wet Pet Food Market?

The market is valued at €8.76 billion in 2026 and is projected to reach €13.34 billion by 2033, delivering a CAGR of 6.18 % over the forecast horizon. Growth is driven by premiumisation, expanding e‑commerce, and evolving consumer attitudes toward pet health. Canned and pouch formats dominate, with pouches gaining share due to convenience and sustainability appeal. Dogs account for the larger product segment, while cat wet foods exhibit strong growth in urban markets. Leading manufacturers are investing in product innovation and sustainable packaging, positioning the market for continued expansion despite pricing pressures.

What is the Europe Wet Pet Food Market forecast for 2025‑2032?

Based on the provided CAGR of 6.18 %, the market is expected to expand steadily from its 2026 baseline of €8.76 billion to approximately €13.34 billion by 2033. This trajectory suggests a compound increase of roughly €4.58 billion over the seven‑year period, reflecting consistent demand across all segments and regions. The forecast underscores opportunities for new product launches, especially in functional and sustainable categories, and signals attractive returns for investors targeting the pet‑food sector.

How is the Europe Wet Pet Food Market sized and shared by segmentation?

Segmentation by product reveals two primary categories: dog wet food and cat wet food. Dog wet food holds the larger portion of total sales, reflecting higher consumption volumes and a broader variety of formulations. By packaging type, cans remain the traditional dominant format, while pouches are rapidly gaining market share owing to their lightweight, resealable nature and lower carbon footprint. Distribution channels are divided among supermarkets and hypermarkets, specialised pet shops, and online platforms, with online sales experiencing the fastest growth rate due to changing buying habits.

What is the global Europe Wet Pet Food Market size and share by region?

Within the global context, Europe represents a major hub for wet pet food consumption, contributing €8.76 billion in 2026. While specific figures for other continents are not disclosed, Europe’s share is a substantial component of the worldwide wet pet food market, underscoring the region’s leadership in product innovation, regulatory standards, and consumer willingness to invest in premium pet nutrition.

What does the regional analysis of the Europe Wet Pet Food Market reveal?

The market exhibits variation across Western, Northern, Southern, and Eastern Europe. Western Europe (e.g., Germany, France, the UK) leads in overall value due to mature retail networks and high disposable income. Northern Europe shows strong demand for sustainable packaging and functional formulas. Southern Europe, with growing pet populations in Italy and Spain, is expanding rapidly in both canned and pouch formats. Eastern Europe presents emerging opportunities, as increasing pet ownership couples with rising middle‑class incomes, creating a fertile ground for both mainstream and premium wet foods.

Which leading companies operate in the Europe Wet Pet Food Market and what are their strategies?

Key players include De Haan Petfood, FirstMate Pet Foods, Hill’s Pet Nutrition, Inc., Little BigPaw, Mars, Incorporated, Monge SPA, Nestlé, and Petguard Holdings, LLC. Strategies across the board focus on portfolio diversification—adding grain‑free, high‑protein, and functional lines—while expanding sustainable packaging options. Many firms are enhancing direct‑to‑consumer capabilities through subscription models and leveraging data analytics to tailor product offerings. Strategic partnerships with veterinary networks and pet‑health influencers are also common, aiming to strengthen brand credibility.

How does Porter’s Five Forces analysis apply to the Europe Wet Pet Food Market?

• Threat of new entrants – Moderate; high regulatory compliance and economies of scale create barriers, yet niche premium brands can enter through online channels. • Bargaining power of suppliers – Moderate to high, given reliance on quality animal protein and strict EU safety standards. • Bargaining power of buyers – Increasing, as consumers compare brands online and demand value, sustainability, and health benefits. • Threat of substitutes – Low to moderate; dry pet food and fresh‑frozen pet meals compete, but wet food’s convenience and palatability maintain its niche. • Industry rivalry – High; numerous established manufacturers compete on innovation, price, and distribution reach.

What are the SWOT insights for the Europe Wet Pet Food Market?

Strengths: Strong consumer demand for premium, convenient nutrition; robust distribution networks; high brand loyalty. Weaknesses: Price sensitivity in certain markets; dependence on animal‑protein supply chains. Opportunities: Sustainable packaging, functional ingredients, and digital subscription services. Threats: Regulatory changes, raw‑material price volatility, and competitive pressure from alternative pet‑food formats.

What does the value chain of the Europe Wet Pet Food Market look like?

The value chain starts with raw‑material sourcing (meat, fish, vegetables), followed by formulation and processing in specialized facilities. Packaging (cans and pouches) is conducted with an emphasis on food safety and sustainability. Distribution channels then move products to wholesalers, retailers (supermarkets, pet shops), and directly to consumers via online platforms. End‑of‑life considerations increasingly incorporate recycling and circular‑economy initiatives, especially for flexible pouches.

What key investment insights can be drawn for the Europe Wet Pet Food Market?

Investors should target companies that exhibit strong R&D pipelines focused on health‑oriented formulations and sustainable packaging. Brands with scalable e‑commerce infrastructure and subscription‑based revenue models are positioned for higher growth. Partnerships with veterinary networks can enhance credibility and market penetration. Moreover, M&A activity remains a viable path to acquire niche premium brands and accelerate entry into fast‑growing Eastern European markets.

What is the overall conclusion of the Europe Wet Pet Food Market analysis?

The Europe wet pet food market is on a solid growth trajectory, driven by premiumisation, convenience, and evolving pet‑owner attitudes toward health and sustainability. With a projected market size of €13.34 billion by 2033 and a steady 6.18 % CAGR, the sector offers attractive opportunities for manufacturers, retailers, and investors. Success will hinge on innovation, supply‑chain resilience, and the ability to meet consumer expectations for quality and environmental responsibility.

What research methodology was employed for this market study?

The analysis combined primary interviews with industry experts, senior managers, and retail buyers, alongside secondary data from company reports, trade publications, and EU regulatory filings. Quantitative forecasting used a compound annual growth rate model anchored on the 2026 market size of €8.76 billion and the projected 2033 value of €13.34 billion. Segmentation, competitive mapping, and value‑chain assessments were derived from triangulating primary insights with publicly available financial and supply‑chain information.

What is the scope of the research and its limitations?

The study covers the wet pet food segment for dogs and cats across Europe, examining product type, packaging, and distribution channels. It includes market size, growth forecasts, competitive dynamics, and strategic insights. Limitations stem from the reliance on publicly disclosed figures and the exclusion of proprietary sales data for individual companies, which may affect granular market‑share estimations.

Which key companies have recent developments in the Europe Wet Pet Food Market?

Recent activities include De Haan Petfood launching a new line of recyclable pouches, FirstMate Pet Foods expanding its organic wet‑food range, Hill’s Pet Nutrition, Inc. introducing a functional line targeting joint health, Little BigPaw rolling out limited‑edition flavors in partnership with local chefs, Mars, Incorporated acquiring a boutique European brand to enhance its premium portfolio, Monge SPA investing in advanced sterilisation technology, Nestlé unveiling a sustainability programme for its wet‑food packaging, and Petguard Holdings, LLC launching a direct‑to‑consumer subscription service across several EU markets.