North America Quartz Market Overview - Definition, scope, and significance?

The North America Quartz Market comprises the production, processing, and distribution of quartz in its various forms—including quartz surface and tile, high‑purity quartz, quartz glass, quartz crystal, and quartz sand—across key end‑user industries such as electronics and semiconductors, solar, construction, medical, and optics‑telecommunications. This market is significant because quartz’s physical hardness, chemical stability, and optical clarity make it indispensable for high‑tech components, renewable‑energy modules, and durable building materials, driving substantial economic value in the region.

North America Quartz Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Primary drivers include robust demand for semiconductor wafers, rapid expansion of solar‑panel installations, and sustained construction activity that fuels quartz surface and tile sales. Opportunities arise from emerging quantum‑computing applications and increased use of high‑purity quartz in medical diagnostics. Restraints involve fluctuating raw‑material costs and stringent environmental regulations on quartz mining. Challenges stem from supply‑chain disruptions and the need for advanced processing technologies to meet tighter purity specifications.

North America Quartz Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a shift toward thin‑film solar technologies that require higher‑grade quartz glass, and a growing preference for engineered quartz countertops in residential and commercial builds. Emerging trends include the adoption of quartz‑based photonic devices in 5G networks and increased investment in quartz crystal oscillators for precision timing in aerospace applications. Sustainability initiatives are also prompting manufacturers to adopt greener extraction and recycling methods.

COVID-19 Impact on the North America Quartz Market - Pandemic effects and recovery trajectory?

The pandemic caused temporary shutdowns of mining operations and delayed construction projects, leading to a short‑term dip in quartz surface demand. However, the surge in remote work accelerated data‑center expansions, bolstering demand for quartz in semiconductor and optics. By 2022, the market rebounded, and the recovery trajectory remains positive, supported by renewed construction activity and expanding renewable‑energy investments.

North America Quartz Market Competitive Landscape - Major competitors and market consolidation?

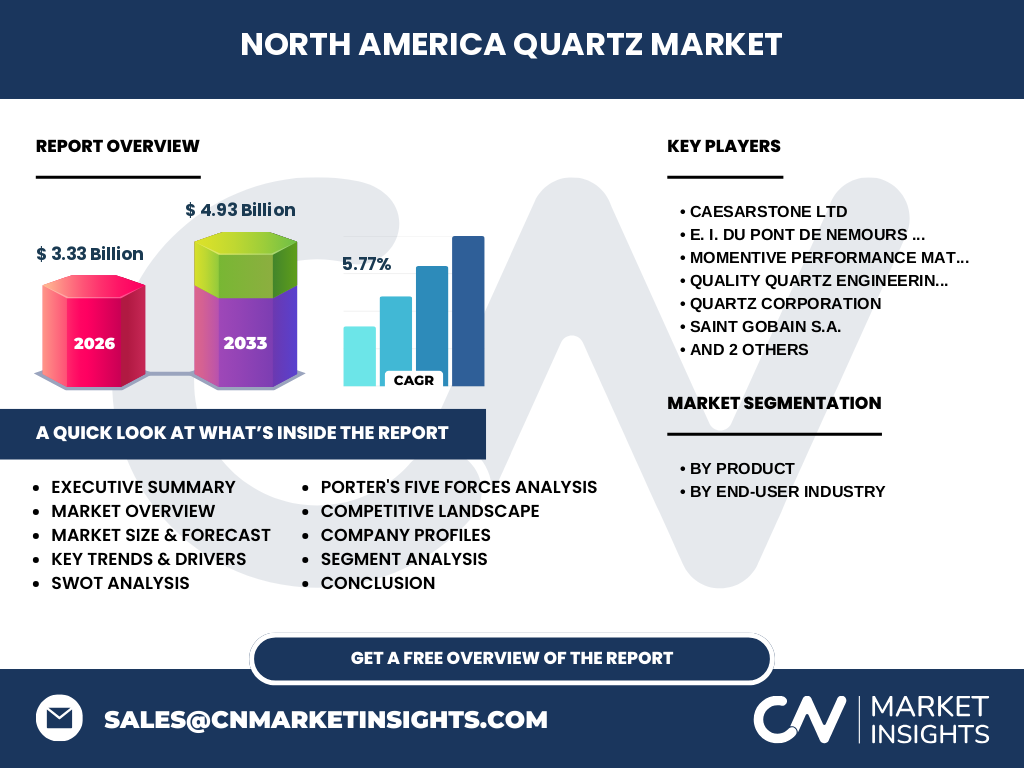

The competitive landscape is fragmented, with several multinational and regional players. Key competitors include Caesarstone Ltd, E.I. Du Pont De Nemours and Company, Momentive Performance Materials Inc., Quality Quartz Engineering, Quartz Corporation, Saint‑Gobain S.A., Sibelco NV, and Thermo Fisher Scientific Inc. Recent consolidation activity includes strategic acquisitions aimed at expanding product portfolios and geographic reach, reinforcing the competitive intensity.

Executive Summary - High-level overview and key findings about North America Quartz Market?

The North America Quartz Market is valued at $3.33 billion in 2026 and is projected to reach $4.93 billion by 2033, reflecting a CAGR of 5.77 % over the forecast horizon. Growth is driven by robust demand in electronics, solar, and construction, while opportunities exist in quantum‑computing and medical applications. Competitive pressures are high, with major players pursuing acquisitions and product‑innovation strategies to capture market share.

North America Quartz Market Forecast - Projections for 2025-2032 period?

Based on the stated CAGR of 5.77 %, the market is expected to expand steadily from its 2026 baseline of $3.33 billion to $4.93 billion by 2033. This trajectory suggests a consistent annual increase driven by rising end‑user demand, especially in semiconductor manufacturing and solar‑energy deployment, coupled with ongoing construction growth and technological advancements in optics.

North America Quartz Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by product includes quartz surface and tile, high‑purity quartz, quartz glass, quartz crystal, and quartz sand. By end‑user industry, the market is divided among electronics and semiconductor, solar, buildings and construction, medical, and optics‑telecommunication sectors. Each segment contributes uniquely to overall market value, with electronics and construction representing the largest consumption, while high‑purity quartz and quartz crystal drive high‑margin niche segments.

Global North America Quartz Market Size and Share by Region - Geographic distribution?

Within the global quartz industry, North America holds a leading position due to its advanced manufacturing base and high adoption rates of semiconductor and renewable‑energy technologies. While precise regional shares are undisclosed, the region’s market size of $3.33 billion in 2026 underscores its importance relative to other continents, supported by strong domestic demand and export capabilities.

Regional Analysis of the North America Quartz Market - Detailed regional market performance?

In the United States, demand for quartz in electronics and solar panels dominates, while Canada shows steady growth in construction‑related quartz applications. The U.S. Midwest and West Coast are hotspots for semiconductor fabs, driving high‑purity quartz consumption. The Northeast exhibits higher per‑capita usage of quartz surfaces in commercial real estate, reflecting regional architectural trends.

Leading Company Profiles in the North America Quartz Market - Industry players and strategies?

Caesarstone Ltd focuses on engineered quartz surfaces, leveraging design collaborations. DuPont emphasizes high‑purity quartz for semiconductor and aerospace. Momentive expands its quartz glass portfolio for optics. Quality Quartz Engineering provides customized quartz sand for specialty applications. Quartz Corporation and Saint‑Gobain target construction markets, while Sibelco emphasizes sustainable mining. Thermo Fisher supplies quartz crystals for scientific instrumentation.

Porter's Five Forces Analysis of the North America Quartz Market - Competitive forces assessment?

• Threat of new entrants: Moderate, due to high capital requirements and regulatory hurdles in mining. • Bargaining power of suppliers: Low to moderate, as raw quartz is abundant but high‑purity grades are limited. • Bargaining power of buyers: High in construction and electronics, where large OEMs demand price competitiveness. • Threat of substitutes: Low, because quartz’s unique properties are hard to replace. • Competitive rivalry: Intense, driven by product differentiation and strategic acquisitions.

SWOT Analysis of the North America Quartz Market - Strengths, weaknesses, opportunities, threats?

Strengths: Abundant raw material, advanced processing capabilities, and diversified end‑user base.

Weaknesses: Sensitivity to raw‑material price volatility and environmental compliance costs.

Opportunities: Expansion into quantum‑device components, medical‑imaging quartz, and recycled‑quartz products.

Threats: Supply‑chain disruptions, stricter mining regulations, and potential trade barriers.

North America Quartz Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with quartz mining and raw‑material extraction, followed by beneficiation and purification. Next, specialized processing creates finished products such as engineered surfaces, glass, and crystals. Distribution channels include B2B wholesalers, direct OEM supply, and retail for consumer‑grade surfaces. End‑users—electronics manufacturers, solar panel assemblers, builders, and medical device firms—complete the chain, creating feedback loops for product innovation.

Key Investment Insights in the North America Quartz Market - Strategic investment recommendations?

Investors should prioritize companies with diversified product portfolios, especially those expanding high‑purity quartz and quartz glass lines for semiconductor and solar growth. Acquisitions targeting sustainable mining operations can mitigate regulatory risk. Funding R&D in quantum‑ready quartz crystals offers high‑return potential, while partnerships with construction firms can secure steady demand for engineered quartz surfaces.

North America Quartz Market Conclusion - Summary and key takeaways?

The market demonstrates solid growth, moving from $3.33 billion in 2026 to an anticipated $4.93 billion by 2033, driven by electronics, solar, and construction demand. Competitive dynamics are shaped by major multinationals pursuing innovation and consolidation. Opportunities lie in emerging high‑tech applications and sustainable practices, while challenges include raw‑material cost volatility and regulatory pressures.

Research Methodology - How this research was conducted?

The study combines primary interviews with industry executives, secondary data from company reports, trade publications, and government databases. Quantitative analysis employs time‑series forecasting based on the given CAGR of 5.77 % and market size figures, while qualitative insights derive from SWOT, Porter’s Five Forces, and value‑chain assessments.

Research Scope - Coverage and limitations?

The scope covers North American quartz production, processing, and end‑use applications across all major product categories and industries listed. It excludes detailed regional market share percentages beyond the provided aggregate figures and does not project individual company financials beyond the aggregate market forecast.

Key Companies and Recent Developments in the North America Quartz Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Caesarstone launched a new line of eco‑friendly engineered quartz countertops. DuPont announced a partnership with a leading semiconductor fab to supply high‑purity quartz. Momentive introduced an advanced quartz glass for high‑temperature optics. Quality Quartz Engineering secured a contract for custom quartz sand in aerospace filtration. Saint‑Gobain expanded its North American distribution network for building‑material quartz. Sibelco unveiled a sustainable mining initiative, and Thermo Fisher released next‑generation quartz crystal oscillators for precision instrumentation.