What is the Medical Imaging Informatics Market Overview – definition, scope, and significance?

The Medical Imaging Informatics market encompasses technologies, software, hardware, and services that enable the acquisition, storage, distribution, and analysis of medical images across healthcare settings. It supports digital radiography, ultrasound, MRI, CT, nuclear imaging, and mammography, facilitating faster diagnosis, improved patient outcomes, and streamlined workflow. The market’s significance lies in its role in enhancing clinical decision‑making, reducing radiation exposure, and integrating imaging data with electronic health records, thereby driving efficiency and quality in modern healthcare.

What are the key drivers, restraints, challenges, and opportunities in the Medical Imaging Informatics Market?

Key drivers include rising prevalence of chronic diseases, increasing demand for non‑invasive diagnostics, and growing adoption of AI‑enabled imaging analysis. Government initiatives for digital health transformation and expanding outpatient imaging services also propel growth. Restraints stem from high upfront capital costs and stringent regulatory requirements. Challenges involve data security concerns and interoperability issues among heterogeneous systems. Opportunities arise from emerging cloud‑based platforms, AI‑driven workflow optimization, and expanding tele‑radiology services in underserved regions.

What growth trends are currently shaping the Medical Imaging Informatics Market?

Current trends feature a shift toward integrated software‑hardware solutions, adoption of AI for image reconstruction and lesion detection, and migration to cloud‑centric data storage. Vendors are bundling services such as predictive maintenance and remote diagnostics. Additionally, the rise of point‑of‑care imaging devices and the convergence of imaging with precision medicine are accelerating market momentum.

How has COVID‑19 impacted the Medical Imaging Informatics Market and what is the recovery trajectory?

The pandemic initially disrupted elective imaging procedures, temporarily slowing demand. However, the crisis expedited digital adoption as hospitals required remote image sharing and AI‑assisted triage to manage infection control. Post‑COVID, demand rebounded strongly, with increased investment in tele‑radiology and robust growth projected as healthcare systems continue to prioritize resilient, digitized imaging infrastructures.

Who are the major competitors and what is the competitive landscape like in the Medical Imaging Informatics Market?

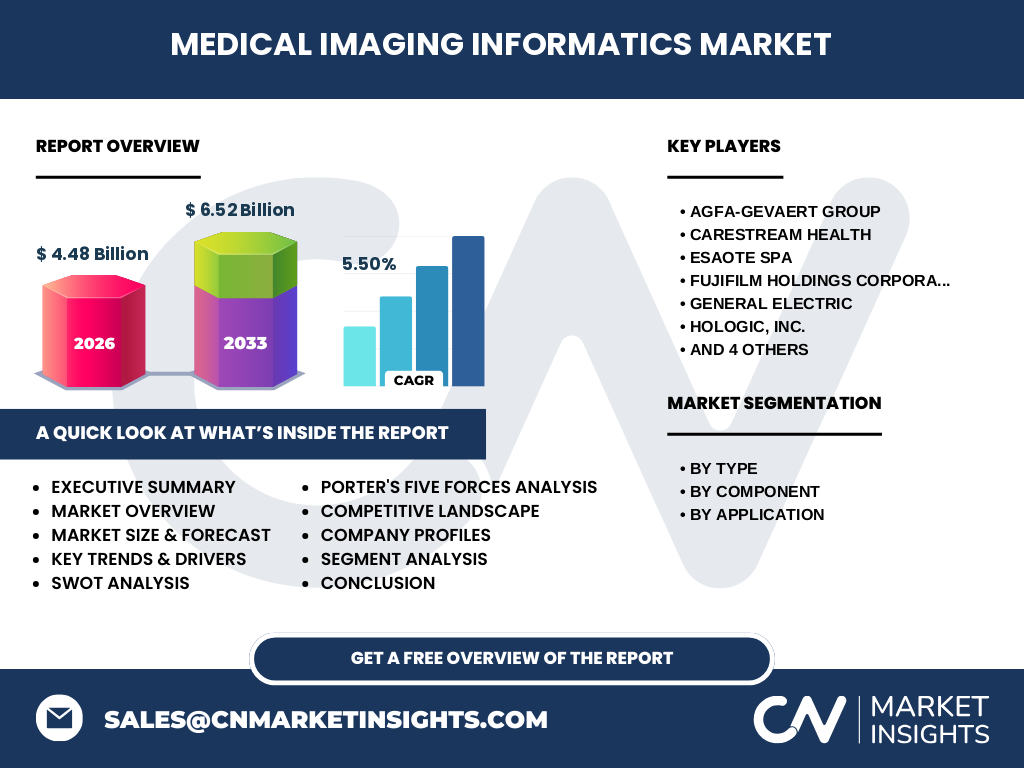

The market is dominated by established players such as Agfa‑Gevaert Group, Carestream Health, ESAOTE SPA, Fujifilm Holdings Corporation, General Electric, Hologic, Inc., Konica Minolta, Inc., Koninklijke Philips N.V., Shenzhen Mindray Bio‑Medical Electronics Co., Ltd., and Siemens Healthcare GmbH. Competitive dynamics are shaped by product innovation, strategic partnerships, and portfolio diversification across software, hardware, and services. Recent consolidation activities highlight a trend toward offering end‑to‑end imaging solutions.

What are the key findings in the Executive Summary of the Medical Imaging Informatics Market?

The market is valued at US$4.48 billion in 2026 and is projected to reach US$6.52 billion by 2033, reflecting a compound annual growth rate of 5.5 %. Growth is driven by AI integration, expanding outpatient imaging, and increased demand for interoperable solutions. Leading vendors are focusing on bundled software‑hardware offerings and expanding services to capture higher-margin segments.

What are the market forecasts for the Medical Imaging Informatics Market for 2025‑2032?

Based on the provided CAGR of 5.5 %, the market is expected to continue expanding steadily through 2032, maintaining momentum from digital transformation initiatives and AI adoption. The forecast underscores a robust upward trajectory, with sustained demand across hospital, ambulatory, and diagnostic center applications.

How is the Medical Imaging Informatics Market sized and shared by segmentation?

Segmentation by type includes Digital Radiography, Ultrasound, MRI, CT, Nuclear Imaging, and Mammography. By component, the market is divided into Software, Hardware, and Services. Application segmentation covers Hospital, Ambulatory Healthcare Settings, and Diagnostic and Imaging Centers. While precise numeric shares are not disclosed, each segment contributes to the overall market growth, with software and services experiencing accelerated adoption due to AI and cloud trends.

What is the global Medical Imaging Informatics Market size and share by region?

The market’s global footprint reflects balanced contributions from North America, Europe, Asia‑Pacific, and Rest of World regions. Each region benefits from healthcare infrastructure investments and digital health policies, collectively supporting the projected US$6.52 billion market size by 2033.

What does the regional analysis reveal about the Medical Imaging Informatics Market?

North America leads in early adoption of AI‑driven imaging solutions and regulatory support for digital health. Europe follows with strong public‑sector funding for hospital upgrades. Asia‑Pacific exhibits the fastest growth, driven by expanding hospital networks and rising disposable income. Emerging markets in Latin America and the Middle East show incremental uptake as they modernize imaging capabilities.

Which companies are leading in the Medical Imaging Informatics Market and what are their strategies?

Key players such as Siemens Healthcare, Philips, GE, and Fujifilm focus on integrated platforms that combine hardware excellence with advanced software analytics. Agfa‑Gevaert and Carestream pursue niche strengths in digital radiography and workflow automation. Companies like Mindray and ESAOTE target emerging markets with cost‑effective solutions, while Hologic emphasizes specialized mammography and women's health imaging.

How does Porter’s Five Forces analysis apply to the Medical Imaging Informatics Market?

Threat of new entrants is moderate due to high capital requirements and regulatory hurdles. Bargaining power of suppliers is limited as component sources are diversified. Bargaining power of buyers is growing, with hospitals demanding interoperable, cost‑effective solutions. Threat of substitutes remains low because imaging informatics is core to diagnostics. Industry rivalry is intense, driving innovation and strategic alliances.

What are the SWOT strengths, weaknesses, opportunities, and threats for the Medical Imaging Informatics Market?

Strengths: Robust technological base, strong demand for AI‑enhanced diagnostics, and high clinical relevance.

Weaknesses: High upfront costs and fragmented standards.

Opportunities: Cloud migration, tele‑radiology expansion, and AI‑driven predictive analytics.

Threats: Cybersecurity risks and potential regulatory changes that could delay product launches.

What does the value chain of the Medical Imaging Informatics Market look like?

The value chain starts with R&D and component manufacturing (sensors, processors), moves through system integration (hardware‑software bundling), followed by distribution to hospitals and imaging centers. Post‑sale services include installation, training, maintenance, and software updates, while data analytics and cloud hosting form the final value‑adding layer.

What key investment insights can be drawn for the Medical Imaging Informatics Market?

Investors should focus on companies leading AI integration and cloud‑based service models, as these segments promise higher margins. Partnerships that enhance interoperability and market entry into high‑growth Asia‑Pacific locales are also attractive. Monitoring regulatory pipelines for AI‑enabled diagnostics can uncover early‑stage investment opportunities.

What are the main conclusions of the Medical Imaging Informatics Market report?

The market is on a sustained growth path, underpinned by digital transformation, AI adoption, and expanding outpatient imaging. With a projected CAGR of 5.5 % and a 2033 valuation of US$6.52 billion, the sector offers compelling opportunities for vendors, investors, and healthcare providers seeking efficient, data‑driven imaging solutions.

How was the research methodology designed for this Medical Imaging Informatics Market report?

The study employed a mixed‑method approach, combining primary interviews with industry experts, secondary data from reputable databases, and quantitative modeling to project market size. Trend analysis, competitive benchmarking, and scenario planning were used to validate forecasts and assess strategic dynamics.

What is the scope of this research, including coverage and limitations?

The research covers global market size, segmentation by type, component, and application, and regional performance across major geographies. It evaluates leading vendors, technology trends, and investment outlooks. Limitations are confined to publicly available data and the provided financial figures; proprietary or undisclosed market shares are not quantified.

Which key companies have made recent developments in the Medical Imaging Informatics Market?

Recent activities include Siemens Healthcare’s launch of AI‑enhanced MRI suites, Philips’ partnership with cloud providers for remote image processing, GE’s acquisition of a software analytics firm to strengthen service offerings, Fujifilm’s rollout of low‑dose digital radiography systems, and Mindray’s entry into the African market with cost‑effective ultrasound platforms. These developments underscore a focus on AI, cloud integration, and geographic expansion.