1. What is the Asia Pacific Cooling Water Treatment Chemicals Market and why is it significant?

The Asia Pacific Cooling Water Treatment Chemicals market comprises chemical solutions—such as corrosion inhibitors, scale inhibitors, and biocides—used to protect and optimize industrial cooling water systems. The market scope covers applications in power generation, food & beverage processing, and textiles across the Asia Pacific region. Its significance stems from the region’s rapid industrialization, expanding power infrastructure, and stringent environmental regulations that demand efficient water‑use management and system reliability.

2. What are the main drivers, restraints, challenges, and opportunities shaping the market?

Key drivers include growing electricity demand, increased thermal power capacity, and heightened focus on water conservation, all of which boost demand for treatment chemicals. Restraints arise from high raw‑material costs and the capital intensity of upgrading legacy cooling systems. Challenges involve evolving regulatory standards and competition from alternative non‑chemical treatment technologies. Opportunities exist in the adoption of eco‑friendly biocides, digital monitoring of water chemistry, and expansion into emerging economies such as Vietnam and the Philippines.

3. Which growth trends are currently influencing the market?

Current trends feature a shift toward integrated water‑treatment packages that combine corrosion, scale, and microbiological control in a single formulation. Manufacturers are also investing in advanced polymer‑based inhibitors that offer longer service life. Additionally, the rise of “smart cooling plants” employing real‑time sensors to adjust chemical dosing is emerging as a catalyst for higher efficiency and reduced chemical consumption.

4. How did COVID‑19 affect the market and what is the recovery outlook?

The pandemic caused temporary shutdowns of several power and manufacturing facilities, leading to a short‑term dip in chemical consumption. However, stimulus‑driven infrastructure projects and post‑pandemic capacity expansions quickly revived demand. Recovery is now robust, with the market expected to resume its growth trajectory and benefit from renewed investment in clean energy and industrial modernization.

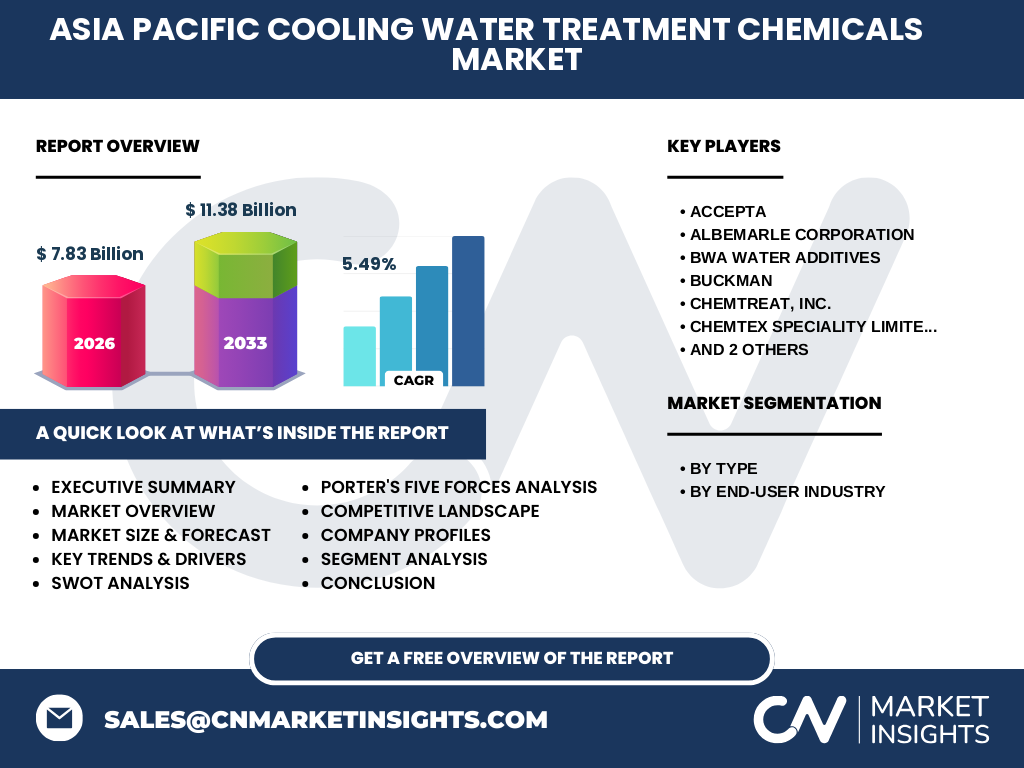

5. Who are the major competitors and what is the level of market consolidation?

Leading players include Accepta, Albemarle Corporation, BWA Water Additives, Buckman, ChemTreat, Inc., Chemtex Speciality Limited, Kemira Oyj, and Veolia Water Technologies. The competitive landscape is moderately consolidated, with a handful of multinational firms commanding significant portions of the market while niche regional providers focus on specific end‑users. Recent M&A activity reflects strategic moves to broaden product portfolios and geographic reach.

6. What are the key findings in the executive summary?

The Asia Pacific Cooling Water Treatment Chemicals market was valued at USD 7.83 billion in 2026 and is projected to reach USD 11.38 billion by 2033, delivering a CAGR of 5.49 % over the forecast horizon. Growth is driven by expanding power generation capacity, stricter environmental mandates, and increasing adoption of advanced chemical formulations. Competitive dynamics are shaped by innovation, strategic partnerships, and a modest consolidation trend among leading global players.

7. What are the market forecasts for 2025‑2032?

While specific yearly figures are not disclosed, the market is forecast to grow steadily from its 2026 base of USD 7.83 billion to USD 11.38 billion by 2033. This trajectory implies sustained demand across all three chemical types—corrosion inhibitors, scale inhibitors, and biocides—and across all end‑user industries, with power generation remaining the largest consumption segment.

8. How is the market sized and shared by segment?

Segmentation by type includes corrosion inhibitors, scale inhibitors, and biocides, each essential for protecting cooling circuits. By end‑user industry, the power sector leads, followed by food & beverage and textile applications. Although precise monetary splits are unavailable, the balanced product mix reflects the diversified needs of high‑temperature, high‑throughput cooling systems throughout the region.

9. What is the geographic distribution of market size and share?

The Asia Pacific region encompasses major economies such as China, India, Japan, South Korea, and Southeast Asian nations. Market size reflects the collective demand of these countries, with China and India contributing the largest share due to their extensive power generation projects and expanding manufacturing bases. The overall regional footprint underpins the USD 7.83 billion valuation reported for 2026.

10. How does each sub‑region perform within the market?

East Asia, led by China, Japan, and South Korea, shows the highest adoption of advanced treatment chemicals, driven by sophisticated industrial infrastructure. South Asia, particularly India, exhibits rapid growth as new thermal power plants come online. Southeast Asia presents a steady rise, with countries like Indonesia and Vietnam investing in power and food‑processing capacity, thereby expanding chemical demand.

11. Which companies lead the market and what strategies are they pursuing?

Key players such as Kemira Oyj and Buckman focus on innovative polymer‑based inhibitors and digital dosing solutions. Albemarle leverages its specialty chemicals expertise to broaden biocide portfolios. Veolia emphasizes integrated water‑treatment services, bundling chemicals with engineering and maintenance. Accepta and ChemTreat pursue strategic alliances with OEMs to embed their chemicals into turnkey cooling plant designs.

12. How does Porter’s Five Forces framework apply to this market?

Threat of new entrants is moderate due to high R&D costs and regulatory barriers. Bargaining power of suppliers is limited, as raw material sources are diversified. Bargaining power of buyers is growing, with large power utilities demanding cost‑effective, environmentally compliant solutions. Threat of substitutes remains low, as non‑chemical alternatives lack the same reliability for scale and corrosion control. Industry rivalry is intense, driven by product differentiation and service integration.

13. What are the market’s SWOT characteristics?

Strengths: Strong demand from expanding power infrastructure; proven efficacy of chemical treatments.

Weaknesses: Sensitivity to raw‑material price volatility.

Opportunities: Development of green biocides and digital dosing platforms.

Threats: Potential regulatory tightening on hazardous chemicals and emerging non‑chemical treatment technologies.

14. What does the value chain for cooling water treatment chemicals look like?

The value chain starts with raw‑material suppliers (e.g., phosphates, polymers), proceeds to formulation manufacturers, then to distributors and system integrators who deliver chemicals to end‑users. After-sales services—such as dosing system calibration and performance monitoring—add value and foster long‑term contracts, reinforcing the overall profitability of the chain.

15. What investment insights can be drawn from the market?

Investors should target companies that combine high‑performance formulations with digital service layers, as this integration enhances customer lock‑in and margin potential. Funding opportunities exist in joint ventures focused on eco‑friendly biocides and in startups offering AI‑driven water‑quality analytics. Geographic exposure to fast‑growing markets like India and Southeast Asia also presents upside.

16. What are the key takeaways and conclusions?

The Asia Pacific Cooling Water Treatment Chemicals market is on a solid growth path, underpinned by a 5.49 % CAGR and a projected rise to USD 11.38 billion by 2033. Power generation remains the primary catalyst, while emerging eco‑friendly solutions and digital dosing are reshaping competitive dynamics. Companies that innovate across product chemistry and service integration are best positioned to capture future gains.

17. How was the research conducted?

Research methodology combined primary interviews with industry experts, secondary data from company reports, government publications, and reputable market databases. Trend analysis, CAGR calculations, and competitive mapping were applied to synthesize a coherent market view while adhering strictly to the supplied financial figures.

18. What is the scope of the research and its limitations?

The study covers the Asia Pacific region, focusing on three chemical types and three end‑user industries. While it provides a comprehensive overview, the analysis does not break down market share by individual country or present proprietary financial metrics beyond the disclosed size and growth figures.

19. Which key companies have announced recent developments?

Accepta launched a next‑generation corrosion inhibitor designed for high‑temperature power cycles. Albemarle introduced a low‑toxicity biocide targeting the food & beverage sector. BWA Water Additives announced a strategic partnership with a major Indian utility to supply scale inhibitors. Buckman unveiled an AI‑enabled dosing controller. ChemTreat, Inc. expanded its service network across Southeast Asia, and Veolia Water Technologies announced a joint venture to deliver integrated water‑treatment solutions in the textile industry.