What is the Asia Pacific Quartz Market overview – definition, scope, and significance?

The Asia Pacific Quartz Market encompasses the production, processing, and distribution of quartz in its various forms—including quartz surface and tile, high‑purity quartz, quartz glass, quartz crystal, and quartz sand—across the Asia Pacific region. The market serves a broad spectrum of end‑user industries such as electronics and semiconductor manufacturing, solar energy, construction, medical devices, and optics & telecommunications. Quartz is valued for its exceptional hardness, chemical stability, and optical clarity, making it a critical raw material for high‑tech applications and durable building products. The significance of this market lies in its contribution to the region’s rapid industrialization, infrastructure development, and the growing demand for renewable energy and advanced electronic components.

What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Quartz Market?

Key drivers include the surge in semiconductor fabrication plants, expansion of solar photovoltaic capacity, and robust construction activities in emerging economies such as Vietnam, Indonesia, and the Philippines. The desire for high‑purity quartz in medical imaging and optics also fuels demand. Restraints stem from the capital‑intensive nature of quartz mining and processing, as well as fluctuating raw material costs. Challenges involve stringent environmental regulations, supply‑chain disruptions, and competition from alternative materials like silicon carbide. Opportunities arise from technological advancements in quartz crystal growth, increased adoption of quartz‑based solar panels, and the burgeoning market for engineered quartz surfaces in residential and commercial projects.

What are the current growth trends in the Asia Pacific Quartz Market?

Current trends show a shift toward integrated quartz solutions, where manufacturers combine surface, crystal, and glass products to offer turnkey packages for electronics manufacturers. There is also a growing emphasis on sustainability, with companies investing in eco‑friendly extraction methods and recycling of quartz waste. Digitalization of supply chains and the use of AI for predictive maintenance in quartz processing plants are emerging, improving operational efficiency and reducing downtime.

How has COVID‑19 impacted the Asia Pacific Quartz Market and what is the recovery trajectory?

The pandemic caused temporary shutdowns of quartz mines and processing facilities, leading to short‑term supply shortages. Demand from the construction sector declined during lockdowns, while electronics and medical segments remained resilient due to heightened need for devices and diagnostic equipment. Post‑2021, the market has rebounded strongly, driven by the resurgence of construction projects and accelerated semiconductor investments, positioning the region on a clear path to recovery and growth.

Who are the major competitors and what is the state of market consolidation in the Asia Pacific Quartz Market?

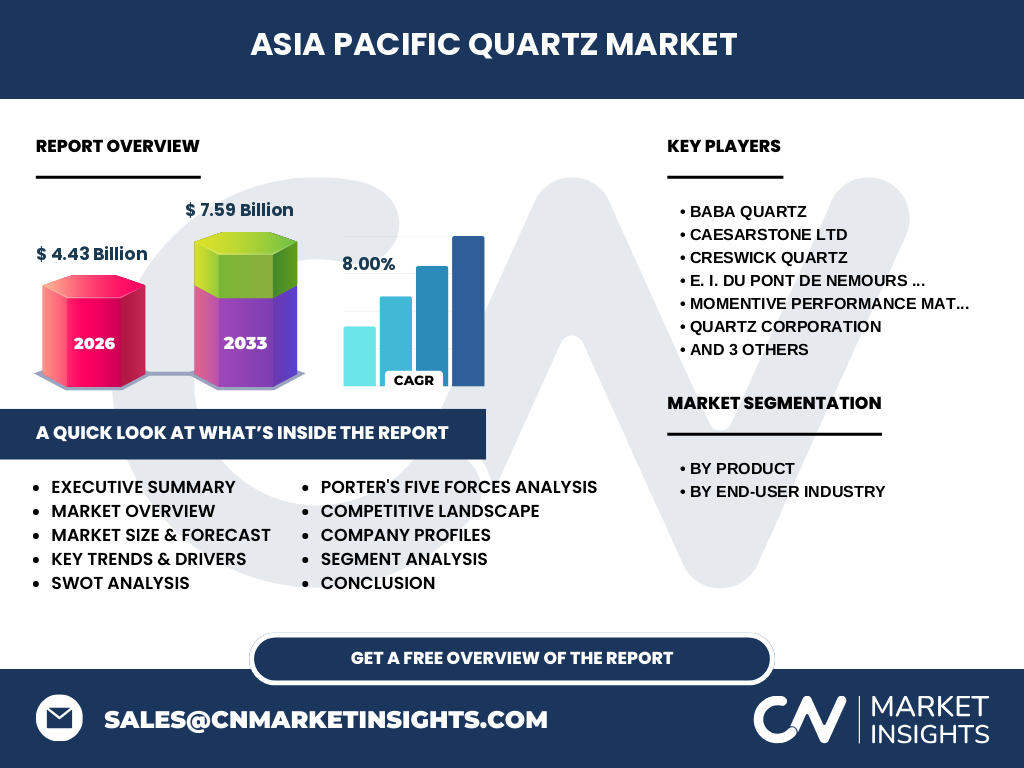

Leading competitors include Baba Quartz, Caesarstone Ltd, Creswick Quartz, E.I. Du Pont de Nemours and Company, Momentive Performance Materials Inc., Quartz Corporation, Saint‑Gobain S.A., Sibelco NV, and Thermo Fisher Scientific Inc. The market exhibits moderate consolidation, with a few global players holding significant market share while numerous regional firms operate niche segments. Mergers and strategic alliances are becoming common as companies seek to broaden product portfolios and enhance geographic reach.

What is the executive summary – high‑level overview and key findings about the Asia Pacific Quartz Market?

The Asia Pacific Quartz Market is valued at USD 4.43 billion in 2026 and is projected to reach USD 7.59 billion by 2033, reflecting a robust CAGR of 8 %. Growth is driven by expanding electronics, solar, and construction industries, alongside advancements in quartz processing technologies. The market faces environmental and supply‑chain challenges but offers considerable opportunities through sustainable practices and product innovation. Major players are consolidating through partnerships, positioning the region for sustained expansion.

What are the forecast projections for the Asia Pacific Quartz Market from 2025 to 2032?

Based on the provided CAGR of 8 %, the market is expected to maintain a steady upward trajectory throughout the 2025‑2032 period. The forecast suggests a consistent increase in demand across all product segments, with particular acceleration in high‑purity quartz for semiconductor applications and quartz surface materials for the construction sector. The growth pattern underscores the region’s ongoing industrialization and its role as a supplier to global high‑tech value chains.

How is the Asia Pacific Quartz Market sized and shared by product and end‑user segmentation?

By product, the market is divided into quartz surface and tile, high‑purity quartz, quartz glass, quartz crystal, and quartz sand. Each segment addresses specific industry needs: surface and tile serve construction; high‑purity quartz caters to electronics and medical; quartz glass is essential for optics; quartz crystal supports telecommunications; and quartz sand is a foundational material for multiple applications. By end‑user industry, the market serves electronics and semiconductor, solar, buildings and construction, medical, and optics and telecommunications, reflecting a diversified demand base that mitigates reliance on any single sector.

What is the global Asia Pacific Quartz Market size and share by region?

The Asia Pacific region accounts for the entirety of the reported market size, standing at USD 4.43 billion in 2026 and projected to reach USD 7.59 billion by 2033. This concentration underscores the region’s dominance in quartz production and its strategic importance to global supply chains.

What does the regional analysis reveal about the performance of the Asia Pacific Quartz Market?

China remains the largest producer, benefiting from abundant quartz reserves and mature processing infrastructure. Australia and India are emerging as key contributors, with increasing investments in mining and value‑added processing. Southeast Asian nations are experiencing rapid growth due to expanding construction and renewable energy projects, while Japan and South Korea continue to drive demand for high‑purity quartz in advanced electronics and optics.

What are the leading company profiles and their strategic approaches in the Asia Pacific Quartz Market?

Baba Quartz focuses on vertically integrated mining and high‑purity crystal production. Caesarstone Ltd leverages brand strength in engineered quartz surfaces. Creswick Quartz emphasizes sustainable extraction practices. Du Pont and Momentive provide specialty quartz glass and high‑performance materials for aerospace and telecom. Quartz Corporation and Sibelco NV specialize in bulk quartz sand supply. Saint‑Gobain S.A. and Thermo Fisher Scientific Inc. target high‑value medical and scientific applications. Across the board, companies are investing in R&D, expanding regional footprints, and pursuing joint ventures to meet diversified end‑user needs.

How does Porter’s Five Forces analysis apply to the Asia Pacific Quartz Market?

Bargaining power of suppliers: Moderate, as quartz deposits are geographically concentrated but abundant. Bargaining power of buyers: High for large semiconductor and construction firms that can negotiate pricing. Threat of new entrants: Low to moderate due to high capital requirements and regulatory barriers. Threat of substitutes: Limited, though alternatives like silicon carbide pose competition in specific niches. Industry rivalry: Intense, driven by product differentiation and cost efficiencies among established players.

What are the SWOT insights for the Asia Pacific Quartz Market?

Strengths: Rich natural resources, diversified end‑user base, and strong technical expertise. Weaknesses: Environmental compliance costs and dependence on capital‑intensive infrastructure. Opportunities: Growth in renewable energy, advanced electronics, and sustainable construction. Threats: Regulatory tightening, raw material price volatility, and competition from emerging alternative materials.

What does the value chain analysis reveal about the Asia Pacific Quartz Market?

The value chain starts with mineral exploration and mining, followed by primary processing (crushing, washing, grading). Subsequent stages include high‑purity refining, crystal growth, glass forming, and surface fabrication. Distribution channels involve bulk shipments to manufacturers and specialized logistics for high‑value crystal products. End‑users receive the final quartz components for integration into electronic wafers, solar panels, building facades, medical devices, or optical lenses. Value‑adding activities such as R&D and custom engineering are critical for higher margins.

What key investment insights can be drawn for stakeholders interested in the Asia Pacific Quartz Market?

Investors should prioritize companies with vertically integrated operations and strong R&D pipelines, as they are better positioned to capture premium pricing in high‑purity and specialty segments. Sustainable mining initiatives and partnerships with solar or semiconductor firms offer attractive growth avenues. Monitoring regulatory developments and investing in technologies that reduce environmental impact can also mitigate risk and enhance long‑term profitability.

What are the concluding takeaways from the Asia Pacific Quartz Market analysis?

The market is on a clear growth trajectory, underpinned by a solid CAGR of 8 % and expanding demand across multiple high‑value industries. While environmental and supply‑chain challenges exist, the region’s resource base, combined with technological innovation and strategic consolidation, creates a favorable outlook. Companies that invest in sustainability, product diversification, and strategic alliances are likely to lead the market.

How was the research methodology designed for this market study?

The study employed a mixed‑method approach, integrating primary interviews with industry experts, secondary data from company reports, trade publications, and governmental sources. Quantitative analysis leveraged the provided market size, forecast, and CAGR figures, while qualitative insights were derived from trend analysis, competitive benchmarking, and expert opinion.

What is the scope of this research, and what limitations should readers be aware of?

The research covers the Asia Pacific Quartz Market from 2026 to 2033, focusing on product and end‑user segmentation, regional performance, and competitive dynamics. Limitations include reliance on publicly available data and the absence of proprietary financial disclosures beyond the provided market size and growth rates.

Which key companies and recent developments are shaping the Asia Pacific Quartz Market?

Notable players such as Baba Quartz announced the commissioning of a new high‑purity crystal plant in 2024, enhancing capacity for semiconductor clients. Caesarstone Ltd launched an eco‑friendly engineered quartz line targeting green construction projects. Du Pont expanded its quartz glass portfolio with a partnership focused on next‑generation optical fibers. Momentive Performance Materials introduced a high‑temperature quartz glass for aerospace applications. Sibelco NV reported increased sand export volumes to meet rising demand from solar panel manufacturers. These developments underscore the market’s dynamism and the strategic moves of leading firms.