What is the Europe Choline Chloride Market Overview – definition, scope, and significance?

Europe’s choline chloride market comprises the production, distribution, and consumption of choline chloride across diverse applications such as animal feed, human nutrition supplements, and oil‑and‑gas processes. The market is defined by its role as a vital nutrient and functional additive that supports liver health, metabolic function, and stress resistance. Its scope extends from raw material manufacturers to downstream formulators, making it a strategic component for enhancing product performance and regulatory compliance throughout the European region.

What are the primary drivers, restraints, challenges, and opportunities shaping the Europe Choline Chloride Market?

Key drivers include rising demand for sustainable animal feed solutions, increased consumer focus on health‑boosting nutrition, and regulatory encouragement of feed additives that improve livestock productivity. Restraints arise from stringent environmental regulations on chemical handling and price volatility of raw materials. Challenges involve supply‑chain disruptions and the need for stringent quality certifications. Opportunities stem from emerging applications in functional foods, formulation of low‑sodium feed additives, and partnerships with biotechnology firms to develop bio‑derived choline sources.

Which growth trends are currently influencing the Europe Choline Chloride Market?

Current trends feature a shift toward high‑concentration choline chloride formulations that reduce transport weight, the integration of choline chloride into precision‑feeding regimens, and the adoption of clean‑label claims in human nutrition products. Additionally, there is a growing trend of consolidating feed additive portfolios to streamline regulatory filings, and an increasing emphasis on traceability through blockchain technologies that enhance supply‑chain transparency.

How did COVID‑19 affect the Europe Choline Chloride Market and what is the recovery trajectory?

The pandemic caused temporary disruptions in raw‑material logistics and delayed capital projects in the feed and nutrition sectors. However, the heightened awareness of immune health boosted demand for choline‑enriched products, accelerating recovery. By late 2022, the market rebounded, and the subsequent years have shown a steady up‑trend, supported by resilient supply chains and renewed investment in animal‑health initiatives across Europe.

What does the competitive landscape look like for the Europe Choline Chloride Market?

The competitive arena is characterized by a handful of global chemical manufacturers and specialized feed‑additive firms competing on quality, price, and service. Market consolidation is evident through strategic alliances and acquisitions aimed at expanding geographic reach and product breadth. While ALGRY Qu is a noted player, other major competitors focus on diversifying product lines and investing in R&D to develop proprietary choline formulations that meet stringent EU standards.

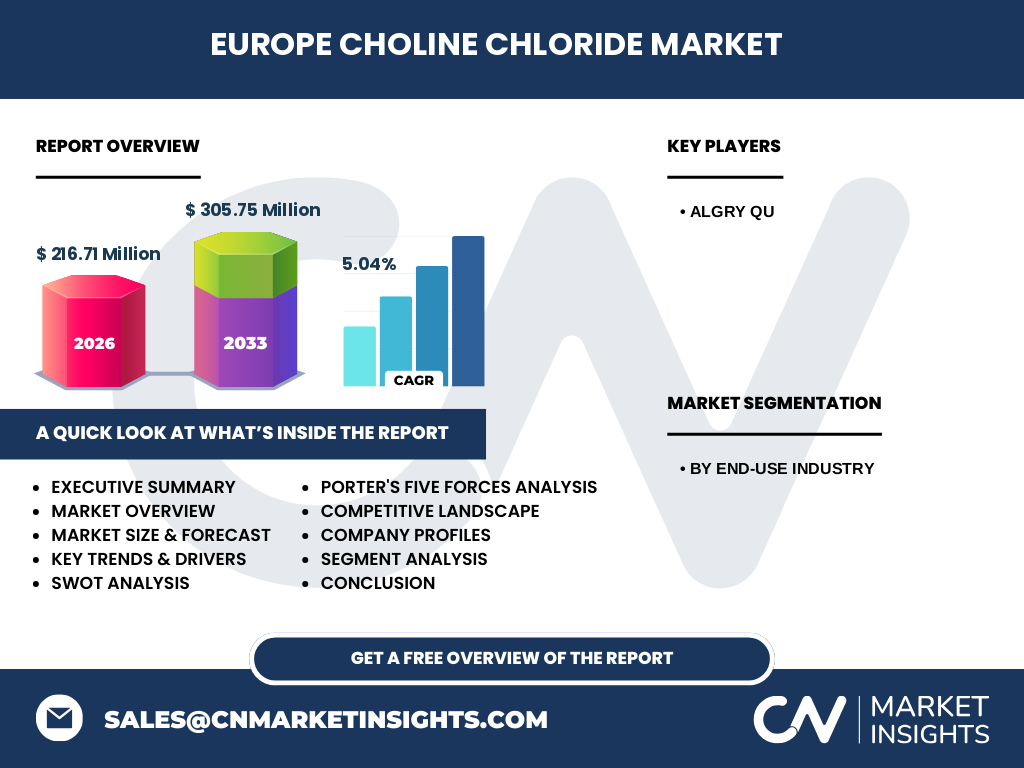

Can you provide an executive summary of the Europe Choline Chloride Market?

The European choline chloride market is valued at €216.71 million in 2026 and is projected to reach €305.75 million by 2033, reflecting a compound annual growth rate of 5.04 %. Growth is propelled by expanding feed‑industry demand, rising consumer interest in functional nutrition, and modest but growing use in oil‑and‑gas applications. The market remains attractive for investors due to its moderate fragmentation, steady regulatory support, and clear pathways for product innovation.

What are the forecast expectations for the Europe Choline Chloride Market from 2025 to 2032?

Based on the 5.04 % CAGR, the market is expected to maintain a consistent upward trajectory, with annual increments of roughly €10‑12 million. Growth will be underpinned by incremental adoption in the feed sector, increased incorporation into fortified foods, and modest expansion in oil‑and‑gas corrosion‑inhibition processes. The forecast suggests a robust demand environment, encouraging capacity expansions and potential entry of new niche players.

How is the Europe Choline Chloride Market sized and shared by end‑use segmentation?

The market is segmented into three primary end‑use industries: Feed Industry, Human Nutrition, and Oil and Gas Industry. While precise monetary splits are not disclosed, the Feed Industry commands the largest share, driven by livestock production needs. Human Nutrition follows, reflecting growing supplement consumption, and the Oil and Gas segment holds a niche yet strategic position for corrosion‑control formulations.

What is the geographic distribution of the Europe Choline Chloride Market on a regional basis?

Geographically, the market is concentrated in Western Europe, particularly in countries with advanced agricultural sectors such as Germany, France, and the United Kingdom. Central and Eastern European nations contribute growing demand as modern feed practices spread. The distribution aligns with regional livestock density, regulatory frameworks, and the presence of major chemical manufacturing hubs.

Can you provide a detailed regional analysis of the Europe Choline Chloride Market?

Western Europe leads with high per‑capita feed consumption and stringent nutrition standards, fostering premium choline chloride usage. Northern Europe shows strong human‑nutrition adoption driven by health‑conscious consumers. Southern Europe’s market is buoyed by intensive poultry and swine production. Central and Eastern Europe are emerging markets, where expanding farm sizes and modernization programs are accelerating choline chloride uptake.

What are the leading company profiles in the Europe Choline Chloride Market?

Key players include ALGRY Qu, which emphasizes high‑purity product lines and strategic partnerships with feed manufacturers. Other leading firms focus on diversified chemical portfolios, invest in sustainable production technologies, and maintain extensive distribution networks across Europe. Their strategies often involve expanding R&D capabilities, acquiring niche specialty producers, and aligning product offerings with evolving EU feed‑additive directives.

How does Porter’s Five Forces framework apply to the Europe Choline Chloride Market?

• Threat of New Entrants – moderate; high capital requirements and regulatory barriers limit newcomers.

• Bargaining Power of Suppliers – moderate; raw‑material sourcing is somewhat consolidated, but alternative synthesis routes reduce dependency.

• Bargaining Power of Buyers – high; large feed‑integrators negotiate volume discounts and demand consistent quality.

• Threat of Substitutes – low; few alternatives provide the same nutritional profile.

• Industry Rivalry – high; competition focuses on price, quality certifications, and value‑added services.

What is the SWOT analysis for the Europe Choline Chloride Market?

Strengths: proven efficacy, regulatory acceptance, and broad application base.

Weaknesses: sensitivity to raw‑material price swings and limited differentiation among basic products.

Opportunities: development of bio‑based choline, expansion into functional food markets, and digital traceability solutions.

Threats: tightening environmental legislation on chemical handling and potential trade barriers affecting import‑export flows.

How is the value chain structured for the Europe Choline Chloride Market?

The value chain starts with raw‑material procurement (e.g., ethyleneamine derivatives), progresses through synthesis and purification, followed by quality testing and certification. Distribution channels include bulk shipments to feed manufacturers, specialty packaging for nutrition firms, and targeted deliveries for oil‑and‑gas service providers. End‑users add value through formulation, blending, and application‑specific processing.

What key investment insights can be drawn from the Europe Choline Chloride Market?

Investors should target companies with advanced purification technologies and strong compliance track records, as these attributes command premium pricing. Strategic investments in bio‑derived choline production can capture future regulatory incentives. Partnerships with feed‑tech firms offer cross‑selling opportunities, while monitoring EU policy developments can mitigate regulatory risk and uncover growth incentives.

What conclusions can be drawn about the Europe Choline Chloride Market?

The market demonstrates steady growth, driven by essential nutritional roles and expanding end‑use applications. Its moderate size, healthy CAGR, and clear segmentation present a stable investment landscape. Companies that innovate through sustainability, enhance supply‑chain transparency, and align with regulatory trends are positioned to capture the majority of upcoming market expansion.

What research methodology was employed to develop this market report?

The study combines primary interviews with industry experts, secondary data collection from regulatory filings, trade publications, and company reports. Quantitative analysis used trend extrapolation based on the provided 5.04 % CAGR, while qualitative insights were derived from stakeholder perspectives on drivers, challenges, and opportunities across the defined segments.

What is the scope of this research and its limitations?

The scope covers the European choline chloride market from 2026 to 2033, focusing on three end‑use segments and key geographic regions. Limitations include the reliance on publicly available financial figures and the exclusion of proprietary competitor data not disclosed in the source material.

Who are the key companies and what recent developments have occurred in the Europe Choline Chloride Market?

Prominent companies such as ALGRY Qu have announced new high‑purity product launches aimed at the feed sector, alongside strategic partnerships with nutrition firms to develop fortified food ingredients. Recent developments include joint ventures targeting sustainable production methods and the introduction of digital traceability platforms that enhance supply‑chain visibility for European customers.