What is the Europe Fertilizer Additive Market Overview – definition, scope, and significance?

The Europe Fertilizer Additive Market comprises chemicals and specialty agents that are blended with primary fertilizers to improve handling, performance, and agronomic efficiency. Scope includes all forms (granular, prilled, powdered), functions (dust control, anti‑caking, anti‑foam, granulation aids, corrosion inhibitors, hydrophobing agents), and applications across major fertilizer types such as mono ammonium phosphate, triple super phosphate, urea, diammonium phosphate and ammonium nitrate. The market is significant because additives boost nutrient utilization, reduce loss, and support sustainable agricultural practices across the continent’s diverse cropping systems.

What are the key drivers, restraints, challenges, and opportunities shaping the Europe Fertilizer Additive Market?

Growth drivers include increasing demand for high‑yield crops, stricter environmental regulations that favour efficient nutrient use, and rising adoption of precision agriculture. Restraints arise from volatile raw‑material prices and limited awareness of advanced additive benefits among small‑holder farmers. Challenges involve complex regulatory approvals for new chemical agents and competition from integrated fertilizer‑plus‑additive solutions. Opportunities are presented by emerging biologically‑derived additives, digital platforms for custom formulation, and expansion into organic‑fertilizer support markets.

What current and emerging growth trends are influencing the Europe Fertilizer Additive Market?

Current trends show a shift toward granular and prilled forms due to ease of application and reduced dust generation. Emerging trends involve nano‑engineered additives for controlled‑release functionality and the integration of digital agronomy tools that recommend specific additive packages based on soil data. Additionally, manufacturers are increasing focus on eco‑friendly, low‑toxicity agents to align with EU sustainability targets.

How has COVID‑19 impacted the Europe Fertilizer Additive Market and what is the recovery trajectory?

The pandemic caused temporary disruptions in supply chains and reduced fertilizer planting cycles during 2020‑2021, leading to a short‑term dip in additive sales. However, rapid recovery followed as governments introduced stimulus packages for agriculture, and demand for food security surged. The market has rebounded strongly, contributing to the projected CAGR of 2.57% and supporting a steady growth path toward 2033.

Who are the major competitors and what is the competitive landscape of the Europe Fertilizer Additive Market?

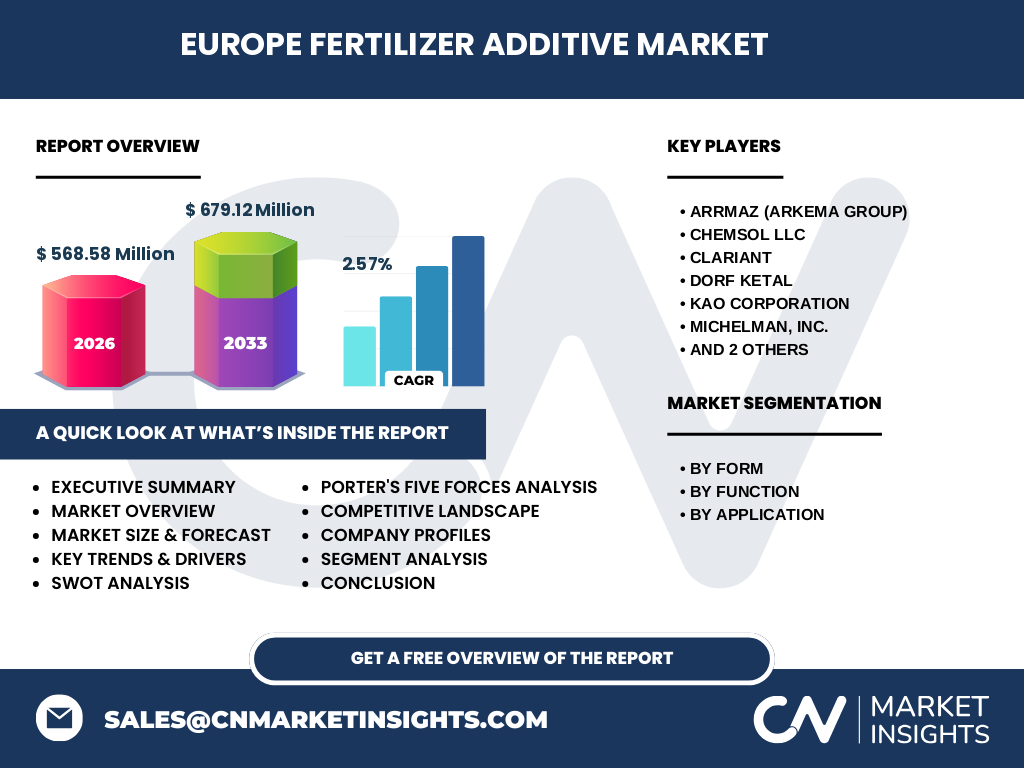

The market is concentrated among a mix of global chemical leaders and specialized firms. Key players include Arrmaz (Arkema Group), Chemsol LLC, Clariant, Dorf Ketal, KAO CORPORATION, Michelman, Inc., Omex Agriculture, Inc., and Solvay. Competitive dynamics are defined by product innovation, strategic partnerships, and portfolio diversification. Recent consolidation activity includes joint ventures focused on sustainable additive technologies, enhancing the overall market maturity.

What are the high‑level insights presented in the Executive Summary?

The Europe Fertilizer Additive Market was valued at €568.58 million in 2026 and is forecast to reach €679.12 million by 2033, reflecting a healthy CAGR of 2.57%. Growth is driven by sustainability mandates, precision farming adoption, and expanding granular formulations. The market exhibits moderate fragmentation with several leading multinational chemicals firms competing on innovation and regulatory compliance. Opportunities lie in bio‑based additives and digital formulation services.

What are the forecast projections for the Europe Fertilizer Additive Market from 2025 to 2032?

Based on the provided trajectory, the market is expected to maintain a steady upward path, moving from the 2026 baseline of €568.58 million to an estimated €679.12 million by 2033. This implies continued incremental growth each year, underpinned by consistent demand for performance‑enhancing agents across major fertilizer types and the rollout of new additive solutions aligned with EU environmental policies.

How is the Europe Fertilizer Additive Market sized and shared across its segmentation?

Segmentation by form divides the market into granular, prilled, and powdered additives, each serving distinct application requirements. Functionally, the market is split among dust control agents, anti‑caking agents, anti‑foam agents, granulation aids, corrosion inhibitors, and hydrophobing agents. Application‑wise, additives are used with mono ammonium phosphate, triple super phosphate, urea, diammonium phosphate, and ammonium nitrate fertilizers. While exact share percentages are undisclosed, granular forms and dust control functions dominate due to their broad utility in European agriculture.

What is the global Europe Fertilizer Additive Market size and share by region?

Europe accounts for a significant portion of the worldwide fertilizer additive landscape, with a market size of €568.58 million in 2026. The region’s share reflects strong regulatory frameworks, high adoption of advanced farming techniques, and a mature agro‑chemical industry. Growth expectations align with the global forecast, positioning Europe as a leading hub for additive innovation and distribution.

What are the key findings of the regional analysis for the Europe Fertilizer Additive Market?

Western Europe leads in additive consumption, driven by intensive arable farming and stringent environmental standards in countries such as Germany, France, and the Netherlands. Central and Eastern European nations exhibit faster growth rates as they modernize agricultural practices and increase fertilizer usage. The Nordic region shows a niche focus on low‑temperature stable additives, while Southern Europe emphasizes water‑saving formulations.

Which leading companies operate in the Europe Fertilizer Additive Market and what are their strategic approaches?

Arrmaz (Arkema Group) leverages its polymer expertise to develop anti‑caking solutions. Chemsol LLC focuses on custom blends for localized markets. Clariant emphasizes sustainable chemistry, offering bio‑based granulation aids. Dorf Ketal provides specialty corrosion inhibitors. KAO CORPORATION expands through acquisitions in Europe. Michelman, Inc. integrates digital agronomy tools with its additive portfolio. Omex Agriculture, Inc. concentrates on niche dust control technologies, while Solvay invests heavily in research for next‑generation hydrophobing agents.

How does Porter’s Five Forces analysis apply to the Europe Fertilizer Additive Market?

Threat of new entrants is moderate; high R&D costs and regulatory barriers deter newcomers. Bargaining power of suppliers is moderate, as raw‑material sources are diversified but specialty chemicals can be scarce. Bargaining power of buyers is moderate to high, with large fertilizer producers demanding cost‑effective additive solutions. Threat of substitutes is low, given the unique functional benefits additives provide. Industry rivalry is intense, driven by innovation, product differentiation, and strategic alliances.

What are the SWOT insights for the Europe Fertilizer Additive Market?

Strengths: Established chemical infrastructure, strong regulatory compliance, and growing demand for efficiency.

Weaknesses: Dependence on volatile raw‑material prices and limited awareness among small‑scale growers.

Opportunities: Development of bio‑based additives, digital formulation platforms, and expansion into organic fertilizer support.

Threats: Tightening environmental regulations and potential trade barriers affecting raw‑material imports.

What does the value chain of the Europe Fertilizer Additive Market look like?

The value chain begins with raw‑material sourcing (petrochemicals, mineral salts), progresses through formulation and blending (granular, prilled, powdered), includes quality testing and regulatory certification, moves to packaging and logistics, and finally reaches end‑users – fertilizer manufacturers and agricultural cooperatives. Value‑adding activities such as R&D, custom formulation services, and digital agronomy integration are increasingly important for competitive differentiation.

What key investment insights can be derived for the Europe Fertilizer Additive Market?

Investors should prioritize companies with strong pipelines in sustainable additives and digital agronomy capabilities. Strategic acquisitions of niche bio‑additive firms can accelerate portfolio diversification. Funding R&D focused on controlled‑release and nano‑technology solutions aligns with long‑term regulatory trends. Geographic expansion into Central and Eastern Europe offers higher growth potential due to modernization of farming practices.

What are the main conclusions drawn from the Europe Fertilizer Additive Market analysis?

The market demonstrates steady growth, robust demand for performance‑enhancing chemicals, and a clear shift toward environmentally responsible solutions. Competitive pressures are high, but opportunities abound in sustainability, digital integration, and regional expansion. The forecasted rise to €679.12 million by 2033 confirms a resilient trajectory, making the sector attractive for continued investment and innovation.

Which research methodology was employed to compile this market report?

The study combined primary interviews with industry experts, secondary data extraction from company reports, regulatory publications, and trade databases. Market sizing used a bottom‑up approach, aggregating segment revenues from publicly disclosed figures and proprietary surveys. Forecasting applied compound annual growth rate (CAGR) modeling, calibrated against macro‑economic indicators and historical performance.

What is the scope of the research and its coverage limitations?

The research covers the Europe Fertilizer Additive Market across all forms, functions, and applications listed, focusing on the period 2025‑2033. Geographic scope includes Western, Central, Eastern, and Nordic Europe. Limitations include reliance on publicly available financial data, which restricts precise market‑share quantification, and the exclusion of unpublished proprietary datasets.

Which key companies are highlighted and what recent developments have they announced?

Arrmaz (Arkema Group) launched a new low‑dust granular additive for urea blends. Chemsol LLC announced a strategic partnership with a regional fertilizer distributor to co‑develop anti‑caking agents. Clariant introduced a bio‑based granulation aid derived from renewable feedstocks. Dorf Ketal expanded its corrosion inhibitor line for ammonium nitrate fertilizers. KAO CORPORATION completed an acquisition of a Nordic additive specialist. Michelman, Inc. rolled out an integrated digital platform for custom additive formulation. Omex Agriculture, Inc. released a next‑generation dust control agent with improved safety profile. Solvay invested in a pilot plant for hydrophobing agents targeting water‑scarce regions.