1. What is the North America Fertilizer Additive Market Overview – definition, scope, and significance?

The North America Fertilizer Additive Market comprises chemicals and specialty ingredients that enhance the performance, handling, and environmental profile of fertilizer products. It includes forms such as granular, prilled, and powdered additives, and functions ranging from dust control to corrosion inhibition. The market serves major agricultural applications—including mono ammonium phosphate, triple super phosphate, urea, diammonium phosphate, and ammonium nitrate—supporting higher crop yields, efficient nutrient use, and compliance with sustainability regulations. Its significance lies in driving productivity for a region that accounts for a large share of global agricultural output.

2. What are the key drivers, restraints, challenges, and opportunities shaping the North America Fertilizer Additive Market?

Key drivers include rising demand for high‑yield crops, stringent environmental standards that favor anti‑caking and dust‑control agents, and ongoing investment in precision agriculture. Restraints stem from volatile raw‑material prices and regulatory scrutiny over certain chemical classes. Challenges involve supply‑chain disruptions and the need for additive compatibility with diverse fertilizer formulations. Opportunities arise from the development of bio‑based additives, growing adoption of granular fertilizers that require granular aids, and expansion into emerging markets within North America that are modernizing their agronomic practices.

3. What are the current growth trends and emerging developments in the North America Fertilizer Additive Market?

Current trends show a shift toward granular and powdered additives that improve uniformity in application. Manufacturers are investing in anti‑foam and hydrophobing agents to meet the requirements of high‑speed liquid fertilizer applications. Emerging developments include nanotechnology‑enhanced additives for better nutrient release control and the integration of digital monitoring tools to track additive performance in real time. Sustainability is also prompting R&D into low‑toxicity, biodegradable additives.

4. How has COVID‑19 impacted the North America Fertilizer Additive Market and what is the recovery trajectory?

The pandemic caused temporary disruptions in raw‑material logistics and a slowdown in fertilizer planting cycles, leading to a short‑term dip in demand for certain additives. However, the market rebounded quickly as agricultural activities resumed, supported by government stimulus programs for food security. The recovery trajectory is positive, with demand expected to grow steadily, reinforced by post‑pandemic emphasis on resilient food supply chains.

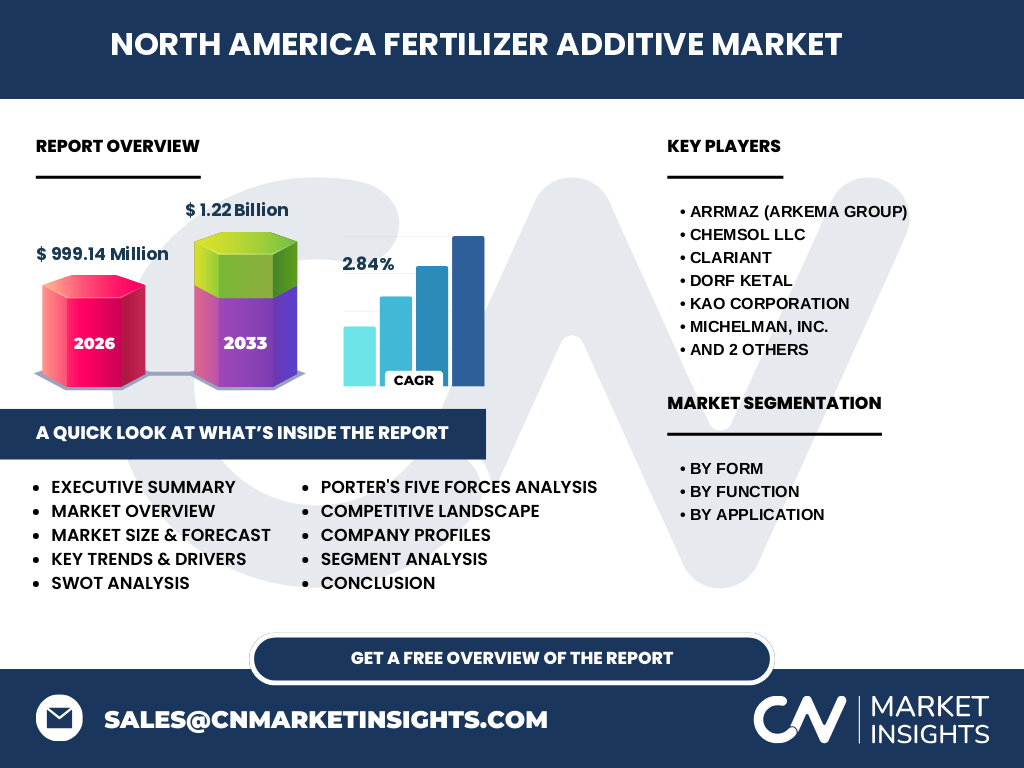

5. Who are the major competitors and what is the state of market consolidation in the North America Fertilizer Additive Market?

Key competitors include Arrmaz (Arkema Group), Chemsol LLC, Clariant, Dorf Ketal, KAO CORPORATION, Michelman, Inc., Omex Agriculture, Inc., and Solvay. The competitive landscape is characterized by strategic partnerships, technology licensing, and selective acquisitions aimed at broadening product portfolios. While the market remains fragmented with several niche players, consolidation is moderate, driven by the need for economies of scale and expanded geographic reach.

6. What are the high‑level findings and key takeaways presented in the Executive Summary?

The Executive Summary highlights a market size of US$ 999.14 million in 2026, projected to reach US$ 1.22 billion by 2033, reflecting a CAGR of 2.84 % over the forecast period. Growth is anchored by strong agronomic demand, regulatory incentives for cleaner additives, and innovation in granular and powdered forms. Competitive dynamics are shaped by a mix of global chemical leaders and specialized regional firms. Strategic opportunities focus on sustainable additive development and leveraging digital agriculture platforms.

7. What are the forecasted market estimates for 2025‑2032?

Based on the provided CAGR of 2.84 %, the market is expected to expand from the 2026 baseline of US$ 999.14 million to approximately US$ 1.22 billion by 2033. This trajectory suggests steady annual growth, with incremental increases each year driven by broader fertilizer application rates and higher adoption of advanced additive functionalities.

8. How is the market sized and shared across the defined segments (form, function, application)?

Segmentation by form includes granular, prilled, and powdered additives, each catering to specific handling and release characteristics. Functionally, the market is divided into dust control agents, anti‑caking agents, anti‑foam agents, granulation aids, corrosion inhibitors, and hydrophobing agents, reflecting the diverse performance needs of fertilizer manufacturers. Application‑wise, additives support mono ammonium phosphate, triple super phosphate, urea, diammonium phosphate, and ammonium nitrate formulations, ensuring optimal nutrient stability and delivery across the major fertilizer product lines.

9. What is the geographic distribution of the market size and share by region within North America?

The market is primarily concentrated in the United States and Canada, with the United States accounting for the majority of demand due to its extensive grain and corn production. Canadian activity is driven by cereal and oilseed cultivation. While exact regional share values are not disclosed, the overall North America market reflects the combined economic output of these two countries, leveraging their advanced agricultural infrastructure.

10. What does the regional analysis reveal about market performance across North America?

In the United States, growth is propelled by large‑scale commercial farming, adoption of precision agriculture, and supportive government policies. Canada’s market is bolstered by its focus on sustainable farming practices and investments in research collaborations. Both regions exhibit a steady increase in additive usage, particularly for anti‑caking and dust control agents, aligning with safety and environmental compliance standards.

11. Which companies lead the North America Fertilizer Additive Market and what are their core strategies?

Leading firms such as Arrmaz (Arkema Group) and Clariant focus on high‑performance specialty chemistries and expanding their granular additive portfolios. Chemsol LLC and Michelman, Inc. leverage strong customer relationships to offer customized solutions. KAO CORPORATION emphasizes innovation in anti‑foam and hydrophobing agents, while Solvay and Dorf Ketal prioritize sustainability through bio‑based additive development. Omex Agriculture, Inc. pursues strategic alliances to broaden market reach.

12. How does Porter’s Five Forces analysis characterize the market’s competitive environment?

Threat of new entrants is moderate due to high R&D costs and regulatory barriers. Bargaining power of suppliers is limited because raw materials are commoditized, though occasional price spikes can affect margins. Bargaining power of buyers is significant as major fertilizer producers demand consistent quality and cost‑effectiveness. Threat of substitutes remains low, given the specialized functions of additives. Rivalry among existing firms is intense, driven by innovation, pricing, and service differentiation.

13. What are the strengths, weaknesses, opportunities, and threats identified in the SWOT analysis?

Strengths include a robust portfolio of functional additives and a growing customer base. Weaknesses involve dependence on volatile raw‑material markets and limited penetration in some niche applications. Opportunities arise from eco‑friendly additive development, digital integration, and expanding agricultural acreage. Threats encompass stricter environmental regulations, potential supply‑chain disruptions, and competitive pressure from emerging low‑cost producers.

14. How is value created and transferred across the North America Fertilizer Additive value chain?

The value chain starts with raw‑material sourcing (e.g., polymers, inorganic compounds), followed by formulation R&D, pilot‑scale manufacturing, and large‑scale production. Quality control, regulatory compliance, and packaging are critical downstream steps. Distribution channels include direct sales to fertilizer manufacturers and third‑party distributors. After‑sales technical support and performance monitoring close the loop, ensuring additive efficacy and customer satisfaction.

15. What investment insights can guide strategic decisions in the North America Fertilizer Additive Market?

Investors should consider targeting companies with strong innovation pipelines, especially those developing biodegradable or bio‑based additives. Leveraging partnerships with precision‑agriculture technology firms can unlock new revenue streams. Capital allocation toward capacity expansion in granular and powdered segments aligns with the projected growth trends. Monitoring regulatory developments will also help mitigate compliance risk.

16. What are the concluding remarks and primary takeaways from the market analysis?

The North America Fertilizer Additive Market is on a steady growth path, underpinned by a solid 2.84 % CAGR and an expected market size of US$ 1.22 billion by 2033. Demand is driven by agricultural productivity goals, regulatory pressures for cleaner operations, and ongoing innovation in additive functionality. Competitive dynamics favor firms that can combine technical excellence with sustainability, making the sector attractive for strategic investment and partnership opportunities.

17. How was the research conducted and what methodology was employed?

The study employed a mixed‑method approach, combining primary interviews with industry experts, supplier surveys, and secondary data analysis from reputable agricultural and chemical market sources. Quantitative forecasts were derived using time‑series modeling anchored on the provided CAGR of 2.84 %. Qualitative insights were validated through cross‑checking with company reports and regulatory publications.

18. What is the scope of the research and any inherent limitations?

The research covers the North America Fertilizer Additive market across form, function, and application segments, focusing on the period 2025‑2033. It includes competitive profiling of eight leading companies and evaluates macro‑economic, regulatory, and technological factors. Limitations arise from the exclusion of proprietary financial data beyond the supplied market size and forecast figures, and from the reliance on publicly available information for company-specific strategies.

19. Which key companies have made recent developments such as product launches, partnerships, or strategic initiatives?

Arrmaz (Arkema Group) recently introduced a new anti‑caking additive optimized for urea blends. Chemsol LLC announced a partnership with a precision‑ag technology firm to integrate additive performance monitoring. Clariant launched a powdered dust‑control agent designed for low‑temperature application. KAO CORPORATION expanded its anti‑foam portfolio with a bio‑based formulation. Michelman, Inc. disclosed a joint venture aimed at developing corrosion inhibitors for ammonium nitrate fertilizers. Solvay reported an acquisition of a niche granulation‑aid developer, enhancing its granular additive capabilities.