Passive Optical Network Market Overview - Definition, scope, and significance

A Passive Optical Network (PON) is a fiber-optic telecommunications technology that delivers broadband network access to end-users through a point-to-multipoint architecture. Unlike active networks that require electrically powered equipment for signal distribution, PONs use unpowered optical splitters to divide a single optical signal into multiple paths, enabling efficient delivery of voice, data, and video services to residential, business, and mobile backhaul applications. The technology represents a fundamental shift in telecommunications infrastructure, offering higher bandwidth capacity, lower operational costs, and greater scalability compared to traditional copper-based systems. PONs have become increasingly significant as global demand for high-speed internet connectivity continues to surge, driven by the proliferation of data-intensive applications, cloud services, and the Internet of Things (IoT).

Passive Optical Network Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers propelling the PON market include the exponential growth in data consumption, increasing demand for high-definition video streaming, and the widespread deployment of 5G networks requiring robust backhaul infrastructure. Government initiatives promoting broadband connectivity in underserved areas and the transition toward fiber-to-the-home (FTTH) deployments are creating substantial market opportunities. However, the market faces restraints such as high initial deployment costs, particularly in rural areas with low population density, and the technical challenges associated with integrating PON technology with existing network infrastructure. The complexity of managing fiber networks and the need for specialized technical expertise present additional challenges. Opportunities exist in emerging markets where broadband penetration remains low, the development of next-generation PON technologies like NG-PON2, and the increasing adoption of PON in enterprise applications beyond traditional residential services.

Passive Optical Network Market Growth Trends - Current and emerging trends shaping the market

The PON market is experiencing several transformative trends that are reshaping the competitive landscape. The migration toward higher-speed PON technologies, particularly the adoption of 10G-PON and NG-PON2, is accelerating as service providers seek to meet growing bandwidth demands. There is a notable trend toward converged PON architectures that can support multiple services simultaneously, including residential broadband, business services, and mobile backhaul. The integration of PON with software-defined networking (SDN) and network function virtualization (NFV) is enabling more flexible and programmable network operations. Additionally, the market is witnessing increased interest in hybrid PON solutions that combine fiber with existing copper infrastructure to optimize deployment costs. The emergence of PON in industrial IoT applications and smart city initiatives represents a new frontier for market expansion, while advancements in optical component technology are driving down costs and improving performance metrics.

COVID-19 Impact on the Passive Optical Network Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a dual impact on the PON market, creating both challenges and opportunities. Initially, the market experienced disruptions due to supply chain interruptions, delayed infrastructure projects, and reduced capital expenditure by service providers. However, the pandemic simultaneously accelerated the demand for broadband services as remote work, online education, and digital entertainment became essential components of daily life. This surge in bandwidth consumption highlighted the limitations of existing copper-based infrastructure and reinforced the need for fiber-optic solutions. The recovery trajectory has been robust, with increased investments in network infrastructure to support the "new normal" of hybrid work models and digital services. Service providers are now prioritizing PON deployments to ensure network resilience and capacity, while governments are incorporating broadband expansion into economic stimulus packages, creating a favorable environment for market growth in the post-pandemic era.

Passive Optical Network Market Competitive Landscape - Major competitors and market consolidation

The PON market features a mix of established telecommunications equipment vendors and specialized optical networking companies competing for market share. The competitive landscape is characterized by technological innovation, strategic partnerships, and geographic expansion strategies. Major players like Huawei Technologies, Nokia Corporation, and ZTE Corporation leverage their extensive telecommunications experience and global presence to maintain strong positions. Meanwhile, companies such as Calix, Adtran, and Ciena focus on differentiated solutions and niche market segments. The market has witnessed some consolidation through mergers and acquisitions, particularly as larger companies seek to acquire specialized PON technology capabilities. Competition is intensifying as companies invest in next-generation PON technologies and expand their product portfolios to address evolving customer requirements. The competitive dynamics are further influenced by regional market preferences, with different technologies dominating in various geographic areas based on historical deployments and regulatory frameworks.

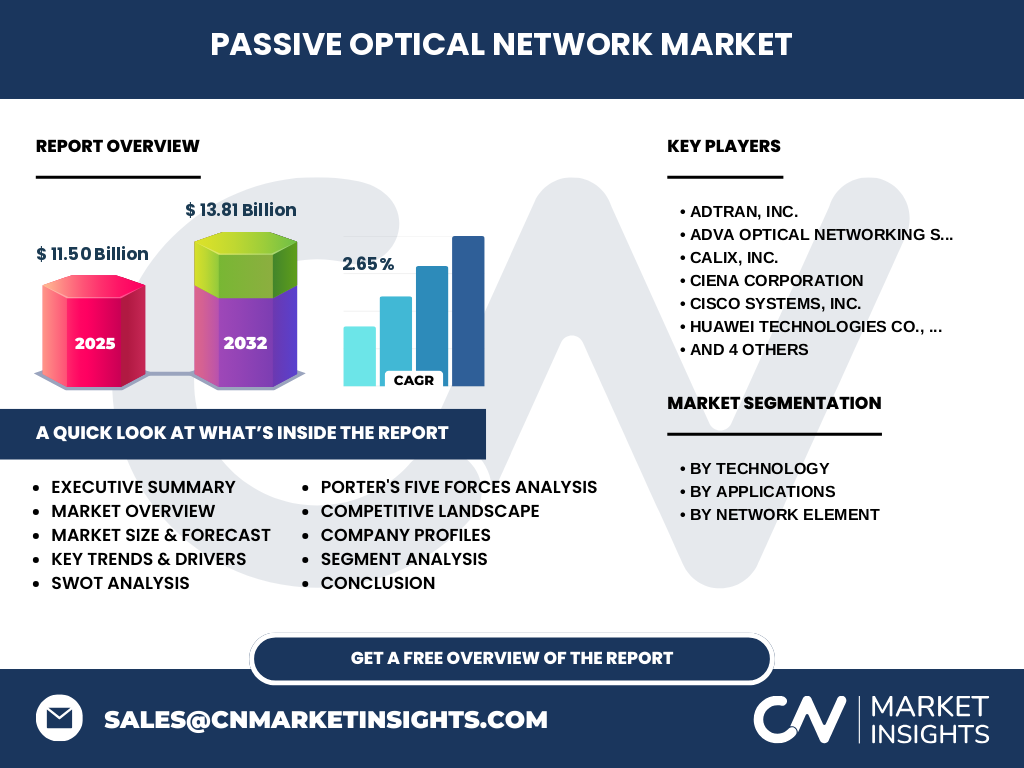

Executive Summary - High-level overview and key findings about Passive Optical Network Market

The Passive Optical Network market is positioned for steady growth, with the market size projected to increase from $11.50 billion in 2025 to $13.81 billion by 2032, representing a compound annual growth rate of 2.65%. This growth is underpinned by the fundamental shift toward fiber-optic infrastructure driven by insatiable bandwidth demand across residential, business, and mobile backhaul applications. The market segmentation reveals a diverse ecosystem spanning multiple PON technologies including GPON, EPON, and NG-PON, each serving specific market needs and regional preferences. The competitive landscape features a balanced mix of global telecommunications giants and specialized optical networking firms, creating a dynamic environment for innovation and market development. Key findings indicate that while the overall growth rate may appear modest, the market represents critical infrastructure investment with long-term implications for digital transformation across industries and economies.

Passive Optical Network Market Forecast - Projections for 2025-2032 period

The PON market forecast for 2025-2032 indicates a measured but steady growth trajectory, with the market expanding from $11.50 billion to $13.81 billion over the seven-year period. This represents a compound annual growth rate of 2.65%, reflecting the mature nature of the market while acknowledging ongoing infrastructure investments. The forecast period is expected to witness continued migration from legacy copper-based systems to fiber-optic networks, particularly in developed markets where broadband penetration is high but capacity requirements are escalating. Emerging markets will contribute significantly to growth as governments and service providers invest in broadband infrastructure to support economic development and digital inclusion initiatives. The forecast also accounts for the gradual adoption of next-generation PON technologies, with NG-PON2 deployments gaining momentum as service providers seek to future-proof their networks. Regional variations in growth rates are anticipated, with Asia-Pacific markets likely to show stronger growth compared to more saturated markets in North America and Europe.

Passive Optical Network Market Size and Share by Segmentation - Breakdown by {segmentData}

The PON market segmentation reveals distinct patterns across technology types, applications, and network elements. By technology, Gigabit Passive Optical Network (GPON) currently holds the largest market share due to its widespread deployment and proven reliability, while Ethernet Passive Optical Network (EPON) maintains a strong presence particularly in Asia-Pacific markets. Next-Generation PON (NG-PON) represents the fastest-growing technology segment as service providers prepare for future bandwidth requirements. In terms of applications, residential services dominate the market share, driven by the ongoing fiber-to-the-home (FTTH) deployments, followed by business services that require higher bandwidth and reliability. Mobile backhaul applications are experiencing rapid growth as 5G networks expand. The network element segmentation shows that Optical Line Terminals (OLTs) represent the largest component market due to their critical role in network architecture, while Optical Network Terminals (ONTs) and Optical Power Splitters constitute significant but smaller segments. This segmentation analysis provides insights into where market opportunities and competitive dynamics are most pronounced.

Global Passive Optical Network Market Size and Share by Region - Geographic distribution

The global PON market exhibits significant regional variations in market size and growth patterns. Asia-Pacific represents the largest regional market, driven by massive infrastructure investments in countries like China, Japan, and South Korea, where government initiatives and high population density create favorable conditions for PON deployment. North America maintains a substantial market share, characterized by advanced broadband infrastructure and ongoing upgrades to support increasing data demands. Europe follows as a significant market, with varying adoption rates across different countries reflecting diverse regulatory environments and market maturity levels. Emerging markets in Latin America, the Middle East, and Africa are showing promising growth potential as governments prioritize digital infrastructure development. The regional distribution also reflects technology preferences, with GPON dominating in most regions while EPON maintains stronger positions in specific Asian markets. These geographic variations create both opportunities and challenges for market participants seeking to expand their global footprint.

Regional Analysis of the Passive Optical Network Market - Detailed regional market performance

Regional analysis reveals distinct market dynamics and performance characteristics across different geographic areas. In Asia-Pacific, the market is characterized by aggressive deployment targets and massive scale, with China leading global PON installations through its "Fiber to the Village" initiative and other broadband expansion programs. Japan and South Korea represent mature markets with high broadband penetration but continue to invest in network upgrades to maintain technological leadership. North America shows steady but measured growth, with the United States and Canada focusing on bridging the digital divide and upgrading existing infrastructure to support emerging applications. The European market presents a mixed picture, with Western European countries demonstrating high PON adoption rates while Eastern European markets are still in earlier deployment phases. Regional regulatory frameworks significantly influence market performance, with some regions offering incentives for fiber deployment while others maintain more conservative approaches. These regional variations create opportunities for market participants to develop tailored strategies that address specific local requirements and market conditions.

Leading Company Profiles in the Passive Optical Network Market - Industry players and strategies

The PON market features several prominent companies with distinct competitive strategies and market approaches. Huawei Technologies leverages its comprehensive telecommunications portfolio and strong presence in Asian markets to maintain a leading position, particularly in GPON deployments. Nokia Corporation focuses on innovation and next-generation PON solutions, emphasizing its Bell Labs heritage and R&D capabilities. ZTE Corporation competes effectively in emerging markets with cost-competitive solutions and strong government relationships. Calix specializes in broadband access solutions with a focus on service provider partnerships and cloud-based management platforms. Adtran emphasizes its expertise in hybrid fiber-copper solutions and rural broadband deployments. Ciena Corporation differentiates through its WaveLogic coherent optical technology and network automation capabilities. Cisco Systems brings its extensive networking expertise to the PON market, particularly in enterprise and business applications. Motorola Solutions leverages its communications infrastructure heritage, while Infinera focuses on high-capacity optical transport solutions. These companies employ various strategies including technological innovation, strategic partnerships, geographic expansion, and vertical integration to strengthen their market positions.

Porter's Five Forces Analysis of the Passive Optical Network Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the PON market landscape. The threat of new entrants remains moderate due to the high capital requirements for R&D, manufacturing infrastructure, and established relationships with service providers. However, technological advancements and emerging market opportunities continue to attract new players, particularly in specialized segments. The bargaining power of buyers, primarily telecommunications service providers and large enterprises, is significant as they represent concentrated purchasing power and can influence pricing and technical specifications. Supplier bargaining power varies across different components, with optical component suppliers holding moderate power due to specialized manufacturing requirements. The threat of substitute technologies, such as wireless broadband and cable-based solutions, presents ongoing competitive pressure, though fiber-optic advantages in capacity and reliability maintain PON's competitive position. Competitive rivalry is intense among established players, driven by technological innovation, pricing pressures, and the need to differentiate through service offerings and support capabilities. These forces collectively shape market profitability and competitive strategies within the PON industry.

SWOT Analysis of the Passive Optical Network Market - Strengths, weaknesses, opportunities, threats

A comprehensive SWOT analysis of the PON market reveals critical factors influencing its development trajectory. Strengths include the technology's inherent advantages in bandwidth capacity, scalability, and energy efficiency compared to alternative access technologies. PON's point-to-multipoint architecture enables cost-effective deployment and operational savings for service providers. The technology's proven reliability and maturity, particularly in GPON implementations, provide a strong foundation for continued adoption. However, weaknesses exist in the form of high initial deployment costs, especially in areas with challenging terrain or low population density. The complexity of network planning and the need for specialized technical expertise can create implementation challenges. Opportunities abound in the form of 5G backhaul requirements, smart city initiatives, and the ongoing digital transformation across industries. Emerging markets with low broadband penetration represent significant growth potential, while technological advancements in NG-PON continue to expand application possibilities. Threats include competitive pressure from alternative technologies, potential regulatory changes affecting deployment incentives, and economic uncertainties that could impact infrastructure investment decisions. Understanding these SWOT factors is crucial for stakeholders developing strategic responses to market dynamics.

Passive Optical Network Market Value Chain Analysis - Industry structure and value flow

The PON market value chain encompasses multiple interconnected stages, each contributing to the delivery of end-to-end optical networking solutions. At the foundation, raw material suppliers provide essential components including optical fibers, semiconductor materials, and specialized manufacturing equipment. Component manufacturers transform these materials into critical PON elements such as optical transceivers, splitters, and integrated circuits. System integrators and original equipment manufacturers (OEMs) combine these components into complete PON solutions, incorporating software platforms and management systems. Telecommunications service providers serve as the primary channel to end-users, deploying PON infrastructure and offering connectivity services to residential, business, and mobile backhaul customers. Value flows through this chain as each participant adds specialized capabilities, with significant value creation occurring at the system integration and service delivery stages. The value chain is characterized by strategic partnerships and vertical integration initiatives, as companies seek to control critical technologies and enhance their competitive positioning. Understanding this value chain structure is essential for identifying investment opportunities and strategic collaboration possibilities within the PON ecosystem.

Key Investment Insights in the Passive Optical Network Market - Strategic investment recommendations

Investment insights for the PON market highlight several strategic considerations for stakeholders seeking to capitalize on market opportunities. The ongoing transition to higher-speed PON technologies, particularly NG-PON2, represents a compelling investment theme as service providers upgrade their networks to support future bandwidth requirements. Investment in companies with strong intellectual property portfolios and technological differentiation is recommended, given the importance of innovation in maintaining competitive advantage. The growing demand for PON in 5G backhaul applications presents investment opportunities in companies developing specialized solutions for mobile network operators. Geographic diversification is advisable, with particular attention to emerging markets where broadband penetration remains low and government initiatives support infrastructure development. Investments in companies offering comprehensive service portfolios, including network planning, deployment, and managed services, are attractive given the trend toward outsourced network operations. Additionally, companies developing software-defined and cloud-managed PON solutions represent interesting investment targets as the industry moves toward more programmable and automated network architectures. These investment insights reflect the market's evolution toward higher performance, greater flexibility, and expanded application domains.

Passive Optical Network Market Conclusion - Summary and key takeaways

The Passive Optical Network market represents a critical component of global telecommunications infrastructure, enabling the high-speed connectivity essential for digital transformation across industries and societies. With the market projected to grow from $11.50 billion in 2025 to $13.81 billion by 2032 at a CAGR of 2.65%, the industry demonstrates steady but measured expansion driven by fundamental shifts toward fiber-optic networks. Key takeaways include the technology's proven advantages in bandwidth capacity and operational efficiency, the ongoing migration toward next-generation PON solutions, and the diverse application landscape spanning residential, business, and mobile backhaul services. The competitive landscape features a mix of global telecommunications giants and specialized optical networking firms, creating a dynamic environment for innovation and market development. Regional variations in market maturity and technology preferences create both opportunities and challenges for market participants. As the demand for high-speed connectivity continues to escalate, PON technology remains central to meeting these requirements while supporting emerging applications in 5G, smart cities, and industrial IoT. The market's future trajectory will be shaped by technological advancements, regulatory frameworks, and the evolving needs of an increasingly connected world.

Research Methodology - How this research was conducted

This comprehensive market research was conducted using a rigorous methodology combining primary and secondary research approaches to ensure accuracy and reliability. Primary research involved interviews with industry experts, telecommunications service providers, equipment manufacturers, and technology analysts to gather firsthand insights into market dynamics, technological trends, and competitive strategies. Secondary research encompassed extensive review of company annual reports, financial filings, industry publications, technical journals, and market databases to validate findings and establish historical context. Data triangulation techniques were employed to cross-verify information from multiple sources, while market size calculations utilized both top-down and bottom-up approaches to ensure comprehensive coverage. The research methodology incorporated segmentation analysis across technology types, applications, and network elements, with regional assessments based on economic indicators, infrastructure development patterns, and regulatory environments. Forecasting models considered technological roadmaps, investment trends, and macroeconomic factors to project market growth through 2032. This multi-faceted approach ensures the research provides a robust and reliable foundation for understanding the PON market landscape.

Research Scope - Coverage and limitations

This research provides comprehensive coverage of the global Passive Optical Network market, focusing on key technology segments including Gigabit Passive Optical Network (GPON), Ethernet Passive Optical Network (EPON), and Next-Generation PON (NG-PON). The scope encompasses major application areas such as residential services, business services, and mobile backhaul, along with essential network elements including Optical Network Terminals, Optical Line Terminals, and Optical Power Splitters. Geographic coverage extends across major regions including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with detailed analysis of market dynamics within each region. The research timeframe spans from historical data through 2025 to forecast projections extending to 2032. Limitations include the exclusion of certain niche PON applications and emerging technologies still in early development stages. Additionally, while the research provides comprehensive market sizing and trend analysis, specific financial metrics for individual companies are limited to publicly available information. The scope also does not extend to detailed technical specifications of PON equipment, focusing instead on market-level analysis and strategic implications for industry stakeholders.

Key Companies and Recent Developments in the Passive Optical Network Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The PON market features several key companies driving technological innovation and market expansion through strategic initiatives. Huawei Technologies recently announced advancements in its OptiXstar series, introducing enhanced GPON and XG-PON solutions with improved energy efficiency and management capabilities. Nokia Corporation launched its latest FP4 optical platform, supporting NG-PON2 deployments with increased capacity and simplified operations. ZTE Corporation unveiled new 10G PON solutions optimized for 5G backhaul applications, strengthening its position in mobile network operator markets. Calix introduced its Broadband Access Network Gateway (BANG) platform, integrating PON technology with cloud-managed services for service providers. Adtran announced strategic partnerships with multiple rural broadband initiatives, focusing on cost-effective fiber deployment solutions. Ciena Corporation expanded its WaveLogic coherent optical technology to support converged PON and transport network architectures. Cisco Systems launched enhanced enterprise PON solutions targeting business services and industrial IoT applications. Motorola Solutions strengthened its public safety communications portfolio with new PON-enabled infrastructure solutions. These recent developments reflect the industry's focus on higher speeds, greater flexibility, and expanded application domains, while strategic partnerships and product innovations continue to shape the competitive landscape.