What is the Probe Card Market overview – definition, scope, and significance?

The Probe Card Market encompasses the design, manufacturing, and supply of specialized test interface devices used to electrically test semiconductor wafers during the fabrication process. A probe card physically connects the wafer’s bond pads to automated test equipment, enabling high‑speed, high‑precision verification of device functionality, performance, and reliability. The market scope covers all types of probe cards (advanced and standard), the principal technologies (MEMS, cantilever, vertical), and major application segments such as foundry & logic, DRAM, flash, and other memory or logic products. Its significance stems from the critical role probe cards play in wafer‑level testing, which directly influences yield, time‑to‑market, and overall manufacturing cost for semiconductor manufacturers worldwide.

What are the main drivers, restraints, challenges, and opportunities influencing the Probe Card Market?

Key drivers include the rapid growth of advanced logic and memory nodes, increasing wafer sizes (up to 300 mm and beyond), and the demand for higher test throughput to support higher‑volume production. Technological strides in MEMS‑based probe cards, offering finer pitch and superior reliability, further boost adoption. Restraints arise from the high capital cost of advanced probe card systems and the long development cycles required for new node support. Challenges involve maintaining probe integrity at sub‑10 nm pitches and integrating probe cards with emerging test architectures such as wafer‑level packaging. Opportunities are found in expanding applications for novel memory technologies (e.g., 3D‑XPoint), the rise of heterogeneous integration, and the need for in‑line testing solutions that reduce defect‑related losses.

Which growth trends are currently shaping the Probe Card Market?

Current trends include a shift toward MEMS probe cards owing to their ability to achieve sub‑micron pitch and higher durability. Vendors are also investing in vertical probe technologies that provide better contact force control for fragile advanced nodes. Another trend is the migration to higher‑frequency testing to accommodate faster device speeds, prompting the development of advanced signal integrity solutions within probe cards. Additionally, the industry is seeing increased collaboration between probe card manufacturers and test equipment providers to deliver turnkey wafer‑testing platforms.

How did COVID‑19 impact the Probe Card Market and what is the recovery trajectory?

The pandemic caused temporary disruptions in semiconductor fab operations and supply‑chain constraints for precision components, leading to a short‑term slowdown in probe card orders. However, the rapid rebound in demand for consumer electronics, data‑center servers, and automotive electronics accelerated the resumption of wafer‑testing activities. As fabs returned to full capacity, the market experienced a robust recovery, with demand for next‑generation probe cards outpacing the pre‑COVID baseline, setting the stage for strong growth in the forecast period.

What does the competitive landscape of the Probe Card Market look like?

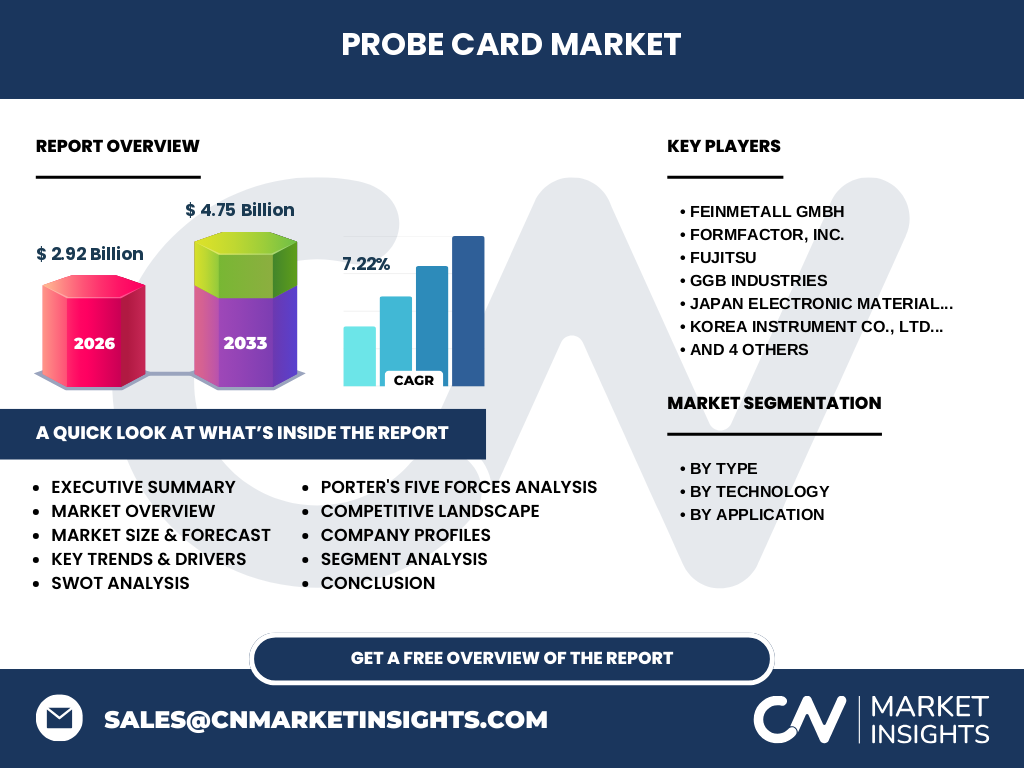

The market is moderately consolidated, featuring a mix of long‑established specialists and emerging technology firms. Major players such as FEINMETALL GmbH, FormFactor, Inc., Fujitsu, GGB Industries, Japan Electronic Materials Corporation, Korea Instrument Co., Ltd., MPI Corporation, Micronics Japan Co., Ltd., SV Probe, and Technoprobe S.p.A. dominate the space. Competition is driven by technological differentiation, portfolio breadth (advanced versus standard cards), and strategic partnerships with semiconductor manufacturers. Recent consolidation activity includes targeted acquisitions aimed at augmenting MEMS capabilities and expanding regional service networks.

What are the key findings highlighted in the Executive Summary?

The Probe Card Market is projected to grow from a 2026 valuation of $2.92 billion to $4.75 billion by 2033, reflecting a CAGR of 7.22 %. Growth is powered by escalating wafer‑level testing requirements for advanced logic and memory nodes, the adoption of MEMS and vertical probe technologies, and the expansion of high‑volume semiconductor production in Asia‑Pacific. Competitive dynamics are marked by a few dominant suppliers leveraging R&D to deliver higher‑density, higher‑reliability cards. The market offers attractive investment potential, especially in companies that can shorten time‑to‑market for next‑generation probe solutions.

What are the forecast expectations for the Probe Card Market from 2025 to 2032?

Forecasts indicate a steady upward trajectory, with the market reaching $4.75 billion by the end of 2033. The projection assumes continued scaling of wafer sizes, ongoing migration to advanced nodes (7 nm and below), and sustained demand from the burgeoning AI, 5G, and automotive semiconductor segments. The average annual growth rate of 7.22 % suggests that each year the market will add roughly $200–$250 million in revenue, driven principally by advanced probe card adoption and replacement cycles for aging test infrastructure.

How is the Probe Card Market sized and shared by segment?

Segment analysis reveals three primary dimensions:

By Type: Advanced probe cards command a higher price premium due to finer pitch, enhanced durability, and integrated signal conditioning, while standard probe cards serve cost‑sensitive, lower‑density applications.

By Technology: MEMS technology holds the largest share among the three, owing to its superior scalability for sub‑micron pitches. Cantilever cards remain prevalent in legacy nodes, and vertical probes are gaining traction for high‑force, high‑reliability testing.

By Application: The foundry and logic segment leads usage, reflecting the volume of high‑performance CPUs and ASICs. DRAM and flash follow, driven by memory‑intensive data‑center and mobile markets. “Other Applications” include emerging areas such as power management ICs and RF components.

What is the geographic distribution of the global Probe Card Market?

The market is globally dispersed, with the Asia‑Pacific region (particularly Taiwan, South Korea, Japan, and China) holding the largest share due to its concentration of fab capacity and leading semiconductor manufacturers. North America follows, primarily driven by design‑centric fabs and high‑value test services. Europe maintains a modest share, focusing on niche high‑precision applications and R&D activities.

What does the regional analysis of the Probe Card Market reveal?

In Asia‑Pacific, robust fab expansions and government incentives for semiconductor self‑sufficiency fuel strong demand for both advanced and standard probe cards. The region’s focus on 3‑nm and beyond nodes amplifies the need for MEMS‑based solutions. North America’s market is characterized by a higher proportion of pilot‑line and prototype testing, wherein flexibility and rapid turn‑around are prized, benefitting companies offering fast‑service engineering support. Europe’s market is influenced by precision‑instrument manufacturers and collaborative research initiatives, leading to incremental growth in advanced probe card innovations.

Which companies are the leading players in the Probe Card Market and what are their strategies?

Key firms include:

• FEINMETALL GmbH – focuses on high‑precision MEMS probe cards and strategic partnerships with leading fabs.

• FormFactor, Inc. – leverages its broad test‑equipment portfolio to bundle probe cards with automated test solutions.

• Fujitsu – invests in vertical probe technology to address high‑force testing for power devices.

• GGB Industries – emphasizes cost‑effective standard cards for legacy nodes while expanding MEMS capabilities.

• Japan Electronic Materials Corporation – prioritizes material innovations to improve probe durability.

• Korea Instrument Co., Ltd. – targets the DRAM market with customized cantilever designs.

• MPI Corporation – focuses on rapid engineering cycles for prototype testing.

• Micronics Japan Co., Ltd. – expands its global service network to support high‑volume production.

• SV Probe – specializes in niche high‑frequency probe solutions.

• Technoprobe S.p.A. – invests in R&D for next‑generation MEMS and vertical probes.

How does Porter’s Five Forces analysis apply to the Probe Card Market?

Threat of new entrants: Moderate – high capital requirements and proprietary technology create barriers, but niche entrants can succeed with specialized MEMS expertise.

Bargaining power of suppliers: Low to moderate – component suppliers for precision materials are limited, yet large manufacturers maintain multiple sources.

Bargaining power of buyers: High – fab operators demand high reliability and can switch suppliers if performance criteria are not met.

Threat of substitutes: Low – there are few viable alternatives to probe cards for wafer‑level electrical testing.

Industry rivalry: High – competition centers on technology leadership, price, and service speed, driving continuous innovation.

What are the SWOT insights for the Probe Card Market?

Strengths: Critical role in semiconductor yield, advanced MEMS technology, established supplier relationships.

Weaknesses: High R&D costs, long development cycles, dependence on fab capital cycles.

Opportunities: Expansion into AI‑driven testing, 3D‑stacked memory, and heterogeneous integration; growing demand for in‑line testing.

Threats: Rapid node shrinkage outpacing probe development, potential supply constraints for rare materials, macro‑economic volatility affecting fab investment.

How is the Probe Card Market value chain structured?

The value chain begins with material sourcing (high‑purity silicon, diamond, and alloy components), proceeds to design engineering (CAD, simulation, and reliability analysis), moves into precision manufacturing (clean‑room assembly, laser cutting, and MEMS micromachining), followed by rigorous testing and qualification, and ends with distribution to fabs and after‑sales support (calibration, repair, and lifecycle management). Value is added primarily at the design‑engineer and manufacturing stages, where technology differentiation occurs.

What key investment insights can be drawn from the Probe Card Market?

Investors should target companies with strong MEMS IP portfolios and proven fab‑partner programs, as these are positioned to capture the bulk of growth from advanced node testing. Firms offering integrated test solutions (probe card plus test equipment) can command higher margins through bundling. Also, companies expanding service capabilities in Asia‑Pacific stand to benefit from the region’s fab boom. Strategic M&A focusing on niche vertical probe technology may unlock synergistic cost efficiencies.

What is the overall conclusion of the Probe Card Market analysis?

The Probe Card Market is on a clear growth trajectory, underpinned by the relentless scaling of semiconductor technology and the need for precise, high‑throughput wafer testing. With a projected market size of $4.75 billion by 2033 and a 7.22 % CAGR, the sector presents robust opportunities for innovators, service‑oriented firms, and investors. Success will hinge on delivering next‑generation MEMS and vertical probe technologies that meet the exacting demands of sub‑10 nm nodes while maintaining cost competitiveness.

What research methodology was employed for this market study?

The research combined primary interviews with senior executives from probe‑card manufacturers, fab test engineers, and industry analysts, together with secondary data from company reports, trade publications, and semiconductor fab forecasts. Quantitative modeling used historical revenue data, technology adoption curves, and fab capacity growth to extrapolate the forecast. Cross‑validation with independent market databases ensured consistency.

What is the scope of this Probe Card Market research?

The study covers global demand for probe cards across all major technology types (MEMS, cantilever, vertical) and applications (foundry & logic, DRAM, flash, other). It includes segmentation by product type, technology, and end‑use, as well as geographic analysis for the primary regions (Asia‑Pacific, North America, Europe). The scope excludes peripheral test‑equipment markets and focuses on wafer‑level probing solutions only.

Which key companies and recent developments should stakeholders be aware of?

Recent highlights include FEINMETALL GmbH’s launch of a next‑generation MEMS probe card capable of sub‑5 µm pitch, FormFactor’s strategic partnership with a leading AI chip fab to co‑develop high‑frequency probe solutions, and Technoprobe’s acquisition of a vertical‑probe specialist to broaden its product portfolio. Fujitsu announced a new vertical probe line optimized for power‑device testing, while Korea Instrument introduced a cantilever series tailored for next‑gen DRAM. These developments illustrate the market’s focus on technology advancement and collaborative innovation.